1. Introduction

Purpose of the Article: This article provides an up-to-date overview of the cryptocurrency landscape, examining key trends and recent developments as of today. The crypto market evolves rapidly, so staying informed is crucial for both investors and enthusiasts. By understanding the latest market movements, technological innovations, regulatory shifts, and adoption patterns, readers can make better decisions in this fast-paced space. We also use El Salvador’s bold Bitcoin experiment – the first nation to adopt Bitcoin as legal tender – as a case study to gauge how the world’s crypto experiment is faring in practice.

Why Staying Updated Matters: The crypto industry is known for its volatility and innovation. Prices of assets like Bitcoin and Ethereum can swing dramatically in days, while new technologies (from Layer-2 scaling solutions to NFTs) emerge frequently. For investors, missing a regulatory update or market trend could mean overlooking significant risks or opportunities. Enthusiasts and builders also benefit from tracking trends to identify where the industry is heading. Reliable information from trusted platforms such as CoinDesk, Glassnode, and Bloomberg Crypto can help cut through the noise and provide data-driven insights. In a market where sentiment can shift on a tweet and new protocols can disrupt incumbents, an informed participant is far better equipped to navigate and thrive.

Key Insights Covered: In this article, we will explore:

- Market Movements: The current performance of the global crypto market (market capitalization, recent price trends of leading cryptocurrencies, and significant market drivers).

- Technological Innovations: Recent advancements in blockchain technology (scalability improvements, Ethereum 2.0’s impact, emerging projects like Solana) and security enhancements (smart contract security, zero-knowledge proofs).

- Regulation: The evolving legal landscape, from U.S. SEC and CFTC actions to Europe’s MiCA regulations and other global policy updates, including high-profile legal cases involving major exchanges.

- Adoption & Sentiment: Trends in both retail and institutional adoption – how more people and companies are using crypto – and the role of social media and influencers in shaping market sentiment.

- On-Chain Activity: What on-chain metrics (like transaction volumes, active addresses, liquidity in DeFi) tell us about the health of the crypto ecosystem.

- Emerging Trends: The growth of NFTs and DeFi’s evolution, plus the rise of stablecoins and progress on central bank digital currencies (CBDCs).

- Investor Behavior: How investor psychology and risk management strategies are adapting in the face of volatility and uncertainty.

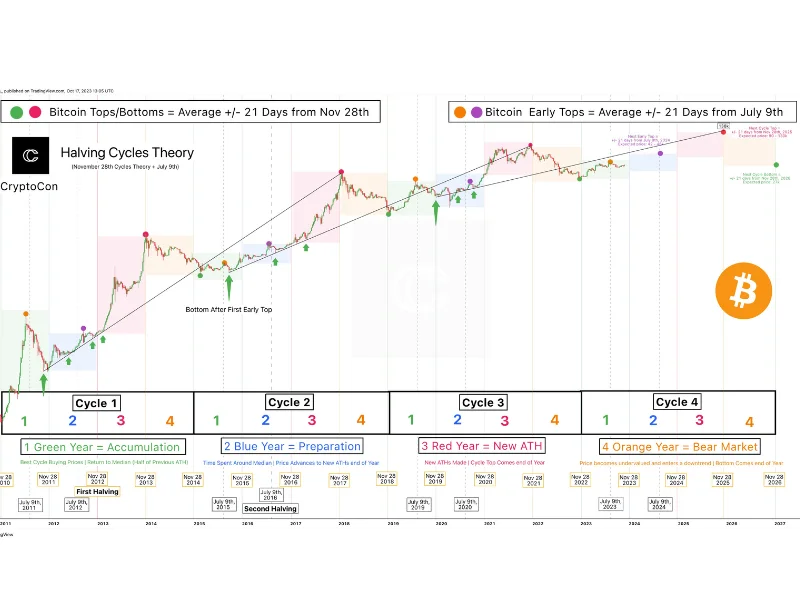

- Case Studies: Specific examples, including Bitcoin’s halving cycles (and their price impacts) and Ethereum’s transition to 2.0, to illustrate broader points.

- Global Events Impact: How macroeconomic factors (inflation, recession fears) and geopolitical events influence crypto markets.

- Expert Opinions: Insights and predictions from industry experts about the future of crypto.

By the end, readers should have a comprehensive understanding of where the crypto market stands today and where it might be headed, along with an appreciation for why staying informed via credible sources is so important.

2. Global Market Trends

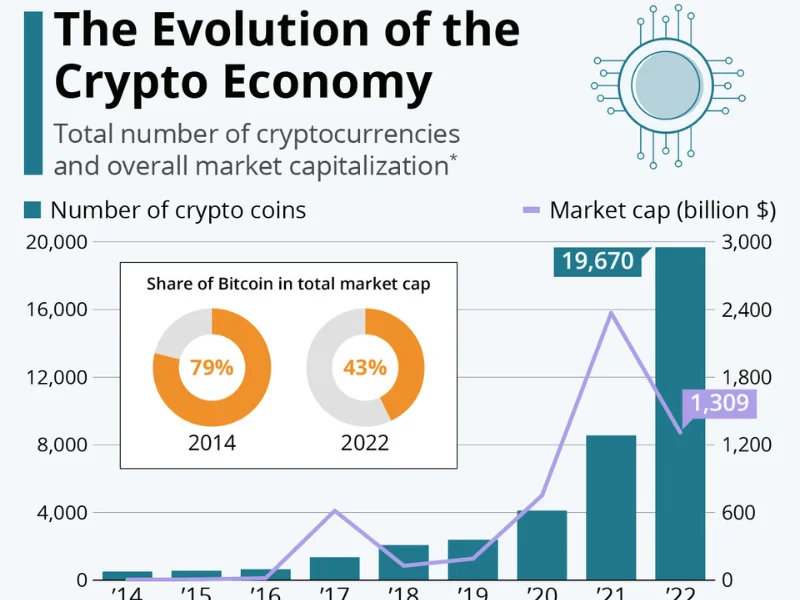

Current Market Performance & Capitalization: The global cryptocurrency market is experiencing robust growth in 2025. As of now, the total crypto market capitalization stands around $3.86 trillion[1], which reflects roughly a 67% increase from a year ago[2]. This surge underscores the sector’s recovery and expansion after the last “crypto winter.” Bitcoin (BTC), the largest cryptocurrency, alone accounts for over $2.18 trillion of the market (approximately 56.6% dominance) while Ethereum (ETH) comprises about 13.8%[3]. Notably, stablecoins (crypto tokens pegged to stable assets like the USD) collectively make up about $282 billion in market cap, roughly 7.3% of the total[3], highlighting their significant role in providing liquidity and a haven during volatility.

Major cryptocurrencies have hit new milestones in 2025. Bitcoin’s price pushed past its previous all-time high (around $69k in late 2021) and reached six figures earlier this year, peaking above the $110,000 mark[4]. In fact, BTC hit a fresh record high in early August 2025, which subsequently triggered some profit-taking and a healthy correction[5]. As of late August, Bitcoin is trading in the ~$110K–115K range after a brief pullback (about 9% off its peak)[6]. Ethereum, similarly, rallied to a new record around $4,946 in recent weeks[7]. Other top altcoins like BNB, XRP, Solana (SOL), etc., have also seen strong year-to-date gains, although with typical higher volatility than Bitcoin. For example, Solana climbed back toward its all-time high (~$290) during the year’s bull run[8], and XRP reached multi-year highs above $2.90 following favorable legal developments.

Trend Analysis: Recent market action shows a mix of bullish momentum and short-term consolidation. Over the past month, crypto prices experienced a rally followed by a moderate correction. In mid-August the total market cap briefly touched $3.9T, then dipped and bounced about 1% off the lows to ~$3.86T by late August[9]. Analysts describe this as a “bounce on the way down” rather than a full trend reversal, indicating caution as markets digest gains[9]. In the short-term (24h to 7d), volatility has returned: daily moves of 1–5% are common for major assets. For instance, Bitcoin traded between roughly $109K and $113K in a recent 24-hour span and was down about 1% on the day[10]. Ethereum saw a slightly larger daily swing (recently ~$4,400, down ~3% in 24h)[11]. Over a weekly view, prices have seesawed – a sharp mid-August sell-off (after BTC’s record high) was followed by a stabilization as some buyers stepped in[12][5]. Significant events driving these fluctuations include macroeconomic signals (like U.S. Federal Reserve commentary), ETF fund flow dynamics, and occasional large holder (“whale”) trades. For example, news of ETF outflows and profit-taking contributed to Bitcoin struggling to hold above $115K[12], while more dovish inflation data or hints of rate cuts have tended to boost sentiment.

Institutional Involvement & Economic Influence: Big-money players are increasingly shaping crypto market trends. Institutional investors – ranging from hedge funds and asset managers to corporations – have poured capital into Bitcoin and other digital assets, influencing both price and market structure. A prime example is MicroStrategy, the publicly-listed company led by Michael Saylor, which has aggressively accumulated Bitcoin as a treasury reserve. By mid-2025, MicroStrategy held about 629,376 BTC (nearly 3% of Bitcoin’s total supply) on its balance sheet[13], with continued purchases even above the $100K price level. This kind of corporate adoption, once unheard of, is now a bellwether for market confidence. Likewise, Grayscale – which operates the largest Bitcoin trust – signaled institutional demand by pursuing conversion of its trust into a spot ETF and even expanding into new crypto ETFs (e.g. filing for an Avalanche ETF)[14]. Traditional financial giants are also in the fray: for instance, Goldman Sachs reportedly expanded its Bitcoin holdings and investments in crypto ETFs[15], and BlackRock and others have filed for Bitcoin ETFs, reflecting Wall Street’s growing acceptance.

Weekly fund flow reports underscore this institutional impact. In mid-August, crypto investment products saw a record-breaking inflow of $3.75 billion in just one week – one of the highest ever – which pushed total assets under management in these products to an all-time high of $244 billion[16]. Notably, Ethereum-focused funds dominated those inflows (over $2.8B, ~77% of the total) as investors anticipated the network’s upgrades, while Bitcoin funds saw ~$552M in inflows[17][18]. However, by late August the trend flipped: outflows of $1.43B were recorded – the largest weekly withdrawal since March – as some institutions took profits and reacted to macro uncertainties[19]. Bitcoin funds suffered about $1B of those outflows in a week, whereas Ethereum proved relatively resilient with smaller outflows (~$440M)[20]. Analysts attributed the mid-August reversal partly to U.S. economic signals – early in the week, pessimism over Federal Reserve policy (concerns of continued tight monetary conditions) led to risk-off behavior and fund outflows[21]. Later in the week, a speech by Fed Chair Jerome Powell with a dovish tone helped sentiment recover, even spurring a modest $594M back into crypto funds[21]. This highlights how broader economic factors (inflation, interest rates, recession fears) are now tightly interwoven with crypto market movements.

Overall, institutional players (from companies like MicroStrategy to funds like Grayscale or ETF issuers) have added both liquidity and a degree of macro correlation to crypto. When economic optimism rises (e.g. expectations of looser monetary policy or hedge demand against inflation), we see increased institutional buying – which in 2025 helped drive Bitcoin to new highs as it is increasingly viewed as “digital gold” in portfolios[22][23]. Conversely, when global economic uncertainty or stricter monetary policy looms, these same players might pause allocations or even take some risk off the table, contributing to short-term price dips. Market sentiment gauges also show that inflationary pressures and fiat currency concerns (like unsustainable government deficits) have been a tailwind for crypto adoption as a hedge[24][23]. In summary, the global market trend in crypto is one of maturation: higher market capitalization, involvement of sophisticated investors, and sensitivity to economic cycles – all pointing to a market that is integrating with the wider financial system while still providing unique growth opportunities.

3. Technological Developments and Innovations

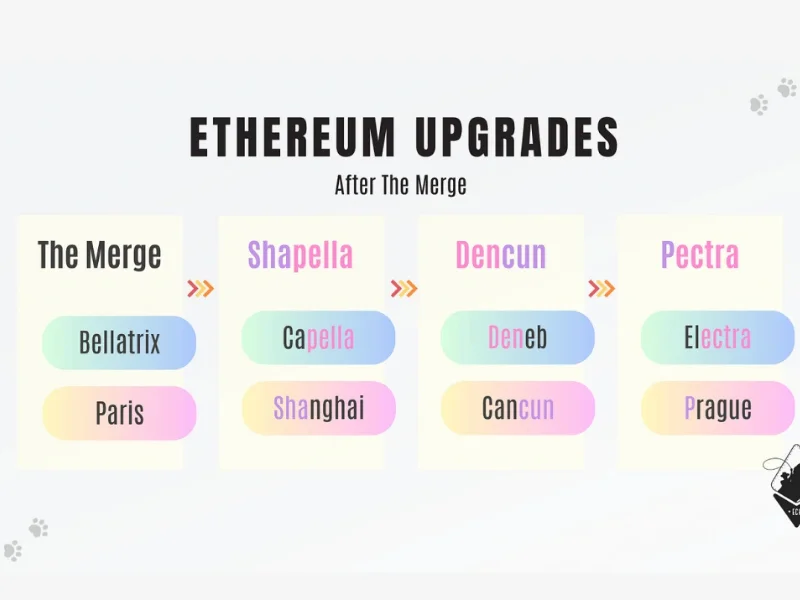

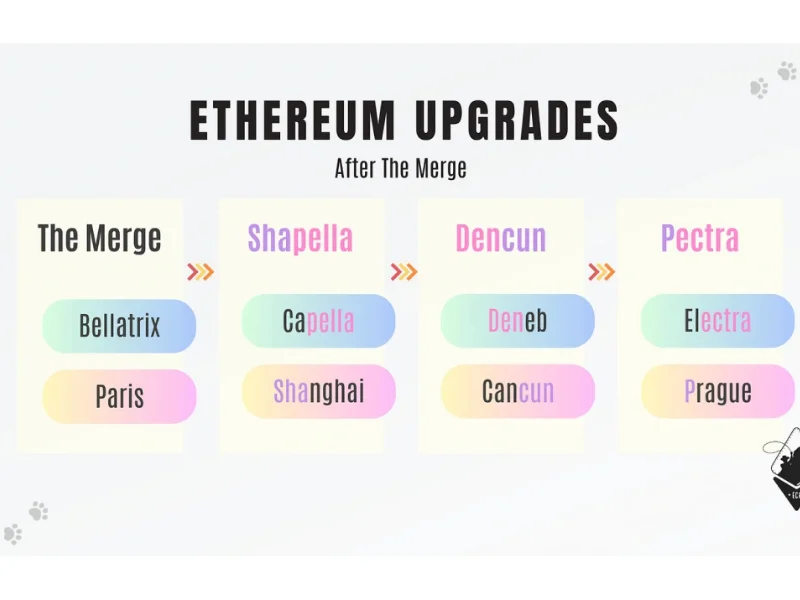

Blockchain Advancements: At the heart of the crypto industry’s evolution are continuous improvements in blockchain technology. A major theme has been scalability – increasing the number of transactions networks can handle, without sacrificing speed or security. In the past year, we’ve seen significant progress on this front. Ethereum’s long-planned transition to “Ethereum 2.0” (moving from Proof-of-Work to Proof-of-Stake consensus) was successfully completed with The Merge in late 2022, and subsequent upgrades have further improved the network. In 2023 and 2024, Ethereum introduced updates like the Shanghai upgrade (enabling staked ETH withdrawals) and, more recently, the Pectra upgrade in May 2025, which focused on efficiency and scalability. The Pectra upgrade improved Ethereum’s transaction throughput and user experience by making transactions faster and fees more predictable[25]. However, it also had nuanced effects on Ethereum’s on-chain economics – by making transactions more efficient, base fees have declined, reducing the amount of ETH “burned” (destroyed) and slightly decreasing the network’s deflationary pressure[26][27]. In other words, Ethereum’s supply is now expanding marginally (a modest 0.3% net annual inflation post-upgrade, versus being net deflationary when fees were very high)[27]. This trade-off was anticipated: better scalability often means lower fees, which is great for users and adoption even if it means validators rely a bit more on issuance than on fees as rewards.

To further address scalability, Ethereum’s roadmap includes sharding (parallelizing the network’s workload) and heavy reliance on Layer-2 solutions (like Optimistic and Zero-Knowledge rollups). Indeed, a big development is the rise of Layer-2 networks – such as Optimism, Arbitrum, zkSync, and Polygon’s zkEVM – which handle transactions off the main chain and periodically settle back to Ethereum. These L2s have exploded in usage, effectively increasing Ethereum’s overall capacity. In Q2 2025 alone, about $6.2 billion in net capital flowed into Layer-2 ecosystems[28] as users and developers seek lower fees and faster transactions. This shift has reduced congestion on Ethereum Layer-1, leading to much lower gas fees on the mainchain[26]. The long-term vision is that Ethereum Layer-1 becomes a secure settlement layer, while most day-to-day transactions happen on Layer-2 networks – combining scalability with the security of the base chain.

Beyond Ethereum, other blockchain protocols are pushing the envelope on performance. Solana is a prime example of a high-throughput chain leveraging a unique timestamping mechanism (Proof-of-History) alongside Proof-of-Stake. Solana aims to process thousands of transactions per second (TPS) on-chain, far above what Ethereum Layer-1 can do. In a recent stress test, Solana’s network briefly handled over 100,000 TPS – a milestone that no major blockchain had hit before[29][30]. Under normal conditions, Solana’s real transaction throughput is about 1,000 TPS (once you filter out validator voting messages and artificial load)[31][32], which still vastly outpaces Bitcoin (~7 TPS) and Ethereum (~15 TPS on L1). This performance has made Solana popular for certain applications like high-frequency trading and gaming. The network did face stability challenges in its early days (outages in 2021-2022 due to overload), but it has improved reliability in the past year. The fact that Solana’s DeFi ecosystem’s TVL climbed back to $10.7B (near its all-time high)[33] indicates renewed confidence in its technology. Other notable blockchain projects focusing on scalability and specialized use-cases include Avalanche, Algorand, and Polkadot (with its multi-chain sharding via parachains). Each is innovating on consensus algorithms and network design to strike the “trilemma” balance (decentralization, security, scalability).

In summary, the technological trend is clear: blockchains are getting faster and more efficient. Ethereum’s move to PoS and ongoing upgrades have reduced energy usage by >99% and set the stage for future throughput gains, while alternative Layer-1s like Solana show that speeds of 1k+ TPS are achievable with different architectures. Meanwhile, interoperability is improving – protocols and bridges now allow assets and data to move between chains more seamlessly than before, addressing the fragmentation issue. All these advancements are critical for blockchain tech to support mass adoption, as they lower costs and improve user experience.

Security Enhancements in Crypto: Alongside scalability, security remains a top priority in crypto tech development. High-profile hacks and exploits in previous years (especially in DeFi protocols and cross-chain bridges) have galvanized the community to innovate on security models. One major area of focus is decentralized security and auditing. Projects are increasingly using formal verification for smart contracts – mathematically proving the correctness of code – to prevent bugs. For example, some DeFi protocols now write critical contracts in Vyper or use tools like Certora and Solidify to rigorously test their code. We also see growth in bug bounty programs and decentralized insurance to mitigate the impact of any vulnerabilities that slip through.

A cutting-edge development in crypto security and privacy is the rise of Zero-Knowledge Proofs (ZKPs). ZKPs are cryptographic techniques that allow one party to prove a statement is true to another party without revealing any additional information. This seemingly magical capability has huge implications. On the privacy side, ZKPs enable things like proving your identity or credit score without revealing your personal data, or transacting on a blockchain without exposing amounts and addresses (think of projects like Zcash’s shielded transactions or Aztec network on Ethereum). On the scaling side, ZKPs power zk-Rollups, an L2 technology where a batch of transactions can be proven and compressed with a succinct proof posted to L1. Zk-rollups (like StarkNet, zkSync, Polygon’s zkEVM) can inherit Ethereum’s security while processing many transactions off-chain, making them a cornerstone of Ethereum’s scalability plans. Impressively, Ethereum developers are even planning an eventual Layer-1 integration of zk-EVM proofs to further optimize the base chain[34][35]. The momentum behind ZK tech is so strong that even standard-setting bodies have taken note: the U.S. NIST (National Institute of Standards and Technology) has an initiative to standardize zero-knowledge proof methods by 2025[36]. This standardization could accelerate enterprise and governmental adoption of ZKPs, ensuring these proofs are secure and interoperable across systems. The bottom line is that ZKPs are enhancing security (through privacy and robust math) across crypto applications, from protecting user data to enabling trustless scaling.

Another aspect of security is protecting smart contracts and funds from malicious actors. The industry has seen a shift toward multi-signature wallets, hardware security modules, and even experimental decentralized multi-party computation (MPC) wallets for both individuals and institutions to safeguard crypto assets. Protocols are also adopting decentralized governance safeguards – for instance, requiring time-locks and multi-step votes for any code changes, so that if a bad proposal passes, there’s time to react before it takes effect.

In the mining realm (for proof-of-work coins like Bitcoin), security comes from hashrate – and there, we’ve witnessed all-time highs in 2025. Bitcoin’s network hashing power exceeded 1 zettahash per second (ZH/s) for the first time in April 2025[37]. This means miners worldwide are computing an almost unfathomable 10^21 hashes per second. A higher hashrate makes the network more secure against 51% attacks and indicates robust investment in mining infrastructure. Interestingly, miner revenues per hash are near record lows due to high competition and Bitcoin’s lower block subsidy post-halving[38][39], but miners have become very efficient and are banking on price appreciation to compensate for thinner margins. The rising difficulty and hashrate show that Bitcoin’s proof-of-work security model continues to strengthen even as the block rewards shrink.

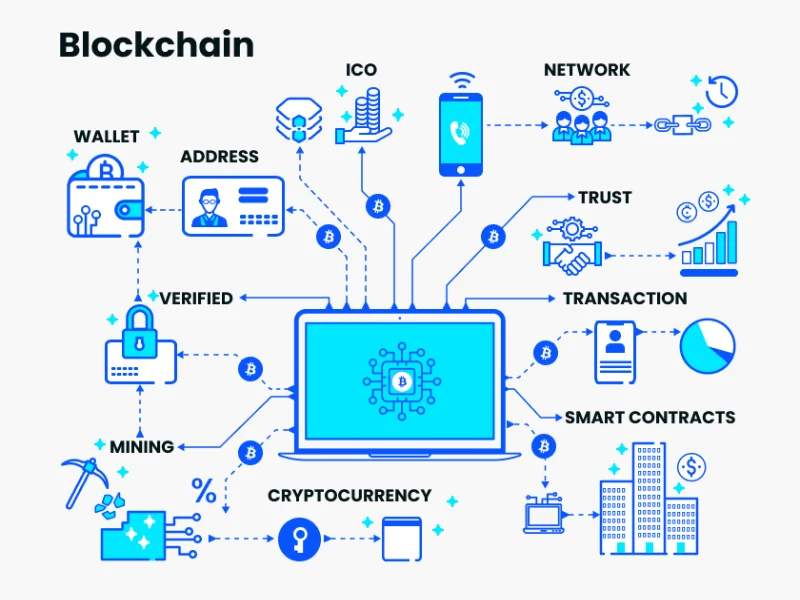

Impact of Smart Contracts and dApps: Smart contracts – self-executing code on blockchains – have unlocked an entire universe of decentralized applications (dApps) that are reshaping industries. One of the most transformative arenas has been Decentralized Finance (DeFi). Platforms like Uniswap (decentralized exchange), Aave (lending protocol), Curve (stablecoin swap), and Compound (money market) have grown into multi-billion dollar networks handling lending, borrowing, trading, and asset management without traditional intermediaries. DeFi effectively turned every user with a crypto wallet into their own bank/trader, and it has been expanding into new territory. In 2023–2025, we’ve seen DeFi protocols introduce more sophisticated financial instruments: options and derivatives (e.g., Dopex, dYdX), asset management vaults (Yearn, Enzyme), and even under-collateralized lending using on-chain credit scores or real-world asset collateral.

Importantly, DeFi is now bridging with traditional finance through tokenization of real-world assets (RWA). Projects are creating tokens that represent ownership in government bonds, real estate, or company equities, and these tokens can be used in DeFi protocols. This RWA trend means dApps might soon facilitate borrowing against, say, tokenized Treasury bills or trading tokenized stocks 24/7. It’s still early, but interest is strong because it combines DeFi’s efficiency with real-world value. Even centralized institutions are taking note – Goldman Sachs launched a digital asset platform, and multiple banks are experimenting with offering DeFi yields to clients, essentially acting as a front-end while the backend is a protocol like Aave or Compound.

Regarding usage metrics: the Total Value Locked (TVL) in DeFi is a common gauge of adoption. Crypto’s total DeFi TVL is in recovery mode – currently around $150–200 billion across chains (fluctuating with crypto prices), which is below the peak of ~$250B in late 2021 but significantly higher than just a few years ago. On Ethereum, despite ETH’s price hitting new highs, DeFi TVL has not yet surpassed its prior peak; it sits around $91B on Ethereum versus ~$108B at the 2021 peak[40]. This reflects some structural changes: more competition from other chains (like BSC, Solana, Avalanche) and more capital-efficient protocols that do more with less locked capital (e.g., Lido liquid staking has huge influence with relatively lower TVL since it issues liquid staked ETH). Additionally, many retail users who drove the DeFi Summer 2020 boom have not returned at the same scale, as evidenced by Ethereum’s DeFi usage in ETH terms (only ~21M ETH locked now vs 29M at the peak)[41]. Nonetheless, DeFi continues to evolve and eat into traditional finance use cases. Platforms like Uniswap v4 (proposed) are looking to add features rivaling centralized exchanges, and Layer-2 DeFi on Arbitrum, Optimism, and others is flourishing since transactions there are cheap and fast.

Outside of finance, smart contracts and dApps are expanding into other industries: for example, NFT marketplaces and games bring blockchain to digital art and collectibles; decentralized social media platforms (like Lens Protocol or the foreseen Twitter integration with crypto by some entrepreneurs) aim to give users control of their social identities; and supply chain management uses smart contracts for provenance tracking of goods. Another burgeoning area is decentralized autonomous organizations (DAOs) – essentially online, blockchain-governed cooperatives – which use smart contracts to manage membership and treasury funds. DAOs are investing in real-world assets, funding protocol development, and even serving as social clubs or philanthropic groups, all governed by token holder votes.

On-chain data from sources like Dune Analytics and Messari shows steady growth in dApp usage. For instance, daily active users on NFT platforms and blockchain games (particularly on chains like Polygon, Wax, and Solana) number in the hundreds of thousands. Unique addresses interacting with DeFi protocols have also cumulatively risen, indicating that while the hype cycles come and go, the base of users engaging with smart contracts keeps expanding. As of mid-2025, Solana’s daily active addresses (around 1 million) actually surpassed Ethereum’s (~0.5M) by a wide margin[42], thanks to popular Solana apps (especially those related to memecoins and gaming). This is a remarkable indicator of how newer networks optimized for certain use cases can onboard masses of users – even if many are light, frequent transactions – and it’s pushing the whole industry to accommodate millions of users in a decentralized way.

In summary, smart contracts are no longer a niche concept – they are running exchanges, lending platforms, games, media platforms, and more. This is shaping new industries by disintermediating traditional players and unlocking novel models (e.g., play-to-earn gaming, NFT-based memberships, algorithmic stablecoins). As we progress, expect the line between “crypto industry” and other industries to blur, with decentralized apps becoming just “apps” that people use, possibly without even realizing blockchain is under the hood.

4. Regulatory and Legal Landscape

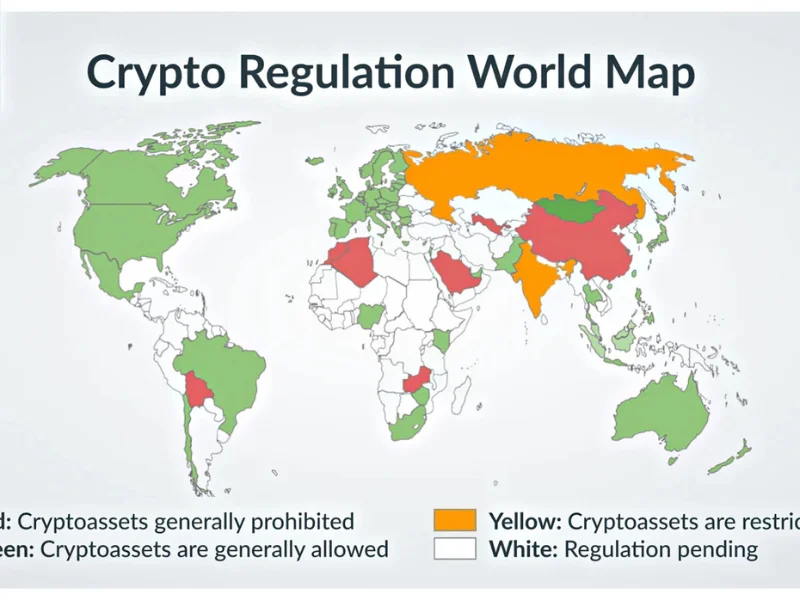

Current Regulatory Updates: The regulatory environment for cryptocurrencies has been dynamic and varies widely across the globe. In the United States, there’s been a notable shift between 2023 and 2025. Under the previous SEC leadership, the approach was often described as “regulation by enforcement,” exemplified by the Securities and Exchange Commission (SEC) launching high-profile lawsuits against major crypto exchanges like Binance and Coinbase in 2023. Those suits alleged that the exchanges operated unregistered securities platforms and listed tokens that should be regulated as securities. However, in 2025 the U.S. saw a change in administration and regulatory tone. In a surprising development, the SEC voluntarily dismissed its lawsuit against Binance in May 2025, with prejudice (meaning it cannot refile the case)[43][44]. Earlier, in February 2025, the SEC had also dropped its case against Coinbase[44]. These actions signaled a major policy pivot. The new SEC Chairman – Paul Atkins, appointed by President Donald Trump – indicated a preference to establish “clear rules of the road” for crypto through formal regulation rather than litigation battles[45]. The dismissal of the Binance case was hailed by the industry as a “landmark moment” and came with acknowledgement that innovation should not be stifled by unclear rules[46][47].

Now, U.S. regulators are working on concrete guidelines: both the SEC and the Commodity Futures Trading Commission (CFTC) have set up special crypto regulatory initiatives and “working groups.” Topics on the agenda include how to define and classify digital assets (security, commodity, or other), how to oversee stablecoin issuers (there’s bipartisan discussion on a stablecoin-specific law), and how to integrate crypto trading platforms into existing financial regulatory frameworks without crushing their operations. We’ve also seen movement in Congress – for example, proposals for a Digital Asset Market Structure bill and stablecoin regulations passed some committee hurdles, though final laws are still pending. Notably, the U.S. Federal Reserve and OCC are providing guidance for banks that engage with crypto, focusing on risk management and reserve requirements.

In Europe, a comprehensive regulatory framework has already been approved: the Markets in Crypto-Assets (MiCA) Regulation. MiCA was passed by the EU in 2023 and is in the implementation phase (phasing in through 2024 and 2025). This landmark law creates uniform rules across EU member states for crypto asset issuance and services. Under MiCA, companies offering crypto trading, custody, or exchange services will require a license (with prudential and consumer-protection requirements), and issuers of stablecoins (termed “asset-referenced tokens” or “e-money tokens”) have to meet strict reserve and reporting standards. By the end of 2024, parts of MiCA – like the rules for stablecoin issuers – kicked in, and by late 2025, the licensing regime for broader crypto service providers is taking effect[48]. Regulators like ESMA (European Securities and Markets Authority) have been preparing guidelines, and indeed by 2025 national regulators have started granting MiCA compliance licenses to exchanges and custodians. The MiCA approach is significant because it provides clarity and a single market across 27 countries, potentially making the EU a more straightforward jurisdiction for crypto business compared to the patchwork in the U.S.

The U.K., no longer in the EU, has been crafting its own path. The UK’s Financial Conduct Authority (FCA) initially took a very cautious stance – banning crypto derivatives for retail in 2021 and enforcing registration for any crypto businesses under anti-money laundering (AML) rules. In 2023–2024, the FCA introduced new marketing rules requiring clear risk warnings on crypto ads and banning incentives like referral bonuses to retail consumers. Compliance with these was spotty, and the FCA even had some firms temporarily halt UK promotions until they got it right. However, in a noteworthy development, by August 2025 the FCA decided to open up retail access to crypto-backed Exchange Traded Notes (ETNs) under certain conditions[49][50]. The FCA announced that retail investors will be allowed to buy crypto ETNs that are listed on approved exchanges (like the London Stock Exchange) – this reflects an understanding that the market has matured and “products have become more mainstream and better understood,” as an FCA director put it[51]. Protections (like adherence to financial promotion rules and absence of compensation scheme coverage) remain in place, but it’s a step toward a more permissive regime. The UK government is also working on broader crypto legislation to establish a regime for crypto trading platforms and stablecoins to be supervised like other financial services, possibly integrating them into the existing Electronic Money or Payment Services rules. In essence, the UK is trying to strike a balance between innovation and consumer protection, and is now signaling that with proper safeguards, retail crypto products can be allowed.

Elsewhere in the world, regulations vary: Asia presents a mixed picture. Japan has a fairly strict but clear framework (exchanges must be licensed and segregate customer assets; Japan was one of the first to legalize crypto as property and regulate exchanges after Mt. Gox). Singapore positions itself as crypto-friendly but with robust AML controls – it introduced licensing under the Payment Services Act and has been selective in approvals. Hong Kong made headlines in 2023 by opening up licensed retail crypto trading for certain large-cap tokens, marking a shift to rebrand Hong Kong as a crypto hub (with a licensing regime in 2024). China, of course, remains officially prohibitive on trading and mining, but their focus has been on the digital yuan (CBDC); many Chinese users still access crypto via OTC and offshore platforms in a gray market. Middle East: The UAE (particularly Dubai’s VARA) has set up a welcoming regulatory environment to attract crypto companies, issuing licenses to exchanges under clear rules.

Legal Cases & Precedents: The past couple of years have produced several legal precedents with broad implications. One of the most significant was the Ripple (XRP) case in the U.S. – in mid-2023, a judge ruled that XRP token sales on exchanges did not constitute securities offerings (since buyers didn’t have a reasonable expectation of profits tied to Ripple’s efforts for those blind exchange transactions), whereas XRP sales to institutional investors (with contracts) did qualify as securities offers. This split decision gave the crypto industry partial victory and clarity that many tokens, when sold to the general public, might not be deemed securities by the courts. It directly influenced the SEC’s approach and is likely why some enforcement cooled until rules are clarified.

Another big saga: Binance vs various regulators. Binance not only faced the SEC lawsuit (now dismissed)[52], but also enforcement actions elsewhere – e.g., the CFTC had sued Binance in early 2023 for offering illegal futures to U.S. customers. That case was on hold as Binance negotiated; and in late 2023, Binance and its founder Changpeng Zhao (CZ) were charged by the U.S. Department of Justice for AML violations. By 2024, CZ pleaded guilty to charges of willfully failing to implement AML programs and agreed to step down as CEO, with Binance paying hefty fines (over $4B)[53][54]. This was a watershed moment: one of the industry’s largest figures being held accountable, and it underscores that compliance is not optional if crypto businesses want to operate globally. The outcome sets a precedent that exchanges must have rigorous compliance or risk criminal consequences. Binance has since been restructuring and attempting to become more compliant (including possibly a change in leadership and operations).

Coinbase’s legal battles have also shaped the landscape. While the SEC’s case against Coinbase (for being an unregistered securities broker) was dropped[44], Coinbase scored a win in court compelling the SEC to respond to its request for clearer rulemaking (though the SEC basically said “not yet” in response). Coinbase has also actively engaged with policymakers, and its fate (being a U.S. publicly traded exchange) is a barometer for U.S. crypto regulation. So far, the trend suggests that regulatory clarity will eventually come through legislation or formal rules, rather than forcing a company like Coinbase out via court order.

In Europe, MiCA itself is the big legal framework, but we also see enforcement of AML: e.g., exchanges have to implement strict KYC and travel rule (transaction reporting) compliance. The EU’s Transfer of Funds Regulation now mandates that even unhosted wallet transactions above certain thresholds need info collected by service providers – a challenge for privacy advocates.

Precedents in other regions: India flirted with a crypto ban but settled on a heavy tax regime (30% tax on gains and 1% TDS tax on every transaction), which has dampened the market but not banned it. Russia, after initial hostility, is considering using crypto for cross-border trade to circumvent sanctions, illustrating how geopolitics can influence legal stances.

Overall, the legal landscape is trending toward integration of crypto into existing regulatory frameworks. The journey involves friction – like the SEC cases – but the recent U.S. policy shift suggests regulators want to craft bespoke rules (e.g., safe harbor for tokens, new definitions for crypto assets) rather than rely solely on applying 90-year-old securities laws. Meanwhile, clear frameworks like MiCA in the EU are setting a high bar for consumer protection and could become a reference model globally. For market participants, these developments reinforce the need to pay close attention to policy changes: a new law or enforcement action can significantly impact market sentiment and the viability of certain business models. On the bright side, the move toward clarity (licenses, guidelines) will likely encourage broader adoption by institutions that were waiting on the sidelines due to legal uncertainty.

5. Adoption and Market Sentiment

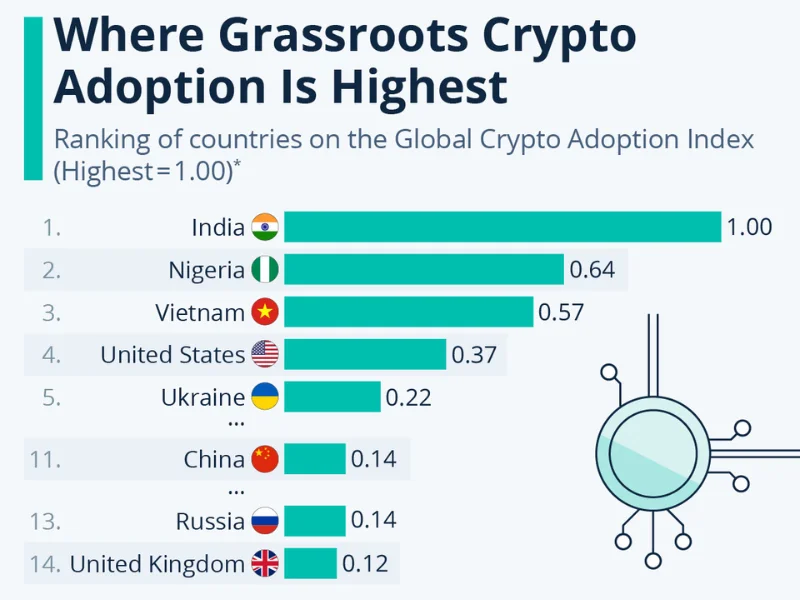

Retail and Institutional Adoption: Cryptocurrency adoption has grown significantly on both the retail (individual) and institutional fronts. On the retail side, global participation in crypto is at an all-time high. An estimated 560–600 million people worldwide now own some form of cryptocurrency[55] – roughly 7–8% of the world’s population – and this number continues to climb. In fact, 2024 saw a 172% surge in global crypto adoption, with particularly high growth in countries like India, Nigeria, and Indonesia[55]. In some nations with economic instability or currency controls, nearly 1 in 3 people have turned to digital assets as either an investment or a remittance tool[55]. This grassroots adoption is often driven by young, tech-savvy populations and by real-world utility: for example, people in inflation-hit economies using stablecoins for savings, or migrant workers using Bitcoin for cheaper cross-border transfers.

One prominent real-world adoption case is El Salvador. In 2021 El Salvador became the first country to declare Bitcoin legal tender, effectively conducting a nationwide experiment on crypto adoption. Two years on, the results are mixed but instructive. President Nayib Bukele touts the initiative as a “net positive” for the country – citing benefits like greater international branding, increased tourism, and foreign investment interest in El Salvador[4][56]. The move put El Salvador on the map as “Bitcoin country,” and indeed tourism spiked in 2022, and Bitcoin enthusiasts have been visiting or even relocating there (driving a mini tech sector). The government also claims to have a public crypto wallet (Chivo wallet) holding $400 million in BTC reserves[57][58], and they’ve launched Bitcoin-backed initiatives like volcano geothermal mining and proposed Bitcoin bonds. However, domestic adoption among Salvadorans has lagged. Surveys indicate that a large majority of Salvadorans rarely use Bitcoin for daily transactions – one 2023 poll found 88% of people hadn’t used Bitcoin that year despite the government’s push[59]. Many still prefer U.S. dollars (El Salvador’s other legal currency), and businesses report limited Bitcoin usage after the initial curiosity faded. The government even had to scale back a law that mandated all merchants accept BTC; under a new IMF-backed agreement, Bitcoin acceptance is now voluntary rather than compulsory for businesses[60][61]. So, while El Salvador’s experiment hasn’t (as skeptics warned) crashed the economy or caused financial instability – life goes on and the feared IMF sanctions didn’t materialize – it also hasn’t turned the average Salvadoran into a Bitcoin user overnight. It shows that even with national-level support, behavioral adoption takes time and perhaps more education or incentive. Other countries are watching this closely, and a few (like the Central African Republic) even tried their own version of legal tender status, though with limited success so far.

Apart from nation-level moves, retail adoption is evident in the proliferation of crypto wallets and user-friendly apps. Millions of people now have mobile wallets like Coinbase, Binance, or regional apps that allow them to buy, sell, and store crypto. Payment companies are integrating: you can use wallets like Cash App, PayPal, or Revolut to handle Bitcoin, and we see crypto debit cards in many countries. Digital wallet user counts keep rising – many of these people start by buying a small amount of Bitcoin or Ethereum as an investment, and gradually some experiment with DeFi or NFTs.

Institutional adoption has likewise accelerated. We’ve discussed how corporations (like MicroStrategy) and traditional financial institutions are involved, but to highlight sentiment: a Deloitte CFO survey in mid-2025 found a significant portion of corporate finance executives expect to be using crypto for routine transactions or reserves in the next few years[62]. Hedge funds and asset managers have also entered the space as an asset class – today, dozens of crypto-focused funds exist, and even stalwarts like BlackRock and Fidelity have either launched crypto products or made strategic investments (for instance, Fidelity offers Bitcoin in 401k retirement accounts on an opt-in basis, and BlackRock’s proposed iShares Bitcoin Trust ETF is pending approval). Pension funds and endowments – traditionally very conservative – have dipped their toes by allocating small percentages to venture funds or buying publicly traded crypto stocks (like Coinbase or Bitcoin mining firms). This institutional trickle could become a flood if regulatory clarity improves, as suggested by the Bitwise analysis that U.S. pension plan allocations could drive Bitcoin to $200k levels[63].

Another dimension of adoption is mainstream companies integrating crypto. Examples: Tesla famously bought $1.5B in Bitcoin (in 2021) and still holds a portion; fintech companies like Square (Block) derive significant revenue from Bitcoin sales; and merchants from Starbucks to Microsoft accept Bitcoin in some form (often via payment processors). More recently, stablecoins have seen adoption in commerce: Tether (USDT) and Circle’s USDC are widely used for B2B settlements in the crypto industry, and some merchants in Asia and Latin America accept USDT as an alternative to dollars.

In summary, retail adoption is broadening in geographic and demographic reach, while institutional adoption is lending credibility and stability to the market. Each reinforces the other: as more individuals use crypto, institutions see opportunity (more customers, new markets), and as more big players get involved, individuals gain confidence that crypto is “here to stay.”

Market Sentiment and Social Influence: Crypto markets are famously sentiment-driven. Emotions like fear and greed can cause outsized reactions – thus the popularity of the “Crypto Fear & Greed Index” which tracks sentiment from extreme fear to euphoria. After the harsh bear market of 2022, sentiment in 2025 turned bullish as prices recovered to new highs. Retail enthusiasm returned – evident in the resurgence of meme coins and vibrant chatter on social media – but with some caution after past lessons.

Social media (especially Twitter, now X) and online communities (Reddit, Discord, Telegram, YouTube) play a massive role in shaping crypto sentiment. Influential figures can move markets, at least for short periods. The most notorious example is Elon Musk: his tweets about Dogecoin and Bitcoin in 2021 sent those prices soaring or plunging. That dynamic persists – a single tweet or announcement from a key influencer can spark a mini buying frenzy or panic sell. In 2025, figures like Musk still comment (e.g., regarding integrating crypto into X or commenting on AI coins), but the market has grown larger, so such impacts are a bit more muted on the majors (less so on small altcoins). Additionally, crypto-native influencers – people like certain traders on Twitter, analysts at firms like Messari, or popular YouTubers (Coin Bureau, BitBoy, etc.) – have large followings that trust their analysis or calls, which can create self-fulfilling momentum in the short run.

Platforms like Reddit have dedicated crypto communities (e.g., r/CryptoCurrency with millions of members) where retail investors share news, memes, and sometimes coordinate (the way WallStreetBets did for stocks). Sentiment on these boards often reflects retail risk appetite – a flurry of positive posts and upvotes usually corresponds to bullish sentiment and vice versa. Analytics firms track this: for instance, Santiment monitors the frequency of crypto ticker mentions on social media and the positivity/negativity of the discourse. They noted that as Bitcoin hit new highs this year, Bitcoin’s social dominance (share of crypto chatter) spiked to historic levels[64], which can paradoxically be a contrarian indicator (extreme hype sometimes precedes a correction). Conversely, in bear phases, social engagement drops and sentiment becomes very bearish – often a sign of capitulation that savvy investors look for to start buying.

Another element is the emergence of influencer-led investment groups and platforms. Some well-known crypto personalities have launched their own tokenized communities or DAOs. For example, people have created social tokens (personal cryptocurrencies) that represent a brand or community following an influencer, granting holders special access or content. These can influence market sentiment too, as they gamify community engagement.

Messari and CoinCenter (a policy think tank) also contribute to sentiment not by hype but through education and advocacy. When these respected organizations put out reports (like Messari’s annual Crypto Theses or CoinCenter’s policy briefs), they help shape the narrative among serious investors and lawmakers. For instance, if Messari’s report is bullish on Web3 gaming or layer-2 adoption, it can tilt sentiment among institutional readers positively toward those sectors. CoinCenter’s advocacy for reasonable regulation can reassure the community that there are voices defending innovation in DC, indirectly boosting confidence.

One distinct trend in sentiment is the “mainstream-ification” of crypto news. Coverage on Bloomberg, CNBC, and other traditional outlets has increased. Bloomberg Crypto’s daily segment and Reuters crypto feeds give constant updates, meaning macro and traditional investors are also influenced by crypto sentiment now. Headlines like “Bitcoin breaks $100k” or “Major bank offers crypto custody” on mainstream media bring in waves of new interest or trust.

Market sentiment indicators: We have on-chain ones like Nansen’s Smart Money indices – e.g., Nansen’s Stablecoin Risk Appetite Indicator measures what percentage of smart money wallets are in stablecoins versus deployed in crypto investments[65][66]. When it’s high (lots of stablecoin holding), it indicates a risk-off (bearish) sentiment; when it falls below a threshold (meaning smart money is deploying capital into crypto), it’s a bullish sign of increasing risk appetite[67][66]. As of mid-2025, that indicator has signaled improving risk appetite as smart money reduced stablecoin holdings during the bull run, but it hasn’t hit extreme lows (suggesting some caution remains and plenty of dry powder available). We also have the traditional fear/greed index (which aggregates volatility, volume, social, Google trends, etc.) – it hovered in “Greed” territory for much of early 2025, occasionally tipping to “Extreme Greed” during big rallies, and then cooling off to neutral on pullbacks.

Finally, psychology patterns in crypto tend to repeat: early bull phase optimism, mid-bull euphoria with many believing “this time is different” and everyone is a genius trader, then a sharp correction that reminds people of risk, etc. By staying aware of these patterns and using sentiment tools, seasoned investors try to do the opposite of the crowd (buy when fear is high, take profits when greed is rampant). For newcomers, the community always emphasizes educating oneself and only investing what one can afford to lose, because sentiment can turn quickly on negative news or if a bubble forms and bursts.

In conclusion, crypto adoption is steadily increasing both at retail and institutional levels, and market sentiment – heavily influenced by social media and macro trends – can amplify price movements. The interplay of new users entering, big players adopting, and the hive-mind of social networks creates a unique environment where narrative and data are both king. Those who actively track community sentiment (on Twitter, Reddit, etc.) alongside on-chain and market indicators can gain an edge in anticipating the market’s emotional swings.

6. On-Chain and Blockchain Activity

Tracking On-Chain Activity: One of the advantages of public blockchains is that a wealth of data is available for analysis – often in real time – to gauge the health and usage of the network. These on-chain metrics serve as fundamental indicators, analogous to economic indicators in traditional finance. Key metrics include transaction volume, active addresses, hash rate (for PoW chains), staking participation (for PoS chains), and more.

On-chain analysis firms like Glassnode, CryptoQuant, and Nansen compile these metrics to derive insights. For example, active addresses represent the number of unique blockchain addresses sending or receiving transactions in a given period – a proxy for how many users (or at least addresses) are active. In Bitcoin’s case, active addresses have been trending upward. As of August 2025, roughly 700k–800k Bitcoin addresses are active daily[68][69], which is a notable increase (Glassnode reported about a +8% uptick to ~793k around mid-August)[68]. This suggests growing participation, possibly due to new users and also expanding usage via second-layer solutions (e.g., the Lightning Network, although those transactions aren’t directly on-chain) and Ordinals inscriptions (Bitcoin’s pseudo-NFTs) which briefly spiked usage. Similarly, transaction fees on Bitcoin spiked by ~10% week-over-week in that same mid-August period[68], implying higher demand for block space – usually a result of increased activity or congested periods[69]. Rising fees can indicate the network is very much in use (and willing to pay for priority), though extremely high fees might also price out some users. Currently, Bitcoin’s fees are moderate except during brief surges; Ethereum’s fees have been consistently lower than in previous cycles thanks to L2s, except for when an NFT craze or memecoin trading clogs the network.

Another major on-chain metric is total transaction volume (the total value transacted on the blockchain). High transaction volumes can reflect greater economic activity – e.g., bull markets often see on-chain volumes swell as more value moves between investors (for buying, selling, arbitrage, etc.). In 2025, adjusted on-chain volume for Bitcoin and Ethereum has risen compared to the bear market lull, though interestingly, some of that activity has migrated to L2s or alternative chains. For Ethereum, if you include L2 transactions, the “real” transaction count and volume hitting the network ecosystem is at record highs (multiple millions of tx per day across L1 + L2).

Mining activity and hash rate are another vital sign for proof-of-work chains. As mentioned, Bitcoin’s hash rate reaching all-time highs (~1 ZH/s)[37] is extremely bullish from a security standpoint – more hashing power means the network is more resilient against attacks and underscores miners’ confidence (they’re investing in more machines because they expect long-term profitability). The network difficulty adjustments have also hit records to keep block times steady[70][71]. Mining geographic distribution has improved since China’s 2021 ban; now the U.S., Middle East (Kazakhstan), and others have significant shares. High hash rate doesn’t directly influence price short-term, but it often correlates with miners’ positive outlook. In contrast, if hash rate were dropping significantly, it could signal miner capitulation (often in bear markets) which can pressure prices as they might sell off holdings to stay afloat.

For proof-of-stake networks like Ethereum post-Merge, staking metrics are analogous to hash rate. The percentage of ETH staked, number of validators, and staking yield are tracked. Ethereum now has over 26 million ETH staked (about 20%+ of total supply) in its Beacon Chain, with hundreds of thousands of active validators. A high and rising stake participation indicates many holders are locking up their ETH to secure the network (and earn yield ~4-5%), reflecting trust in the protocol. After the Shanghai upgrade allowed withdrawals, there was a fear of mass unstaking, but in reality net staking has grown – a sign that Ethereum’s PoS is stable and attractive to participants.

On-Chain Indicators & Market Health: Analysts often look at ratios like MVRV (Market-Value-to-Realized-Value), which compares market cap to the aggregated cost basis of coins (realized cap). In early 2025, Bitcoin’s MVRV went above 1 (bullish zone) and even heated near levels that in past cycles indicated a top was forming, but it cooled off a bit after the recent correction. Percent supply in profit is another indicator (the share of coins whose current price is above the price at which they last moved). Currently, about 94% of Bitcoin supply is in profit[72][69] – meaning only 6% of coins were acquired at higher prices than today, which are basically those bought at the very peak. Such a high profit ratio is a double-edged sword: on one hand it affirms the strength of the rally (almost everyone is “in the money”), on the other hand it raises the risk of profit-taking – some holders might decide to realize gains, which could increase selling pressure[72][73]. In fact, Glassnode flagged that historically when >95% of supply is in profit, markets are near euphoric and vulnerable to pullbacks[72][74]. So these metrics help investors gauge where we are in the cycle.

Liquidity and Market Movements: Liquidity refers to how easily assets can be bought or sold without causing large price impacts. In crypto, liquidity comes from both centralized exchanges (CEXes) order books and decentralized finance liquidity pools. Over the past year, market liquidity has generally improved for the major cryptocurrencies. Data providers like Kaiko report that order book depth for BTC and ETH on major exchanges is at or near all-time highs[75] (meaning you can execute larger orders now with minimal slippage compared to a few years ago). This is partly due to more participation from market makers and the entrance of institutional market-making firms (some migrated from traditional markets to crypto or expanded operations). For example, a billion-dollar sell order of BTC, which a few years ago could have crashed the price 5-10%, might now move the market a smaller percentage because buyers are quicker to step in and there’s more resting depth on order books[75].

However, liquidity can still fragment and vanish in smaller cap tokens or during extreme volatility events. We saw a mini “liquidity crunch” during a flash crash in August 2025 when a whale sold a huge amount of BTC on a weekend – liquidity was thinner and prices swung harder (BTC dropped a few percent in minutes causing liquidations). After such events, liquidity often rebounds as arbitrageurs and market makers rush in to take advantage of spreads[76][75]. Exchanges like Bybit and OKX that had lost some market depth post-FTX collapse in 2022 have since recovered a lot of that depth within 30 days during stable market conditions[77][78].

In DeFi, liquidity pools tracked by DeFiLlama show that major DEXes like Uniswap, Curve, and PancakeSwap collectively hold tens of billions in liquidity. This allows fairly large swaps on-chain with moderate slippage, especially for pairs like stablecoin-to-stablecoin or WETH-WBTC. The total TVL (Total Value Locked) across DeFi is an aggregate measure of liquidity; it currently hovers around ~$180B (depending on price changes) with Ethereum’s ecosystem making up half or more of that. Notably, liquidity is spreading out: layer-2 networks and alternative L1s collectively now host a significant chunk (Arbitrum alone has ~$10B TVL, BSC around $6-7B, etc.). This multi-chain liquidity means the market is less concentrated on one chain, but also requires aggregators for best execution (projects like 1inch and Thorchain facilitate cross-exchange and cross-chain liquidity usage).

Liquidity crunch risks still exist. For example, stablecoin liquidity is critical – a lot of traders park value in stablecoins between moves. The combined stablecoin market cap (~$282B across USDT, USDC, BUSD, DAI, etc.)[79] acts as the dry powder of the crypto market. If trust in a major stablecoin wavers, liquidity can evaporate as people flee to fiat or other assets (as seen when Terra’s UST collapsed in 2022). In 2025, stablecoins like USDT and USDC have maintained their pegs robustly; in fact, stablecoin usage is huge in emerging markets for everyday commerce and savings, augmenting crypto liquidity globally by effectively importing dollar liquidity into crypto rails.

Platforms like Kaiko also introduce indices to rank liquidity of different crypto assets, aiding institutions in knowing what’s reasonably tradeable. As of now, beyond BTC and ETH, coins like XRP, SOL, BNB, and ADA also have deep liquidity – important for those looking beyond just the top two assets.

In terms of market movements, liquidity is what can dampen or exacerbate price swings. When liquidity is high and order books are thick, large buy or sell orders can be absorbed without much slippage, leading to smoother price action. When liquidity is low (e.g., weekends or during a panic when market makers pull bids), even modest orders can move price a lot, causing sharp spikes or drops. Crypto still faces the phenomenon of liquidity drying up during extreme fear – for instance, a rapid 10% drop can cascade into a 20% drop if order books thin out and leveraged positions start liquidating (since forced selling adds to downward pressure). The industry’s answer to this is twofold: more on-chain transparency (to see these liquidations and gauge when they might end) and circuit breakers or safeguards on some exchanges (though not widely implemented yet in crypto).

Finally, on-chain liquidity metrics – like exchange inflows/outflows – are closely watched. When a lot of BTC is flowing into exchanges, it can imply potential sell pressure (investors moving coins to sell) whereas large outflows often signal accumulation (coins being moved to cold storage). In 2025, we saw a trend of net outflows from exchanges during bullish periods, indicating hodlers pulling their assets into long-term storage as prices rose (a bullish sign), and brief spurts of inflows during corrections (as traders deposited coins to perhaps take profit or add collateral). For example, during the run to $100k, exchange BTC balances hit multi-year lows – investors were not rushing to sell, which helped sustain the rally.

In summary, on-chain and liquidity indicators provide a nuanced real-time pulse of the crypto market. They tell us not just what the price is, but why it might be so – e.g., whether a rally is accompanied by robust network activity (healthy sign) and whether whales/exchanges are accumulating or distributing. Right now, those indicators show strong network utilization (active addresses up, high hash rate, lots of staking), robust liquidity (especially in majors and via stablecoins), but also caution signs like high profits (risk of some sell-off) and macro sensitivity. For a savvy investor, keeping an eye on Glassnode dashboards or DeFiLlama charts is as important as reading price tickers – it’s like reading the blockchain’s heartbeat.

7. Emerging Trends and Future Outlook

NFT Growth and Impact: The NFT (Non-Fungible Token) market has undergone a rollercoaster of hype and correction, but it continues to be one of the most influential trends in the crypto space. After the explosive growth in digital art and collectibles in 2021 (when names like Beeple and Bored Apes made mainstream headlines), NFT activity cooled significantly in 2022 with the bear market – trading volumes dropped and many speculative projects lost value. In fact, sobering data indicates that over 90% of early NFT projects have effectively “died” (inactive communities, near-zero trading) by late 2024[80]. However, this period also flushed out the junk and allowed serious builders to refocus on utility and community. By late 2024 and into 2025, we saw a resurgence of NFTs – sometimes dubbed an “NFT Renaissance” – albeit in a more mature form[81].

Notably, the blue-chip NFT collections that survived the downturn (such as CryptoPunks, Bored Ape Yacht Club, Azuki, Pudgy Penguins) have regained spotlight and value. CryptoPunks, for example, cemented itself as a digital cultural icon (with a collective market value over $1.4B)[82]. These established communities doubled down during the bear market, building brand collaborations, games, or simply strengthening their member loyalty. Now, with crypto markets rising again, NFTs stand to benefit from renewed liquidity and interest. Floor prices of many top collections have been climbing in 2025, although they haven’t all hit previous highs yet – indicating room for growth if the bull market continues.

More importantly, NFTs are evolving beyond just static collectibles. Real-world utility and big-brand adoption are expanding NFT use cases. For instance, NFTs are increasingly used in gaming (as in-game items or characters that players can truly own and trade), in music (artists releasing albums or rights via NFTs), and in ticketing (event tickets as NFTs to verify authenticity and enable post-event collectibles). One standout example: Sony has filed patents indicating plans for NFT integration in PlayStation gaming, specifically exploring interoperable NFTs that could represent in-game assets usable across multiple games/platforms[83]. This is a big deal – imagine earning a special sword in one game and carrying it to another game because it’s an NFT in your wallet. If major gaming companies implement this, it could bring tens of millions of gamers to use NFTs without even realizing it’s blockchain under the hood.

Major brands are also leveraging NFTs for marketing and customer engagement. We’ve seen fashion and luxury brands like Nike, Adidas, Gucci issue limited edition NFTs tied to physical products (sneakers with NFT counterparts proving ownership or granting perks). Pudgy Penguins, a popular NFT collection, struck partnerships with traditional retailers: they launched physical toys in Walmart and Target that come with QR codes linking to NFTs[84], effectively creating a fun onboarding for kids and collectors from toy aisles to blockchain. This phygital (physical+digital) model showcases how NFTs can break into the mainstream via familiar retail experiences. Forbes has experimented with NFT-based subscriptions and membership content[85], pointing toward media companies using NFTs to cultivate loyalty (like token-gated articles or special NFT-holder events). Additionally, tokenizing real-world assets is starting to overlap with NFTs in the form of digital collectibles for real estate, art or wine – e.g., buying an NFT that represents a share of an expensive wine cask or a luxury car.

From a regulatory standpoint, the U.S. seems to be warming up to NFTs as well – with more clarity that many NFTs are collectibles or digital goods rather than securities, experimentation is safer. The change in SEC leadership to a more crypto-friendly stance[86] means projects aren’t as fearful that releasing an innovative NFT might draw regulatory ire, spurring a wave of creative models like dynamic NFTs (which can change properties over time or with certain conditions) and token-gated communities (where holding an NFT grants access to exclusive experiences or chats). Indeed, a prediction is that under clearer regulations, we’ll see NFT projects offering richer utility – for example, an NFT that acts as your membership pass to a global co-working space network, or VIP access at conferences[87][88].

Looking forward, NFTs appear poised to move further into the mainstream consciousness. The notion of digital ownership is being normalized. Many expect the next big NFT wave to be driven not just by art, but by industries like gaming, sports, and music (where fans value verifiable ownership and limited editions). If Web3 gaming finally produces a hit game where NFT ownership is crucial, that could onboard millions. Likewise, in sports, think of ticket stubs as NFTs or player trading cards on blockchain – some of that is already happening (NBA Top Shot was an early success, and more leagues are exploring it). Even governments are dabbling – e.g., some city governments have issued NFT certificates for things like land registries or company licenses as an immutable record.

In summary, NFTs in 2025 are in a renaissance: the hype excesses were pruned, leaving a field ripe for genuine innovation. They are impacting digital art/collectibles, but also branching into tangible sectors like retail, loyalty programs, and gaming. As they gain functionality and real-world connections, NFTs could drive the next big wave of crypto adoption by engaging mainstream users in ways they value (collecting, gaming, membership). We can expect NFT trading volumes – which recovered from ~$50M/week in late 2024 to ~$175M/week by year-end[89] – to continue growing, potentially challenging the highs of 2021 if the broader market stays strong and new use cases catch fire.

DeFi’s Continued Evolution: Decentralized Finance is steadily transforming from an experimental playground into a competitor (and complement) to traditional finance. The early DeFi products (DEXes, lending, etc.) have now been battle-tested and improved in terms of security and efficiency. Uniswap, for example, is on its 4th iteration with features like concentrated liquidity that greatly enhance capital efficiency (meaning liquidity providers can achieve the same depth with less capital by focusing it in certain price ranges). Aave and Compound have introduced new services like permissioned pools for institutions, and collateral types that include real-world assets.

A major trend in DeFi is integration with TradFi. We see this in multiple ways:

- Institutional DeFi: Platforms like Aave Arc create whitelisted environments where KYCed institutions can participate in liquidity pools with known counterparties, satisfying their compliance requirements while enjoying DeFi tech. Big banks are also dipping in – J.P. Morgan executed a DeFi trade on Polygon as part of a pilot, using a modified Aave pool for foreign exchange transactions, marking one of the first instances of a major bank using DeFi rails.

- Tokenization of real-world assets (RWAs): DeFi is no longer limited to crypto-native collateral. Projects such as MakerDAO have started to include tokenized treasury bonds and real estate loans as collateral backing the DAI stablecoin. There are now DeFi protocols specializing in RWAs (e.g., Goldfinch for real-world credit, Centrifuge for invoices and trade finance). This brings stable yield from outside crypto into DeFi, which can attract more conservative capital. It’s projected that by 2030, trillions of dollars of real-world assets could be tokenized, and DeFi would be a natural venue for trading and lending against them.

- Advanced financial instruments: The DeFi space of 2025 offers pretty much every service traditional finance does, albeit at smaller scale so far. There are decentralized options exchanges (Dopex, Lyra), perpetual futures platforms (dYdX, GMX), structured products (Ribbon Finance for yield strategies), and insurance (Nexus Mutual, which covers smart contract risks, and others expanding into covering stablecoin depegs or even real-world events in a decentralized way). The continued evolution will likely refine these products and perhaps connect them. For example, one can envision a fully decentralized portfolio management system where an NFT represents a basket of assets managed by an algorithm or a DAO, functioning similarly to an ETF.

- Cross-chain and Interoperability: DeFi is expanding across multiple chains, leading to demand for fluid movement of assets. The rise of cross-chain bridges and interoperability protocols (like Cosmos IBC or Polkadot’s parachains) is making it easier for liquidity to not be siloed. In practice, this means a user might use an aggregator like LI.FI or THORChain to swap assets across different chains’ DEXes in one click, or provide liquidity in a pool that spans chains. As this improves, DeFi becomes chain-agnostic – users won’t need to know or care which chain they’re on as much, focusing instead on best rates and uses.

As DeFi continues to evolve, one challenge and opportunity is user experience. Projects are working on smoother interfaces, human-readable wallet names (via ENS or Unstoppable Domains), and integrating with traditional fintech apps. The hope is that users will use DeFi dApps as easily as they use a mobile banking app today. There’s progress: some non-crypto companies like Reddit implemented a form of DeFi (Community Points on Arbitrum) with an interface that hides the blockchain bits for everyday users.

In the near future, we might see DeFi and NFTs merge – e.g., NFTfi (using NFTs as collateral for loans) becoming more popular, or fractionalized NFTs trading on DEXes. And with Ethereum’s upcoming sharding and proto-danksharding (data availability improvements), the capacity for DeFi on Layer-2s will further expand, lowering costs and enabling potentially high-frequency trading or on-chain gaming economies that were previously impractical due to gas fees.

Stablecoins and CBDCs: Stablecoins have become a crucial piece of the crypto (and even global) financial system. By providing a digital asset that’s (relatively) stable in value, they bridge the gap between volatile cryptocurrencies and fiat money. The market cap of major stablecoins like USDT (Tether) and USDC (Circle) has held strong, and new entrants like USDP (PayPal’s USD stablecoin) launched in 2023 show that even fintech giants see opportunity in this space. Stablecoins facilitate everything from trading (they’re the base pair for most crypto trades now, replacing USD on many exchanges) to remittances and yield farming in DeFi.

A significant trend is stablecoin growth outside the US and in emerging markets. In countries with currency inflation or strict capital controls (e.g., Argentina, Turkey, Nigeria), people increasingly use dollar-pegged stablecoins as a store of value and medium of exchange. This grassroot demand has led to situations like USDT occasionally trading at a premium in those local markets when demand is high. Some governments are wary because it can reduce the usage of the local currency – essentially citizens dollarizing via crypto rails. For instance, Lebanon and Venezuela see a lot of stablecoin usage after hyperinflation eroded trust in local money.

In response to stablecoin proliferation, many central banks accelerated their exploration of Central Bank Digital Currencies (CBDCs). A CBDC is a digital version of a country’s fiat currency, issued and backed by the central bank, potentially using blockchain or similar tech. According to the BIS survey in 2024, 91% of central banks were engaged in some form of CBDC work[90], and over a third had accelerated their efforts due to the rise of stablecoins and crypto[91]. By 2025, we have a few live retail CBDCs: China’s Digital Yuan (e-CNY) is in advanced pilot across many cities (with millions of users), the Eastern Caribbean has DCash, Nigeria has the eNaira, and countries like Sweden (e-krona) and South Korea are testing. India’s digital rupee pilot is ongoing and reportedly growing (with a small but increasing amount in circulation)[92]. The European Central Bank is working on a digital euro, expected around 2027 if approved – they are currently in consultation phases focusing on design that preserves privacy for small transactions. The U.S. is more cautious; the Fed has researched a digital dollar (Project Hamilton) but there’s political and banking sector pushback, so they’re in “study mode” and indicating no CBDC will launch without Congress approval.

The interplay between stablecoins and CBDCs is interesting. Many central banks view the widespread use of private stablecoins as a potential risk to monetary sovereignty (hence why some accelerated CBDC plans). We might see regulations requiring stablecoin issuers to be banks or to hold very high quality reserves; already in the US, proposals suggest treating stablecoin issuers like insured depository institutions. Meanwhile, stablecoins themselves are innovating: algorithmic stablecoins largely failed (Terra’s collapse being the cautionary tale), so focus is back on fully reserved models. Circle introduced more transparent attestation and is aiming to register under anticipated stablecoin laws. Tether, after years of opacity, has reduced risk by cutting commercial paper and holding mainly Treasury bills now.

One can foresee a coexistence: CBDCs might handle domestic needs (a digital cash replacement for citizens), whereas stablecoins (especially USD-pegged) might remain popular for global crypto trading and as a dollar access point in economies with weak currencies. In any case, both represent the digitization of money.

From a user perspective, a CBDC could make payments very efficient – imagine instant settlement, no need for physical cash or even cards. But it also raises concerns over privacy and government surveillance of transactions. Some designs propose privacy tiers (small payments anonymous like cash, larger ones traceable).

An IMF report recently even discussed a platform for multi-CBDC interoperability, envisioning a future where many CBDCs operate on compatible standards for seamless cross-border transfers[93]. That suggests a global approach to avoid fragmentation.

In the crypto industry, a big question is: if CBDCs become common, do they compete with or complement crypto? On one hand, a U.S. digital dollar could reduce the need for USDC/USDT. On the other, CBDCs likely won’t have the same programmability and permissionless use that crypto folks desire (a Fed CBDC probably wouldn’t be usable in DeFi protocols without restrictions). Thus, private stablecoins might still thrive as more open alternatives, possibly regulated similarly to money market funds.

In conclusion, stablecoins have solidified their role as a linchpin in crypto markets (and beyond), essentially serving as the bridge currency and a safe harbor in volatility. CBDCs are the state’s answer to not lose relevance in the age of digital money, and their rollout will be one of the major financial stories of the coming few years. Both trends point toward an increasingly digital, tokenized form of money for everyday use, aligning with the broader crypto vision that value should move as seamlessly as information does on the internet.

8. Investor Insights and Sentiment Analysis

Investor Behavior Patterns: The behavior of crypto investors has been evolving as the market matures and new types of participants enter. In the early days, the market was dominated by retail enthusiasts and “whales” from the crypto-native community. Now, with hedge funds, family offices, and even algorithmic traders in the mix, we see a broader spectrum of strategies and psychology at play.

One noticeable pattern is how investors react to volatility compared to previous cycles. In 2025, many retail investors are more battle-hardened – those who lived through the 2018 crash or the 2021–22 drawdown are less likely to panic sell at the first sign of a 20% dip. The concept of HODLing is well ingrained, and on-chain data confirms that a large portion of Bitcoin’s supply is held by long-term holders (LTHs). Glassnode metrics show that coins dormant for 1+ year are near all-time highs, meaning hodlers didn’t significantly reduce their positions even when new peaks were hit. These LTHs provide a sort of anchor to the market, as they act as strong hands not easily shaken out by FUD (fear, uncertainty, doubt). In contrast, short-term holders (recent buyers) tend to have more influence on short-term price moves as they’re more prone to trade on emotion or momentum.

Psychologically, crypto investors often swing between greed and fear faster than in traditional markets due to the 24/7 trading and constant news cycle. Tools like the Fear & Greed Index quantify this, and indeed we saw it reach Extreme Greed levels during the big rallies of early 2025 and drop to Fear during corrections. Behaviorally, during periods of extreme greed, we see phenomena like: new coin offerings getting oversubscribed, meme coins rallying 1000% in days (as happened with a coin like PEPE in 2023 and similar ones in 2025), and investors taking on high leverage expecting quick gains. Experienced traders often start reducing risk when euphoria is rampant. Conversely, during extreme fear, casual investors abandon the market (“crypto is dead” sentiments on social media spike), which ironically can be a good entry point for contrarians.

Santiment and other analytics firms track things like the ratio of bullish vs bearish mentions on social platforms. For example, Santiment noted that when Bitcoin social dominance spiked above 40% and sentiment was overly bullish, a correction followed[64] – a sign of potential overconfidence. They also warned when e.g. many were expecting a Fed pivot and getting euphoric, to be cautious[94].

Investor cohorts differ: Retail often chases rallies (momentum buying) and sells in panic, whereas many institutions and whales do the opposite (accumulate when prices are down or range-bound, and take profits into strength). A striking illustration was the 2022–2023 period: on-chain analysis showed strong accumulation wallets (likely institutional or OG whales) were buying heavily around the $16k–$30k zone when retail interest was low. By 2025, those accumulated coins are deep in profit.

Another behavior change is portfolio diversification. Early crypto investors might have held mainly Bitcoin and a couple altcoins. Now, with thousands of tokens and sectors (DeFi, NFTs, metaverse, layer1s, layer2s, etc.), investors are more diversified or specialized. Many retail investors hold a basket of top 10 or top 20 coins to spread risk. Institutions often focus on Bitcoin and Ethereum (viewing BTC as digital gold, ETH as a Web3 investment) – indeed Bitcoin dominance is still ~50-55%[79] in part because institutions favor it. But some are venturing into higher-yield opportunities like providing liquidity in DeFi or venture investing in upcoming protocols.

Investors have also become more cautious and strategy-oriented post several boom-bust cycles. Concepts of risk management that were perhaps ignored during the 2017 ICO craze or 2021 meme frenzy are taken more seriously now. For instance, using stop-loss orders, setting take-profit levels, and not going all-in on a single coin are more common practices even among retail (helped by the abundance of educational content). The rise of derivative platforms has also allowed sophisticated investors to hedge – e.g., if they hold a large portfolio of altcoins, they might short Bitcoin or Ethereum futures as a hedge during uncertain times, knowing that in a downturn correlations spike and that can offset some losses. We saw evidence of this with Bitcoin’s futures open interest hitting highs and options markets maturing (Bitcoin options now have fairly liquid markets for hedging big moves).

Risk Management in Crypto Investments: Given crypto’s notorious volatility – double-digit percentage swings in a day are not unusual – risk management is crucial. We have observed several strategies and trends:

- Stablecoin Allocation: Many investors keep a portion of their portfolio in stablecoins (USDT/USDC) as a way to manage risk. This allows them to earn yield (through DeFi lending or staking) and have dry powder to buy dips. Nansen’s stablecoin indicator essentially measures this – in risk-off times (like May 2022 crash), smart money raised stablecoin allocations above panic thresholds (~16%)[65][67], and when they feel a bottom is in, they redeploy (indicator falls below ~11% “risk on” threshold)[67][66]. Currently, many investors still keep a decent stablecoin reserve given macro uncertainties, instead of being 100% in crypto as some might have been during euphoric phases.

- Using Derivatives for Hedging: The availability of futures, perpetual swaps, and options on Bitcoin, Ether, and even other large caps means investors can hedge downside. For instance, an institutional holder of a large Bitcoin position can buy protective put options (like buying insurance). The cost of this (the option premium) is something they factor into returns. In 2025, the Bitcoin options market has grown (open interest and volumes are up) and products like Bitcoin volatility index (DVOL) are emerging[95], giving a sense of implied volatility and risk pricing akin to the VIX in equities. We also see structured products like covered calls being popular – selling call options to earn yield on Bitcoin holdings, which essentially caps upside for guaranteed income (a strategy that became common when markets were range-bound).