1) Introduction

Purpose of the article

This report gives you a clear, data-driven read on crypto market sentiment right now—what’s moving prices, how on-chain behavior is shifting, which regulations matter, and where adoption is happening. It blends real-time market data with on-chain analytics and recent policy developments so any audience—from first-time buyers to professional allocators—can make better decisions. We rely on trusted sources including CoinDesk, Glassnode, CoinShares, Kaiko, CoinGecko/CoinMarketCap, Reuters/FT, the BIS and the IMF (citations throughout).

Why staying updated matters

Crypto cycles turn quickly. In just the past few weeks, total Crypto Market Sentiment 2025: Unveiling Investor Insights value has hovered around the multi-trillion dollar mark, with sharp daily rotations between Bitcoin and Ether as macro expectations flip and ETF flows swing. Missing these shifts can mean buying tops or panic-selling bottoms. Up-to-date context—price/volume, fund flows, liquidity, and policy—helps you separate signal from noise and align risk to your time horizon.

What we’ll cover (key themes)

- Global market trends: capitalization, leaders (BTC/ETH), short-term volatility drivers.

- Tech & innovation: Ethereum’s Dencun (EIP-4844) effect, scaling on L2s, Solana performance, security trends (ZKPs, audits, exploit data).

- Regulation: shifts at the SEC, EU MiCA rollout, UK FCA updates.

- Adoption & sentiment: retail vs. institutional flows, social and on-chain behavior.

2) Global Market Trends

Current market performance & capitalization

The global Crypto Market Sentiment remains near its summer highs (multi-trillion USD). Bitcoin trades around $110k today (chart above), while Ether has seen a strong run and subsequent pullback after setting fresh records over the weekend—liquidity in ETH remains supportive despite profit-taking, according to Kaiko. Short-term price action has been whipsawed by macro headlines (Jackson Hole rate-cut hopes) and rebalancing out of BTC into ETH.

Where we are on time frames:

- 24H: A modest risk-off tone with BTC slightly lower and most majors down.

- 7D: Rotation dynamics—ETH outperformance into weekend highs, then a retrace; BTC steadying near $110k. Liquidity has improved across top names, cushioning moves.

- YTD context: Episodes of new highs (BTC above $120k earlier in August) and a July total market cap push above $4T, coinciding with U.S. legislative momentum on stablecoins and broader frameworks.

Primary data: We cross-reference CoinMarketCap/CoinGecko dashboards for real-time cap/price snapshots.

Institutional involvement & macro influence

Institutional flows continue to set the tone. The CoinShares weekly flow series shows record-sized inflows mid-August (US$3.75B, fourth-largest on record, led by ETH) followed by US$1.43B outflows last week as rate expectations swung—illustrating how macro uncertainty (Fed path) transmits into Crypto Market Sentiment ETPs.

- Bitcoin & Ether ETPs increasingly act as sentiment amplifiers, with trading volumes spiking to ~US$38B last week even as net outflows hit.

- MicroStrategy and other corporates continue to anchor the “treasury BTC” narrative, while Grayscale/iShares flows set marginal price moves day-to-day. (Flows: CoinShares weekly; corporate holdings/ETPs: CoinDesk/issuers.)

Macro lens: The BIS 2025 Annual Economic Report flagged rising policy uncertainty (tariffs, slower global trade), a backdrop that often increases Crypto Market Sentiment correlation with risk assets intraday even as some investors frame BTC as macro-hedge.

Bottom line: Sentiment is constructive but fragile—supportive liquidity and ETF access on one side; rates, growth and policy noise on the other.

3) Technological Developments & Innovations

Blockchain advancements (scaling & consensus)

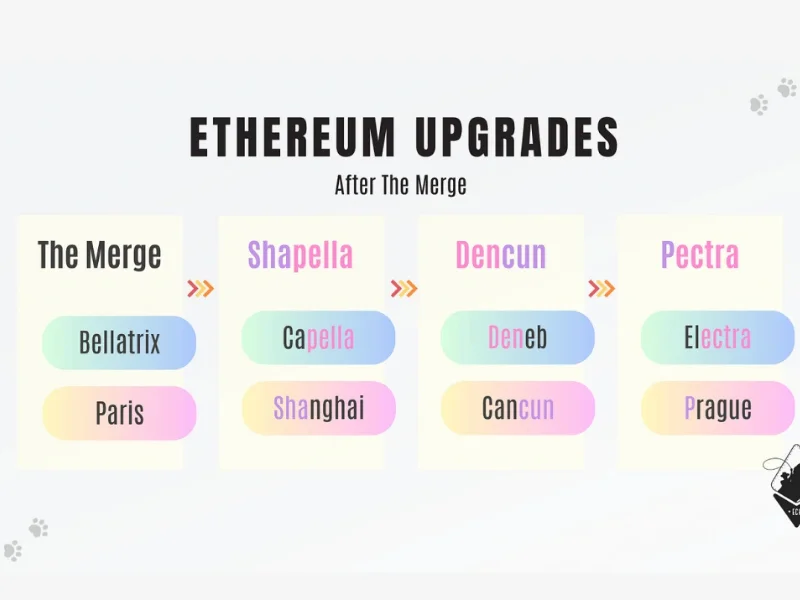

Ethereum’s Dencun (EIP-4844) went live in March 2024 and has kept transforming the stack: “blob” transactions cut L2 data costs, materially improving user fees and throughput on rollups. Glassnode highlights Dencun’s fee-lowering effect and validator set tweaks that can modestly tighten ETH issuance; ecosystem tools (QuickNode) summarize EIP-4844’s design and timelines.

Elsewhere, high-throughput L1s (e.g., Solana) continue optimizing performance while L2 ecosystems on Ethereum expand. DeFi TVL remains in the hundreds of billions with broad-based participation across chains, per DeFiLlama.

On-chain support for progress: Glassnode’s “Week On-Chain / Ethereum” and cross-reports with Coinbase document throughput and cost improvements rippling from Dencun into L2s and dApps.

Security enhancements in Crypto Market Sentiment

Security is improving, but risk persists. In H1 2025, blockchain security firm CertiK tracked ~US$2.47B in losses from hacks/exploits/scams; Q2 saw fewer incidents vs. Q1, a reminder that defensive hardening is working even if absolute losses remain material.

- ZKPs (zero-knowledge proofs) underpin privacy-preserving verification and help scale settlements (ZK-rollups).

- Smart contract rigor: Audits, formal verification, and proxy/upgradeability patterns (now common across dApps) are mainstream; academic work in 2025 tracks how widely these design patterns are used in production.

- Risk dashboards: DeFiLlama’s Hacks tracker makes exploit data transparent, supporting better protocol risk pricing.

Impact of smart contracts & dApps

Smart contracts power DeFi, gaming, RWAs, and payments. Messari protocol reports (e.g., 1inch, Ethereum, Tron) and Dune dashboards show DAU/MAU trends, fees, and volumes. While Q2 2025 dApp activity moderated slightly (24.3M daily UAW, –2.5% QoQ), it’s still well above early-2024 levels (+~247%), with gaming and AI-linked apps leading.

4) Regulatory & Legal Landscape

Current regulatory updates

United States: In a notable 2025 shift, the SEC moved to dismiss its 2023 lawsuits against Coinbase and later Binance, signaling a change in approach under new leadership; the agency has emphasized building clearer rules and has paused several enforcement actions.

European Union: MiCA is now in force, with stablecoin provisions effective since June 30, 2024, and CASP (service-provider) requirements applying from Dec 30, 2024. ESMA has issued detailed 2025 guidelines on knowledge/competence and supervisory implementation.

United Kingdom: The FCA has tightened financial promotions rules and, per recent press, is moving toward retail access to Crypto Market Sentiment ETNs from October 8, 2025, marking a significant policy shift from the 2021 stance.

Legal cases & precedents

The dismissals of the SEC’s Coinbase/Binance suits reduce near-term headline risk, but policy is not a free-for-all: market-abuse, AML/KYC and disclosures remain central under U.S./EU/UK regimes. The Binance criminal settlement (2023) still frames compliance expectations for CEXs.

5) Adoption & Market Sentiment

Retail & institutional adoption

ETF rails have pulled new cohorts into BTC/ETH. CoinShares reports show dramatic swing weeks—from multi-billion inflows led by iShares ETH to US$1.43B outflows as macro jitters surge—illustrating how institutional sentiment can turn on policy headlines.

Retail engagement leans toward low-fee L2s, mobile wallets, and cross-chain swaps; CoinGecko and Messari coverage highlights growing participation in AI-adjacent tokens and RWA-linked assets.

Social media & influencers

Sentiment on X/Twitter, Reddit, and Telegram still drives short-term flows, but data platforms (e.g., Santiment, Nansen) show a maturing pattern: whale transactions and exchange flows tend to front-run social buzz. Educational hubs like CoinBureau continue to onboard beginners and shape narratives.

6) On-Chain & Market Microstructure

Tracking on-chain activity

Bitcoin on-chain: CryptoQuant reported spikes in miner-to-exchange flows during May–June (post-halving difficulty squeeze), followed by declining exchange reserves into August, partially offset by increased ETF custody holdings—a structural shift in where spot BTC sits.

Active addresses & transactions remain robust vs. long-term averages, with recent weeks showing slight softening as prices consolidated. (CryptoQuant dashboards; CoinDesk recap of miner revenue lows in late June.)

Liquidity & market movements

Liquidity quality is a crucial sentiment pillar. Kaiko shows BTC’s 1% market depth at or near record highs in recent months; ETH liquidity has also improved markedly—even after pullbacks—reducing slippage for larger orders. Altcoin order books remain thinner and more stress-sensitive.

DeFi liquidity: TVL sits in the $100B+ range across chains; DEX volumes can surge on macro-or-ETF headlines. DeFiLlama provides protocol-level breakdowns (fees, revenues, chain splits) to monitor when risk appetite broadens beyond BTC/ETH.

7) Emerging Trends & Future Outlook

NFT growth & impact

NFTs are evolving from art/collectibles toward gaming, IP licensing, and ticketing. Industry trackers (CryptoSlam/DappRadar) show activity stabilizing after 2024’s reset, with gaming still the largest vertical by unique wallets. Policy groups (e.g., Coin Center) continue to brief lawmakers on digital ownership and speech implications around NFTs.

DeFi’s next leg

Perps DEXs, restaking, RWAs, and cross-chain liquidity are core narratives. DeFiLlama highlights where capital is actually parked and which fee-generating protocols sustain themselves without heavy incentives. Expect L2-native applications to keep gaining as EIP-4844 economics flow through.

Stablecoins & CBDCs

Stablecoins continue growing as crypto’s everyday “money,” while central banks push on with CBDC research and pilots. The BIS (Aug 2025) notes most jurisdictions now have or are developing stablecoin frameworks, and 9 in 10 central banks are exploring CBDCs. The IMF’s 2025 notes dig into offline CBDC design and private-law issues—evidence that policy plumbing is catching up to technology.

8) Investor Insights & Sentiment Analysis

Behavior patterns

Investors are barbelling risk: core allocations to BTC/ETH via ETFs and L2-friendly, fee-efficient wallets—paired with selective bets on AI, gaming, or RWA narratives. On-chain, miner stress spikes (post-halving) have not triggered systemic capitulation; old-supply (Satoshi-era) selling has been muted in 2025 compared with 2024, suggesting longer-term conviction.

Risk management in Crypto Market Sentiment

Messari reports and pro desks emphasize position sizing, liquidity screens (market depth), venue quality, and hedging (options/futures) as standard. Kaiko’s liquidity work shows why slippage and order book health belong in any risk checklist, especially outside BTC/ETH.

9) Case Studies & Market Examples

Bitcoin halving events & price impact

Historically, BTC’s post-halving phases see strong performance with lags; 2024’s halving cut issuance to 3.125 BTC per block. CoinDesk analysis and index research suggest gains often materialize months after the event, and reactions can be uneven across miners as difficulty and revenue adjust. 2025 has already featured new highs and cooling stretches—classic for prior cycles.

Ethereum’s path post-Dencun (toward Pectra)

Dencun delivered lower L2 costs and better scalability economics; Pectra planning continues into 2025+ with further UX and account-model upgrades on the roadmap. On-chain data indicate lower rollup fees, higher activity on Base/OP/Arbitrum, and a better environment for consumer-grade dApps.

10) Impact of Global Events on Crypto

Economic factors

Inflation progress, growth scares, and rate path ambiguity continue to toggle crypto risk appetite. Last week’s ETP outflows (US$1.43B) coincided with shifting Fed expectations—clear evidence that macro steers sentiment in the short run, even when long-term Crypto Market Sentiment theses remain intact.

Geopolitics

The BIS 2025 overview flags increased trade fragmentation and tariff uncertainty. Such backdrops can raise cross-asset volatility, at times supporting the “digital gold” framing of BTC yet also raising correlation with risk assets intraday. Monitor fund flows and liquidity depth for the cleanest read on how geopolitics is filtering into Crypto Market Sentiment.

11) Key Insights from Industry Experts

- CoinShares (James Butterfill) highlights historic inflow weeks and the fragility when macro turns—useful for timing and sizing.

- Kaiko Research emphasizes record BTC depth and ETH liquidity resilience, explaining why top-tier assets absorb shocks better than many alts.

- CoinDesk analysts connect the dots between halving mechanics, ETF flows, and miner economics—insightful for medium-term cycle views.

Takeaway: The expert consensus for late-2025 is constructive but conditional—supportive flows/liquidity vs. policy/macro headwinds. Position accordingly.

12) Conclusion

Recap

- Market: Multi-trillion cap, BTC near $110k; ETH strong but volatile; liquidity robust for majors.

- Tech: Dencun/EIP-4844 lowered L2 costs and broadened use cases; smart contracts keep expanding DeFi/gaming/RWAs.

- Policy: U.S. enforcement tone has softened; EU MiCA and UK FCA actions shape clearer paths for compliant products.

- Sentiment: ETF flows and liquidity are the heartbeat; on-chain shows no systemic miner stress; social buzz follows whale/exchange moves, not the other way around.

Stay informed (call to action)

Keep a regular cadence: CoinDesk (news/markets), CoinShares (weekly flows), Glassnode/CryptoQuant (on-chain), Kaiko (liquidity), DeFiLlama (TVL, hacks), CoinGecko/CoinMarketCap (prices) and Reuters/FT (policy/legal). These together give you the best near-real-time map of Crypto Market Sentiment.

13) FAQs

1) What’s the single best real-time gauge of crypto market sentiment?

Answer: ETF/ETN flows and order-book depth. Weekly CoinShares flow reports and Kaiko’s liquidity metrics tell you if institutions are adding risk and whether markets can absorb it without slippage.

2) Why did ETH rally so hard and then pull back?

Answer: Post-Jackson Hole, spot demand lifted ETH to new highs, but profit-taking followed. Even so, Kaiko notes liquidity remains supportive—more depth, tighter spreads—so pullbacks haven’t unraveled structure.

3) Are miners capitulating post-halving?

Answer: We saw episodic selling pressure (spikes in miner-to-exchange flows), but no systemic capitulation. Miner revenues dipped in late June, then stabilized; “Satoshi-era” miner selling is minimal in 2025.

4) How did Dencun (EIP-4844) change Ethereum?

Answer: It introduced blob data that dramatically lowered L2 data costs, improving throughput and reducing user fees—fuel for dApp adoption.

5) Is hacking getting better or worse?

Answer: H1 2025 losses were ~US$2.47B (CertiK), but Q2 incidents fell vs. Q1. Security is improving, but vigilance is essential; use protocol risk dashboards like DeFiLlama Hacks.

6) What regulations matter most now?

Answer: In the U.S., the SEC has dismissed major lawsuits (Coinbase/Binance) while signaling a rule-making pivot. In the EU, MiCA is fully in force; in the UK, FCA policy on promotions and retail ETNs (from Oct 8, 2025) is pivotal.

7) How do I judge whether an altcoin is “liquid enough”?

Answer: Check 1% market depth and spreads (Kaiko). Many alts suffer deeper liquidity drawdowns than BTC during stress—plan position size accordingly.

8) Are NFTs dead?

Answer: No—mix is shifting. Volumes rotate toward gaming, tickets, and IP use cases. Track dUAW (daily unique active wallets) for traction; Q2 2025 was down slightly QoQ but dramatically higher vs. early-2024.

9) What’s the importance of stablecoins and CBDCs to sentiment?

Answer: Stablecoins reduce friction and feed liquidity; CBDCs signal official sector engagement. BIS/IMF 2025 publications show most jurisdictions building frameworks—this underpins long-run adoption confidence.

10) I’m new—what’s a simple monitoring routine?

Answer:

- Prices/market cap: CoinGecko/CMC.

- Weekly flows: CoinShares (Mondays).

- Liquidity depth: Kaiko insights.

- On-chain health: Glassnode/CryptoQuant.

- TVL & security: DeFiLlama.

- Policy/legal: Reuters/FT.