1. Introduction

The crypto market is constantly evolving, and staying abreast of the latest developments is crucial for investors and enthusiasts alike. This article aims to provide a comprehensive update on current crypto trends in 2025, covering market movements, technology, regulation, and adoption. We draw on authoritative sources – from industry news outlets (CoinDesk, Bloomberg Crypto) to on-chain analytics (Glassnode) and market reports (CoinShares, CoinGecko) – to give readers a data-driven view of the landscape. Key themes include how macroeconomic factors and institutional flows shape Crypto Market Cycles, the latest blockchain innovations, regulatory shifts worldwide, and the adoption of crypto by retail and institutional players.

2. Global Market Trends

Current Market Performance & Capitalization

As of mid-2025, the total global cryptocurrency market cap hovers around $3.88 trillion[1]. Bitcoin remains dominant, commanding about 56.3% of the market with a market cap around $2.19T[1], while Ethereum’s market cap is roughly $543B (ETH trading near $4,500)[2]. Other large-cap coins include XRP and BNB (each in the low hundreds of billions)[3][4]. Over the last 24 hours and week, prices have been mixed: for example, Bitcoin is up ~0.9% (24h) and ~4.6% (7d)[5], reflecting modest gains amid volatility.

These swings often reflect short-term news – for instance, U.S. inflation reports and Fed policy talks are currently the biggest drivers. Analysts note that if inflation data come in hotter than expected, traders may take profits (e.g. by buying protective puts around $115–118K on BTC)[6][7]. In fact, a recent Coindesk analysis warns that a surprise CPI print could stall the Bitcoin rally by triggering profit-taking across all risk assets[6].

Figure: The crypto market remains led by Bitcoin (~56.3% dominance) with a total cap around $3.88T[1].

Institutional Involvement & Economic Influence

Institutions continue to influence crypto cycles. CoinShares reports that professional investors held ~$21.2B in U.S. Bitcoin ETF positions in Q1 2025[8]. This is down ~23% from Q4 2024, largely due to an 11% pullback in prices[8]. Institutional share of total ETF assets under management (AUM) also slipped (22.9% vs 26.3% prior quarter)[9], indicating hedge funds have trimmed exposure even as investment advisers have added more.

Corporate “treasury” holders (the MicroStrategy model) continued to accumulate: total corporate Bitcoin supply rose from 1.68M to 1.98M BTC by mid-May 2025 (an 18.7% increase YTD)[10]. In particular, MicroStrategy (now Strategy) leads with ~632,457 BTC (~$69.4B) on its books[11][12]. Other public holders are much smaller: for example, Marathon Digital holds ~50.6K BTC, Coinbase ~11.8K BTC, Tesla ~11.5K BTC[13][14].

Sentiment is very sensitive to macro-economic news. For instance, crypto investment funds saw a $1.43B outflow in late August 2025 – the worst since March – as hawkish Fed commentary sparked a risk-off mood[15]. However, a more dovish Fed pivot later in the week recaptured ~$594M in inflows[16]. Similarly, mid-2025 CoinShares flow data show weekly inflows slowing to $224M as investors awaited Fed clarity[17]. Ethereum products led with a $296.4M inflow (its strongest since late 2024), while Bitcoin products had ~$56.5M in outflows amid uncertainty[17][18]. These trends illustrate how global economic factors (inflation, monetary policy, geopolitical risk) are now just as important for crypto bull/bear shifts as crypto-specific news.

3. Technological Developments and Innovations

Blockchain Advancements

Ethereum upgrades: 2025 is seeing major Ethereum protocol changes. After the Shanghai/Dencun upgrades (May 2024), Ethereum briefly moved back into net inflation: issuance of new ETH (from staking rewards) now slightly exceeds the burn from transaction fees[19]. This has reignited debates on ETH value accrual. However, network fundamentals remain strong – active validators and total staked ETH are stable[20]. The ecosystem is increasingly rollup-centric; long-promised sharding gave way to “Danksharding,” a data-model that will bundle rollup transaction data. According to Ethereum.org, this shift means rollups (Layer-2 protocols) will become even cheaper and more efficient[21].

Figure: Glassnode/CME report on Ethereum H1 2025 highlights that ETH’s price underperformance coexists with strong network usage (staked ETH, validator count)[20].

Scaling & new consensus: Other Layer-1 blockchains are also innovating. Solana has established itself as a high-throughput chain: using its Proof-of-History consensus and parallelized architecture, Solana theoretically supports up to 65,000 transactions per second (TPS), though real-world usage is around 3,700 TPS[22]. Ongoing upgrades like Firedancer and Alpenglow aim to enhance Solana’s stability, decentralization, and sub-second finality[23]. Similarly, networks like Avalanche, Polkadot, and Cardano continue to improve their throughput and cross-chain interoperability. In Ethereum’s case, ongoing updates (e.g. EIP-4844/KZG to further cut Layer-2 fees) are in development, keeping its scaling roadmap on track.

Security Enhancements in Crypto

As crypto adoption grows, so do security innovations. Zero-knowledge proofs (ZKPs) are now widely used to enhance privacy and security on-chain. Protocols like Zcash (zk-SNARKs) and emerging zk-rollups (Starknet, zkSync) enable verification of transactions without revealing raw data, protecting user privacy. Research shows ZK techniques are being extended to supply chains and identity systems[24]. Meanwhile, smart contract security has improved: new tools for formal verification and AI-driven auditing (e.g. Hacken’s Defender, MythX, Certora) help catch bugs before deployment.

However, threats have also become more sophisticated. Recent hack summaries underscore the risks of key management: in 2025 a decentralized finance firm (UPCX) lost $70M via a stolen admin private key and malicious upgrade[25], and the WEMIX NFT platform lost $6.1M to compromised auth keys[26]. Such incidents highlight that even audited protocols can be undermined by off-chain failures. Industry experts stress the need for multi-layered security (multi-sig wallets, hardware keys, continuous monitoring) and decentralized “bug bounty” platforms. Notably, a Chainalysis report also flags rising “wrench attacks” (physical coercion of holders) as Bitcoin’s price climbs, emphasizing that crypto security increasingly extends beyond code to personal safety[27].

Impact of Smart Contracts and dApps

Smart contracts and decentralized applications (dApps) continue to reshape finance and other industries. The DeFi ecosystem now has ~123.6B total value locked (TVL)[28], and over 14 million unique wallets have interacted with DeFi protocols in 2025[28]. Leading DeFi chains (Ethereum, BNB, Arbitrum, etc.) host tens of billions in lending, trading, and yield markets. A CoinLaw analysis shows Ethereum holds ~$78.1B of DeFi’s TVL (63%), while Layer-2s like Arbitrum ($10.4B) and Base ($2.2B) are rapidly growing[29]. Platforms like Uniswap (DEX), Aave (lending) and Lido (staking derivatives) remain the largest protocols by market value[30].

dApps are also booming in gaming, NFTs, and social. According to industry surveys, blockchain gaming now accounts for ~24% of dApp user activity and ~25% of NFT trading volume[31][32]. Popular gaming metaverses and NFT marketplaces continue to onboard users by rewarding play-to-earn or offering collectible assets. Overall, decentralized social and content platforms are maturing too, reflecting a trend toward Web3 consumer apps. The Messari team notes that new narratives (like social tokens, GameFi, AI x crypto) are emerging, suggesting the next growth sectors may blend gaming, NFTs, and AI-driven content.

4. Regulatory and Legal Landscape

Current Regulatory Updates

Globally, regulators are moving fast. In the U.S., the SEC and CFTC have been active. Notably, in early 2025 the SEC issued a landmark guidance stating that certain proof-of-stake (PoS) cryptocurrency staking activities are not securities, clarifying compliance for many projects[33]. Congress is also considering stablecoin legislation: the GENIUS Act (passed by one chamber in mid-2025) would create a federal charter for algorithmic stablecoins. Meanwhile, SEC leadership has signaled a willingness to establish “innovation exemptions” to enable DeFi pilots under oversight[34]. The Department of Labor even reversed prior warnings to allow crypto holdings in retirement accounts, reflecting growing acceptance.

In Europe, the MiCA framework has arrived: as of Jan 2025, any crypto-asset service provider must register under MiCA to operate across the EU. This includes rules for stablecoins (stringent reserve backing and transparency). CoinBureau analysts warn that MiCA initially caused FUD (e.g. fears that non-authorized stablecoins like Tether would be delisted)[35]. In practice, Tether has preemptively acquired a MiCA-compliant issuer, and Circle’s USDC is already MiCA-authorized[36], meaning major trading pairs can shift to compliant coins.

The UK’s FCA is likewise formulating rules: it launched a public consultation (CP25/14) in mid-2025 to govern stablecoin issuance and digital asset custody, aiming for implementation by 2026[37][38]. (For instance, the FCA proposal requires stablecoins to back 1:1 with assets and allows holders quick redemption[37][38].)

Other jurisdictions vary: Switzerland, Japan and Singapore continue to license crypto exchanges and token issuers. In the U.S., the CFTC is also asserting jurisdiction: it successfully litigated against Ponzi schemes (e.g. My Big Coin Pay) as unregistered commodity derivatives, and ongoing cases emphasize commodities oversight. Overall, regulators are converging on tighter controls: anti-money-laundering checks, token classification guidance, and investor protections.

Legal Cases & Precedents

High-profile court cases have sent shocks through crypto markets. In early 2025, the SEC abruptly dropped enforcement cases against both Binance and Coinbase[39][40]. For Binance, this followed an 18-month probe (the dismissal came May 2025)[39]. For Coinbase, the SEC filed a joint stipulation in Feb 2025 agreeing to dismiss a 2023 enforcement action[40]. In both cases regulators stated the moves were strategic (to focus on rulemaking via their new Crypto Task Force) rather than meriting acquittal[39][40]. Nevertheless, these decisions underscore legal uncertainty: they effectively reset the playing field and keep much crypto regulation in limbo.

Meanwhile, criminal prosecutions have ramped up. Sam Bankman-Fried (FTX CEO) was convicted and sentenced in late 2023 for fraud and conspiracy related to the FTX collapse (25 years in prison in Mar 2024). His case (and others like Voyager’s Sam Bankman-Quinn plea in Aug 2023) reinforce that traditional fraud charges (wire fraud, money laundering) are the current enforcement path for crypto misconduct. This patchwork of lawsuits and rulings continues to shape investor sentiment: each development can trigger rallies or sell-offs as market participants reassess legal risks.

5. Adoption and Market Sentiment

Retail and Institutional Adoption

Crypto adoption keeps climbing, especially at the retail level. Recent industry data estimate that roughly 6.8% of the global adult population (over 560 million people) owned cryptocurrencies by 2024[41]. Demand is particularly strong in fast-growing markets: for example, Southeast Asia, Latin America, and Africa have seen rapid wallet growth due to inflation hedging and remittance use. Chainalysis’s 2024 adoption index even finds Central and Southern Asia/Oceania leading globally in crypto usage[42]. At the same time, major brands and financial firms are onboarding crypto. PayPal, Visa, and Mastercard have rolled out crypto services; institutional firms like BlackRock and Fidelity now offer crypto ETFs; and companies like Tesla, Square, and MicroStrategy hold crypto on their balance sheets.

Technology adoption is also advancing: more retail users hold non-custodial wallets and try DeFi platforms or NFT marketplaces. Data from DappRadar indicates that DeFi still commands the largest share of active blockchain users (~27%), but gaming dApps (24%) and NFT-related apps (15%) are significant[31]. Even if total user numbers are still far below mainstream apps, growth rates remain high. For example, DeFi TVL and dApp users have increased by 30–40% year-over-year[29][31]. Survey and on-chain analytics show that a new generation of retail investors is entering via mobile-first crypto apps and peer-to-peer networks.

Impact of Social Media and Influencers

Crypto markets are notoriously sentiment-driven, and social media amplifies this. Platforms like Twitter/X, Reddit, and TikTok – and personalities from Elon Musk to crypto Youtubers – can cause rapid price swings. Coin and token launches (or crashes) often trace back to social hype or FUD. Analytics firms (e.g. Santiment, Messari) now track on-chain social metrics: they correlate spikes in Google Trends or Twitter mentions with short-term price peaks. For instance, huge inflows to Dogecoin and memecoins in 2021 were largely driven by Elon Musk’s tweets and Reddit forums. In 2025, new meme projects and “social tokens” continue to emerge, making the market more sensitive to influencer sentiment.

Regulators have taken note: SEC and lawmakers have held hearings about crypto influencers, warning they may face liability for pumping unregistered tokens without disclosure. Nevertheless, for savvy investors, social media can be a double-edged sword – it can reveal emerging trends early (like NFT drops or DeFi protocols going viral) but also trigger irrational manias. Professional investors now often distinguish “noise” from true on-chain demand, using analytics (e.g. wallet inflow data, Slack group chats) to cut through hype. In summary, while social media no longer reliably indicates market fundamentals, it still strongly shapes retail market sentiment and short-term volatility.

6. On-Chain and Blockchain Activity

Tracking On-Chain Activity

On-chain metrics provide a real-time window into market health beyond price charts. Key indicators include transaction volume, active addresses, miner/validator activity, and fees. For example, Glassnode data show that Bitcoin’s active addresses recently fell ~2% to about 692,000, dipping below the low band[43]. Transaction fees also dropped ~17%, indicating less demand for blockspace. These trends (along with a stagnating “Realized Cap” growth) suggest waning demand and profitability[43]. Traders follow these signals closely; low active addresses and falling Net Unrealized Profit/Loss (NUPL) – currently around 5% for BTC – can foreshadow consolidation or pullbacks[43].

Ethereum’s on-chain stats similarly guide sentiment. Recent Glassnode reports show that ETH staking participation (validator count and total staked) has remained robust despite price weakness[20]. Additionally, the growth of layer-2 networks can be tracked via bridges: for instance, Arbitrum’s and Optimism’s transaction counts and bridge inflows are used by analysts to gauge L2 adoption. Overall, active address counts, transaction throughput, and gas fees across major chains are key components of “blockchain activity” indices that signals investor engagement and network usage.

Liquidity and Market Movements

Liquidity in crypto markets is uneven. Bitcoin and Ethereum have deep liquidity pools on major exchanges, which helps dampen volatility for those assets. In contrast, many altcoins trade in far thinner markets. Data from providers like Kaiko rank assets by true liquidity – measuring order book depth and spread[44]. Their frameworks consistently show BTC and ETH at the top, followed by a handful of major alts.

This means that selling large positions in smaller tokens can cause outsized price moves. On the DeFi side, DeFiLlama data reveal total value locked (TVL) across protocols (~$93B in mid-2025). High TVL tends to indicate strong liquidity within lending/DEX pools. For example, DEXs like Uniswap and lending pools like Aave each hold tens of billions.

Short-term market movements are also affected by liquidity dynamics. Low liquidity periods – often seen in summer or year-end – can exaggerate volatility. Conversely, institutional flows can stabilize liquidity: large inflows into crypto funds (e.g. by big investment firms) provide a buffer. Analyst Nansen reports increased activity by whale addresses in 2025, and highlights that these whales often move funds only when liquidity is sufficient to avoid big slippage. In practice, traders watch exchange order books and TVL on major DeFi protocols as proxies for liquidity, to time entries and exits. The recent uptick in decentralized exchange volumes (now regularly exceeding $20B daily[45]) also demonstrates that on-chain liquidity has grown, even if much of trading still occurs on centralized venues.

7. Emerging Trends and Future Outlook

NFT Growth and Impact

The NFT (Non-Fungible Token) sector continues to expand beyond digital art. Global NFT market estimates for 2025 range widely, but one analysis projects $49–61 billion in market size by year-end[46]. Gaming is now the dominant NFT use case: $12.9B in gaming-related NFT revenue was recorded in 2025 (about 25% of total NFT volume)[32]. Sports collectibles (NFL, NBA, FIFA cards) added ~$2.7B, while art/community NFTs still generated ~$4.1B[32]. Blockchains facilitating NFTs also diversify: Ethereum still hosts ~62% of NFT contracts and volume, but Solana (~18%) and Polygon (~11%) are major players[47]. Innovations like “phygital NFTs” (linked to real goods) and fractionalized ownership of NFTs are emerging trends.

Regulators and institutions are cautiously watching NFTs: while some jurisdictions warn of scam NFTs, others see potential. Centralized entities (e.g. eBay, Visa, sports leagues) have announced NFT initiatives, blurring lines with mainstream media. The future outlook is mixed: on one hand, overall interest (measured in unique wallets engaging with NFT marketplaces) has leveled off from the mania of 2021–2022; on the other, NFTs are finding real utility in gaming and digital identity. Policy think tanks (Coin Center, for instance) argue that NFTs can play a long-term role in verifying digital ownership, and any short-term speculator hype is likely to settle as the market matures.

DeFi’s Continued Evolution

Decentralized Finance is steadily penetrating traditional finance. Total DeFi TVL is rebounding (~$123.6B as of mid-2025[28]) and continuing on a multi-year growth trajectory. New applications – such as decentralized insurance, on-chain credit scoring, and automated portfolio management – are gaining traction. Real-world asset tokenization (e.g. bonds, real estate) is an emerging category: industry reports show DeFi tokenization projects up significantly in 2025. Leading protocols are also evolving their product lines: for example, Uniswap has launched version 4 (with more flexible pools), and Aave introduced credit delegation on a larger scale.

From a platform view, the dominance is shifting. While Ethereum still holds ~63% of DeFi activity[29], Layer-2 solutions are chipping in. Notably, Avalanche, Tron, and newcomers like Aptos/Sui are building substantial DeFi ecosystems. Multi-chain liquidity is growing too: users increasingly move assets across chains via cross-chain bridges. DeFiLlama ranks Arbitrum and BNB Chain among the highest TVLs, reflecting how liquidity and use are spreading.

Stablecoins and CBDCs

Stablecoins remain a bedrock of crypto liquidity. Major USD-pegged coins (USDT, USDC, BUSD) collectively have $277B market cap[45], accounting for over half of all crypto trading volume. Their dominance means that any stress or regulatory change in stablecoins quickly ripples through markets. For instance, debates over reserve audits and legal compliance (e.g. in the UK or EU) drive investor caution.

Parallel to crypto stablecoins, central banks worldwide are progressing with central bank digital currencies (CBDCs). According to a BIS 2024 survey, 91% of central banks are exploring retail and/or wholesale CBDCs[48]. More than one-third of surveyed banks have accelerated their CBDC projects specifically due to the rise of stablecoins and cryptoassets[49]. Major economies are in trials: China’s digital yuan expansion, India’s upcoming retail CBDC launch (with offline functionality), and a digital euro pilot (part of the 2020–25 EU digital finance strategy) are all examples.

The IMF and World Bank have also published frameworks on CBDCs to guide emerging-market adoption. While CBDCs themselves won’t directly move Crypto Market Cycles, their emergence signifies a broader trend: tokenization of value is driving both private and public innovation in digital money. Observers note that CBDCs could eventually reduce demand for unbacked crypto (for payments), but initially they may lend legitimacy to blockchain technology and keep more public assets (like currency) on-chain.

8. Investor Insights and Sentiment Analysis

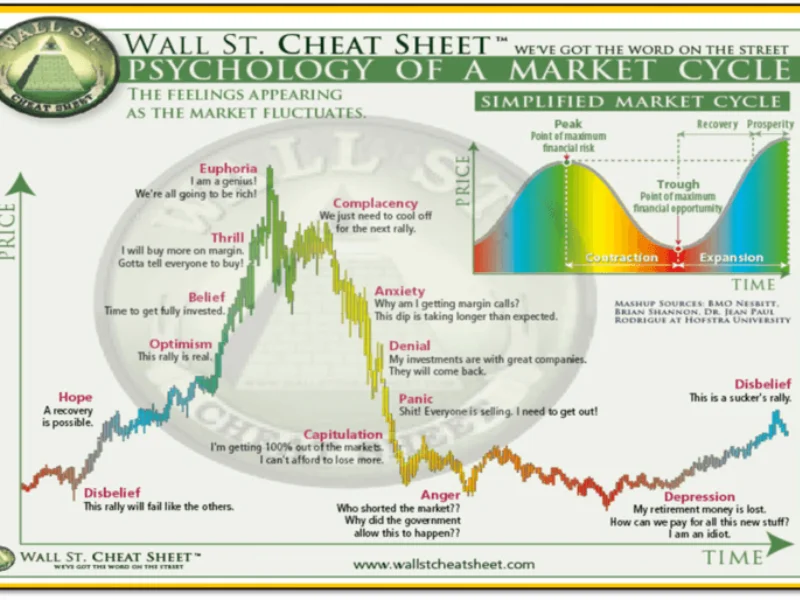

Investor Behavior Patterns

Behavioral patterns in crypto cycles resemble traditional markets but with higher tilt toward fear/greed swings. Surveys in 2025 show many retail investors still buy on hype (FOMO) and sell on FUD news, while seasoned investors use macro signals (rate outlook, currency trends) to time trades. Chain on-chain data providers (Nansen, Santiment) track the “whale” activity of large holders. Lately, they note that many whales have been accumulating quietly on dips – for example, on-chain analysis found that the top 10% of addresses continued adding BTC in Q2–Q3 2025, indicating accumulation phase. Sentiment indices (like the Crypto Fear & Greed Index) reflect this: it hovered in the “fear” zone during sharp pullbacks but recovered to neutral/greed as prices rebounded post-Fed pivot.

Regulatory clampdowns or industry scandals (like past exchange hacks) have historically pushed retail to panic-sell. However, 2025 data suggest a growing maturity: more crypto holders now “hodl” through volatility. Fund flow reports show fewer flight-to-stablecoins spikes after corrections. This shift is partly due to the increasing presence of institutional investors, whose allocation strategies smooth out emotional retail moves.

Risk Management in Crypto Investments

Investors are applying more risk management disciplines. Diversification across multiple crypto assets and strategies (spot, futures, options) has become common for larger portfolios. Stablecoins are used as short-term hedges – for instance, parking gains in USDC during market drops. Derivatives markets (options, perpetual futures) are actively used for hedging: open interest in BTC and ETH options has grown with products on exchanges like Deribit and CME.

Messari analysts emphasize that crypto has no bailouts, so individual investors must hedge tail risks themselves[50]. The Crypto Market Cycles ecosystem now offers insurance products (Nexus Mutual, InsurAce), and larger holders increasingly use institutional custodian services that include security audits and asset insurance.

Finally, margin and leverage use has become more controlled post-2022. Many exchanges raised margin requirements, and investor education campaigns by platforms have stressed “don’t over-leverage.” As one expert puts it, without a lender of last resort, proper insurance and hedging are “critical” in crypto[50]. Portfolios often cap crypto exposure relative to total assets or use systematic DCA (dollar-cost averaging) to spread risk over time.

9. Case Studies and Market Examples

Bitcoin Halving Events and Price Impact

Historically, each Bitcoin halving (the 4-year event that cuts mining rewards in half) has preceded major bull markets, as reduced issuance eventually tightens supply. Past halvings (2012, 2016, 2020) were followed by sharp price rises 6–12 months later. However, market experts now debate whether this effect is fully priced in. A K33 analyst notes that macro factors (interest rates, fiscal policy) may “matter more now for BTC than the quadrennial halvings”[51]. In other words, Bitcoin’s mature market status and new ETF flows could dilute the halving’s impact. Indeed, Consensus magazine commented that active inflows from spot BTC ETFs have already pushed prices to records, potentially muting the classic post-halving surge[52].

Nonetheless, many investors still see the 2024 halving (occurred in April 2024) as a bullish foundation. Analysts expect that if macro conditions remain supportive (e.g. loose money, geopolitical uncertainty), Bitcoin could still rally into 2025–2026, albeit perhaps with lower volatility than in earlier cycles. The takeaway is that while halvings are positive supply shocks, their impact now plays out alongside larger economic trends[51][52].

Ethereum 2.0 Transition

Ethereum’s long-planned “2.0” (the switch to proof-of-stake) was largely completed with The Merge in 2022. Since then, its evolution has been more iterative. One way to gauge progress is by on-chain metrics: Glassnode data show that after the Shanghai/Dencun upgrades (2024), Ethereum shifted from net deflation back to slight inflation[19]. This is because validators can again withdraw stake rewards. However, staking participation remains high – the number of active validators continues rising and ~20% of all ETH supply is staked[20]. This indicates confidence in the network’s security and yield. Performance-wise, Ethereum has been dealing with congestion fees; Layer-2 scaling has absorbed much of the traffic, keeping base layer usage moderate.

A key aspect of Ethereum’s “2.0” story is the thriving DeFi ecosystem built on it. For example, Lido Finance (liquid staking) alone now manages ~$34.8B TVL[53]. Also, upgrades like EIP-4844 (proto-danksharding, scheduled for 2025) aim to further slash Layer-2 gas costs. In summary, Ethereum’s stake-and-scale transition appears successful: it secured the chain and catalyzed innovation, even if it has temporarily reversed some of the earlier deflation. The expectation is that lower fees and faster throughput from L2s will drive broader adoption of Ethereum’s decentralized finance and NFT applications.

10. Impact of Global Events on Crypto Market Cycles

Economic Factors Driving Crypto Adoption

Economic turbulence often drives crypto interest. In regions suffering high inflation or currency devaluation, cryptocurrencies (especially Bitcoin) have seen increased use as a value store. For instance, CoinShares data have shown that flows into Bitcoin funds often spike when inflation fears rise or when stock markets stumble. A Kaiko report notes that uncertainty over trade policy in early 2025 led to risk-off sentiment that dragged crypto prices down after a January rally[54]. Conversely, expectations of accommodative central bank policy or geopolitical stability tend to boost risk appetite (lifting crypto).

Some investors explicitly compare Bitcoin to “digital gold”: they view it as a hedge against fiat debasement. Academic analysis and BIS surveys note this narrative: as traditional safe-havens like cash become less reliable, crypto is sometimes used as an alternative store of value. The BIS survey found that many central banks are pursuing CBDCs partly to preserve the role of official money in an increasingly tokenized world[49], indirectly acknowledging the impact of crypto trends on monetary policy.

One concrete example: during bouts of high U.S. inflation in 2024–2025, crypto markets swung as traders speculated on Fed action. Coindesk’s commentary on the 2025 CPI report highlighted that even small inflation surprises could either turbocharge or crush the market’s short-term outlook[6].

Geopolitical Events and Crypto

Global events – from wars to trade wars to sanctions – have been shown to affect crypto markets. For example, when Middle East conflicts flare or Russian/Ukraine sanctions intensify, crypto often rallies briefly as investors look for alternatives. In 2022–2023, countries under sanctions (e.g. Iran, Venezuela) saw increased peer-to-peer crypto trading volumes. Major powers also use crypto policy as a lever: China’s ban on crypto mining and trading (2017–2021) temporarily pushed hashrate overseas and shifted global mining dynamics. In 2025, focus has been on Russia’s war economy and how crypto funds could be used for avoidance or aid.

Bloomberg Crypto analysts note that crypto tends to become positively correlated with risk assets (stocks, tech) during global growth, but decouple and act more like alternative assets during crises. Recent data suggest that during U.S.–China tensions or regional wars, Bitcoin has sometimes spiked as investors fear broader market chaos. Reuters reported in mid-2025 that gold and crypto were behaving similarly under inflation fears, though crypto’s volatility was higher. Overall, traders watch geopolitical headlines closely: any sign of escalation (e.g. trade sanctions, diplomatic breakdowns) can push crypto prices up as a hedge, whereas de-escalation or treaties can cool the rally.

11. Key Insights from Industry Experts

Expert Opinions on Crypto’s Future

Leading analysts and crypto thought-leaders generally express cautious optimism for 2025–26. Many foresee that blockchain interoperability, identity protocols, and institutional adoption will accelerate. For example, CoinBureau has highlighted that regulated spot ETFs (for BTC and ETH) have fundamentally changed market dynamics by bringing in large-scale capital and legitimizing crypto to traditional investors. As their newsletter notes, net inflows into ETH ETFs have been strong even when BTC ETFs paused, hinting at a maturing market rotation[55].

Bloomberg’s crypto section (through expert columns) predicts that technologies like Layer-2 scaling, ZK-proofs, stablecoin innovations, and decentralized AI will be key growth areas. Industry veteran analysts also suggest that crypto’s volatility will remain high, but adoption will follow an “S-curve,” implying a surge once regulatory clarity and user-friendly infrastructure reach critical mass.

Notably, experts emphasize structural changes: for example, the emergence of decentralized governance (DAOs) and tokenized real-world assets are cited as transformative. Predictions include growing tokenization of stocks and bonds, making crypto rails more integrated with traditional finance. Overall, the consensus is that while a short-term bear or stagnation could occur, the long-term trajectory remains upward as technology and adoption trends build.

Emerging Trends and Predictions

Going forward, analysts highlight several trends to watch:

- Cross-Chain Liquidity: As more blockchains connect via bridges, true multi-chain DeFi is expected to grow. This may reduce the dominance of any single platform and spread market cycles across networks.

- Regulatory Balance: Many experts predict the U.S. will eventually establish clearer rules (potentially after midterm elections or policy reviews), which could trigger a major bull run once regulatory uncertainty abates.

- NFT and Web3 2.0: Beyond collectibles, NFTs are forecast to integrate into gaming (metaverses) and virtual commerce. Some predict “Internet 3.0” social platforms where users own their data/tokens.

- Stablecoin-Driven Innovation: The development of algorithmic and collateralized stablecoins (e.g. approved by the Fed) could bring new payment use-cases. Conversely, stablecoin crises (if any) could trigger large market corrections – something analysts warn about.

- Green Crypto: Environmental concerns are spurring carbon-neutral mining and proof-of-stake adoption; experts see “clean Crypto Market Cycles” becoming a factor for institutional capital (akin to ESG in equities).

- CBDC Integration: Long term, central bank digital currencies may allow citizens to hold wallets directly with the government, increasing public familiarity with digital money (which could indirectly boost crypto interest).

Industry forecasts generally align on one point: the technology is advancing faster than public understanding or regulation. As one Crypto Market Cycles venture capitalist put it, “the next cycle will be driven not by tokens we know today, but by underlying infrastructure improvements (Layer 2s, bridges, standards).” It’s therefore important for investors to keep an eye on underlying metrics (network growth, developer activity) in addition to price charts.

12. Conclusion

In 2025, the crypto markets remain a complex interplay of technological innovation, macro-economic trends, and regulatory shifts. We have seen the total market value hover around $4 trillion, with Bitcoin and Ethereum still leading. Institutional players and corporate treasuries are active, even as retail adoption spreads globally. On-chain data (from Glassnode, CryptoQuant, etc.) suggests somewhat softer demand indicators recently, but the emergence of new use-cases (DeFi expansion, NFTs, tokenization) continues to draw interest. Key trends like Layer-2 scaling, zero-knowledge cryptography, and CBDC development will shape the coming cycles.

Throughout, reliable information is vital. Staying informed via trusted sources (CoinDesk, Bloomberg Crypto, CoinShares, Glassnode, etc.) helps separate signal from noise. As always, Crypto Market Cycles investors should remain vigilant: adopt proper risk management (hedging, diversification, due diligence) and continuously learn about the evolving landscape. By doing so, they can better ride the bull runs and weather the bear markets that inevitably come.

13. FAQs

- Q: How do I know if the crypto market is in a bull or bear cycle?

A: Crypto cycles are often gauged by price trends and sentiment. Sustained price rises (with higher highs) alongside positive market sentiment (e.g. rising on-chain activity) indicate a bull phase. Conversely, falling prices and fearful sentiment mark a bear phase. Macro factors and news (interest rates, regulations) can also tip the balance. Tools like Fear & Greed Indexes and on-chain metrics (active addresses, fund flows) help interpret the cycle phase. Keep in mind that crypto is volatile: short-term trends can reverse quickly. For example, in mid-2025 a hawkish Fed induced a temporary bear-like pullback, which then reversed into a bullish recovery when the Fed turned dovish[6][17]. - Q: What should I watch in market data for crypto cycles?

A: Key indicators include on-chain activity (transaction volumes, active addresses), fund flows (capital inflows/outflows into crypto investment products[17]), and dominance indices (e.g. Bitcoin’s market share). For instance, a drop in on-chain metrics (like Glassnode’s recent 17% fee decline[43]) can signal waning demand. Chart patterns (support/resistance levels, moving averages) remain useful, but always cross-check with fundamentals: if wallets are dormant and TVL in DeFi is shrinking, that confirms a cooling market. - Q: Will Bitcoin’s halving cause a big price spike?

A: Historically, Bitcoin halvings have led to major bull runs months later, due to reduced supply issuance. However, many analysts believe much of that effect may already be priced in, especially with ETFs and macro forces at play. As noted by experts, current market conditions (ETFs, interest rates, global liquidity) might matter more than the halving itself[51][52]. In short, while halvings are generally bullish structural events, they don’t guarantee immediate price jumps – external factors still play a large role. - Q: How do regulatory changes (like SEC or MiCA rules) affect Crypto Market Cycles?

A: Regulation can cause volatility in the short term. For example, news of MiCA stablecoin rules in Europe (requiring exchanges to delist non-compliant coins) initially spooked markets in early 2025[35]. In practice, market participants adapted (USDT swapping to MiCA-compliant USDC[36]), but the uncertainty caused swings. Similarly, enforcement actions or guidance in the US can lead to sell-offs (e.g. early 2025 SEC announcements). Long-term, clear regulation usually supports markets by reducing uncertainty. Following such updates closely (via sources like CoinDesk or law firm summaries) is wise. - Q: What does “on-chain analysis” mean and why use it?

A: On-chain analysis studies blockchain data to gauge network health and user behavior. Unlike price alone, on-chain metrics (active addresses, transaction counts, fees, staking growth) reflect real usage. For instance, a rise in Bitcoin active addresses or Ethereum smart contract deployments suggests growing adoption. Conversely, declining on-chain activity can warn of fading momentum[43]. Traders often use on-chain signals (from Glassnode, CryptoQuant, etc.) to confirm trends or spot divergences. While not foolproof, on-chain analysis provides objective data beyond price charts. - Q: Is crypto a good hedge against inflation and economic crisis?

A: Crypto proponents often call Bitcoin “digital gold,” citing scenarios where it held value during fiat inflation. There are cases (e.g. in countries with unstable currencies) where crypto use surged as a value store. However, crypto prices are also highly volatile and influenced by broader risk sentiment. In 2024–25, crypto assets reacted strongly to U.S. inflation reports and Fed policy expectations[6]. Many experts believe crypto can diversify an investment portfolio, but it should be balanced with traditional hedges (gold, bonds). Remember, during global crises, crypto sometimes temporarily drops with other risk assets before rallying later. - Q: How do NFTs and DeFi fit into the long-term outlook?

A: NFTs and DeFi are viewed as major growth areas, but with different maturity stages. DeFi has become a stable alternative finance system for many users, offering lending, swaps, and yield on crypto. Its TVL and user count keep growing[28]. NFTs have entered applications beyond art – notably gaming and collectibles, which account for significant market volume[32]. Experts believe sustainable NFT niches (gaming, utility projects) will persist, while fad-driven projects may fade. Both sectors will evolve: DeFi is adding real-world assets and insurance, while NFTs are integrating with AR/VR and online identity. Investors should watch these ecosystems for infrastructure (like layer-2 scaling for Ethereum, cross-chain bridges) that improve usability, and focus on projects with clear use-cases rather than hype alone. - Q: How can retail investors track crypto trends and data?

A: Use reputable platforms for up-to-date info. Market data sites like CoinGecko and CoinMarketCap provide current prices, volume, and market caps (as cited above)[5][1]. News outlets (CoinDesk, Bloomberg Crypto, The Block) cover daily headlines on regulation and big events. On-chain analytics services (Glassnode, CryptoQuant, Dune Analytics) offer charts of network metrics. Trading charts (TradingView, CryptoCompare) help with technical analysis. Finally, read reports from research firms (CoinShares, Glassnode, Messari) which often blend data with commentary. The key is to cross-reference: always verify big moves with on-chain or official data rather than just social media tips. - Q: What role do stablecoins and CBDCs play in crypto markets?

A: Stablecoins (like USDT, USDC) are the plumbing of crypto markets. They provide fiat-like stability and liquidity on-chain – most trading pairs on exchanges use stablecoins. A shock to the stablecoin market (e.g. a peg breaking or regulatory clampdown) can ripple through crypto prices. For instance, MiCA’s treatment of stablecoins directly affected trading behavior in the EU[35][36]. CBDCs (central bank digital currencies) are still mainly a public policy development. While they are not part of crypto markets, they represent the growing digitalization of money. In the long run, successful CBDCs might reduce demand for private stablecoins, but they also validate the concept of digital money. Investors keep an eye on CBDC news for the broader acceptance of blockchain technology, but as of 2025 CBDCs have only an indirect effect on crypto prices. - Q: How should I manage risk in crypto investments?

A: Adopt traditional risk management principles adapted for crypto’s volatility. Diversify your holdings (don’t put all funds in one coin or token). Use allocation limits (e.g. decide what percentage of your portfolio is crypto versus stocks/bonds). Consider dollar-cost averaging (buying at intervals) rather than lump-sum investing. Use staking or yield strategies cautiously (understand lock-up periods). Keep some assets in stablecoins or fiat to hedge short-term downturns. Advanced investors use stop-loss orders or options hedges (calls/puts on BTC, for example). Always do your own research on projects before investing, since crypto projects can fail. As one analyst wrote, since there’s “no lender of last resort” in crypto, it’s critical to have insurance and hedging plans[50]. Regularly rebalance your portfolio – if one asset has grown much larger than intended, sell some to lock profits. Finally, secure your holdings (hardware wallets, reputable custodians) to mitigate theft risk. In summary, treat crypto with as much discipline as any other investment: know your risk tolerance, set limits, and don’t chase emotional trades.