Introduction

Purpose of the Article: This comprehensive article provides readers with the latest updates and trends in the crypto market as of today. In an industry as fast-moving as cryptocurrency, staying updated with current trends is crucial for both investors and enthusiasts. Market dynamics can shift rapidly, and new technologies or regulations can emerge with significant impact. Our goal is to arm readers with timely insights into market movements, technological innovations, regulatory changes, and adoption trends shaping crypto in 2025.

Why Staying Updated Matters: Crypto markets are notorious for their volatility and innovation pace. Those who stay informed via trusted platforms (e.g. CoinDesk for news, Glassnode for on-chain analytics, Bloomberg Crypto for macro perspective) are better equipped to navigate the risks and opportunities. Whether you are managing an investment portfolio or simply passionate about blockchain technology, understanding current trends – from Bitcoin’s price trajectory to DeFi’s growth – is essential. This article pulls data and insights from reputable sources including CoinDesk, CoinMarketCap, CoinShares, Glassnode, Messari, and Bloomberg Crypto, ensuring that the information reflects the state of the market as of August 2025.

Key Themes Covered: We will explore several key themes: (1) Market Movements – the performance of major cryptocurrencies and the overall market; (2) Technological Innovations – including blockchain interoperability milestones like cross-chain bridges, scalability upgrades, and security improvements; (3) Regulatory Updates – how global policies and legal cases are influencing the industry; (4) Adoption Trends – the latest in retail/institutional adoption and market sentiment; (5) On-Chain Activity – what blockchain data reveals about network health; and (6) Future Outlook – emerging trends such as NFTs, DeFi evolution, and the role of stablecoins/CBDCs. By covering these areas, readers will gain a 360° view of where the crypto market stands today and where it might be headed.

Blockchain Interoperability Highlight: Notably, 2025 has seen significant progress in blockchain interoperability. Cross-chain bridges – protocols enabling assets and data to move between different blockchains – are reaching new milestones. This development addresses a long-standing silo problem in crypto: previously, Bitcoin, Ethereum, and other chains were like separate islands. Now, solutions like Polkadot’s XCMP, Cosmos’s IBC, and Chainlink’s CCIP are linking ecosystems, allowing value to flow freely between networks. As we delve into market and tech trends, we’ll also explain how these cross-chain bridges work and why they are critical for the future of a connected crypto economy.

Global Market Trends

Current Market Performance & Capitalization

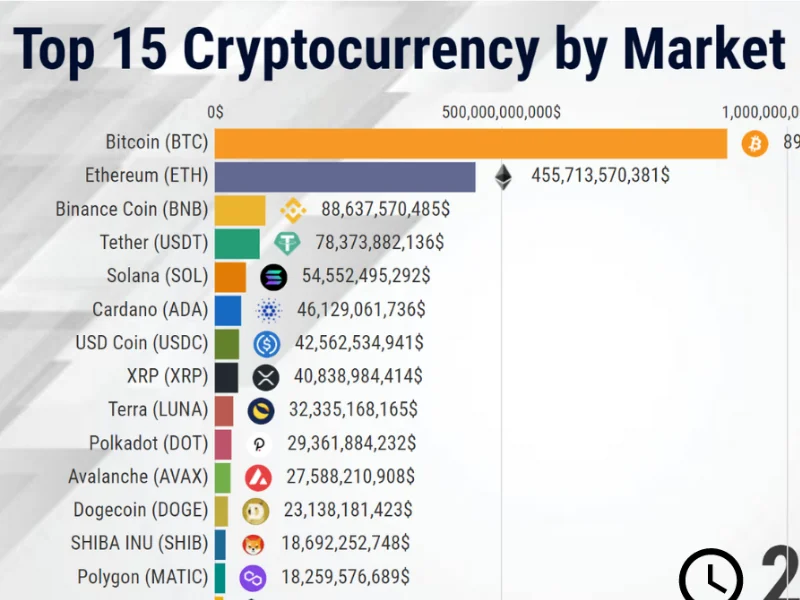

The global cryptocurrency market is in a robust state in 2025. The total market capitalization of all cryptocurrencies currently hovers around $3.86 trillion, reflecting a tremendous recovery and growth (over +67% year-on-year) after the bear markets of 2022–2023. For context, as of April 2025 the market cap was about $2.76T, so the continued rally into late 2025 has pushed valuations to new all-time highs. Bitcoin (BTC), the leading cryptocurrency, now boasts a market cap of roughly $2.18 trillion – over 56% of the total market, with its price well into six figures. Ethereum (ETH), the second-largest asset, makes up about 13.8% of the market (approximately a ~$530B market cap), trading near its record price around the mid-$4,000s. In fact, Bitcoin’s price surpassed the $100,000 milestone for the first time in 2025, and Ether hit a new peak above $4,800. These achievements underscore the bullish momentum driving the market this year.

Major altcoins have likewise seen significant appreciation. Many top 10 cryptocurrencies – including Binance Coin (BNB), Solana (SOL), and others – have outperformed expectations over the past year amid renewed investor enthusiasm. Daily trading volumes remain high (hundreds of billions of dollars), and market liquidity is markedly improved compared to the liquidity crunch experienced during the 2022 bear market. Short-term price trends show healthy volatility: for example, in recent weeks Bitcoin has traded in the $105K–$115K range, experiencing typical 5–10% swings, while Ether has fluctuated around $4K–$4.8K. Trend analysis reveals that over the last 7 days, most large-cap crypto prices have risen a few percent, continuing an uptrend fueled by positive news (like ETF inflows and tech upgrades). In the last 24 hours, the market saw a minor pullback (~2% dip) – a normal breather after weeks of gains. Analysts note that such corrections are healthy for a sustained rally. Overall, sentiment is bullish, with year-to-date returns for Bitcoin and Ether solidly positive (BTC up over +80% YTD, ETH up +60%+). Key market events driving recent changes include the introduction of multiple spot Bitcoin ETFs (which began in early 2024) attracting fresh capital, and Ethereum’s successful protocol upgrades boosting confidence (more on these later). In summary, global crypto market performance in 2025 is strong, with total capitalization reaching new highs and leading assets showing resilience despite occasional volatility.

Embedded data: According to CoinGecko’s global chart, “the global cryptocurrency market cap today is $3.86 Trillion, a -2.29% change in the last 24 hours and 67.4% change one year ago.” Bitcoin alone accounts for over $2.1T of that, reflecting BTC dominance around 56.5%, while all stablecoins combined have a ~$282B market cap (about 7.3% of the total). These figures illustrate how dominant Bitcoin remains, and how significant stablecoins have become as a portion of crypto’s value.

Price Fluctuations & Drivers: In the short term, crypto prices respond to a mix of technical and fundamental drivers. Over the past month, Bitcoin saw a brief dip of ~10% from its record highs (~$123K down to ~$110K) when profit-taking set in and on-chain data showed an extremely high percentage of holders in profit (a classic sell signal). However, macroeconomic news quickly turned favorable – the U.S. Federal Reserve signaled dovish policy shifts at the Jackson Hole symposium in late August, boosting investors’ risk appetite. This “dovish turn” from the Fed sparked a rotation of capital back into crypto, lifting assets like XRP and others during that week. One CoinDesk market piece noted: “dovish comments from Fed Chair Jerome Powell… strengthened expectations of September rate cuts and triggered rotation into risk assets, including cryptocurrencies”. Indeed, macro conditions such as expectations of interest rate cuts or concerns about inflation can greatly influence crypto sentiment. In the current climate, cooling inflation and the prospect of easier monetary policy have been tailwinds for Bitcoin’s “digital gold” narrative. At the same time, market-specific events like large ETF buy-ins or network upgrades have immediate impacts – for example, when Ethereum successfully implemented its Shanghai upgrade (enabling staking withdrawals) in 2023, ETH saw a strong rally as technical uncertainty cleared. Similarly, in mid-2025, news of BlackRock’s Bitcoin ETF crossing significant AUM or tech giant MicroStrategy increasing its BTC holdings can trigger positive price momentum.

Looking at 24h and 7d trends, as of today most top cryptos are modestly in the green week-over-week. Bitcoin is up roughly 3% this week, Ether about 5%, while some altcoins (e.g. Solana, Cardano) have notched high single-digit gains, partly on the back of a renewed appetite for risk among retail traders. We also saw sector rotation: capital flowed into large-caps after Bitcoin’s ETF-driven surge, and now some DeFi tokens and Layer-2 tokens are catching a bid as investors search for value outside the already pumped majors. Overall market volatility is moderate: the Bitcoin Volatility Index is around 50 (lower than the 2021 peak mania levels, indicating a more mature market). It’s noteworthy that crypto’s total market cap (>$3.8T) now exceeds the market cap of some G7 stock exchanges, highlighting how far this asset class has come in terms of global economic significance.

Institutional Involvement & Economic Influence

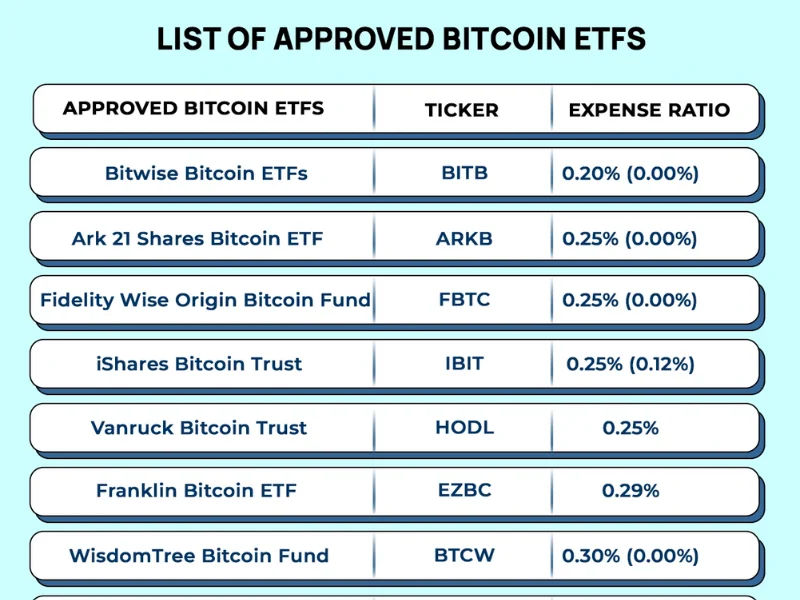

One of the defining trends of the current cycle is deepening institutional involvement in crypto markets. Large corporations, fund managers, and even nation-states are now active participants, bringing significant capital and influencing market dynamics. Companies like MicroStrategy continue to add Bitcoin to their balance sheets (MicroStrategy’s holdings have grown to well over 160,000 BTC by 2025, worth tens of billions of dollars), and Grayscale’s Bitcoin Trust (GBTC) has seen its discount vanish as it transitions toward a likely ETF conversion. More dramatically, spot Bitcoin ETFs launched in the U.S. in January 2024 have amassed huge inflows – “11 spot BTC ETFs have amassed $53.7 billion in investor wealth since their debut in January last year”, according to CoinDesk. This flood of institutional money via ETFs has created a significant new source of demand that helped propel Bitcoin above $100K. Ether ETFs likewise have gathered over $12.4B in inflows, reflecting institutional confidence in Ethereum post-Merge.

Institutional investors are also influencing market structure through digital asset fund flows. Recent data from CoinShares (a leading digital asset manager) shows that crypto investment products hit record assets-under-management (AUM) this year. In one mid-August weekly report, “digital asset investment products saw US$3.75 billion inflows, the fourth-largest on record, driving AuM to an all-time high of US$244 billion”. Notably, that week nearly all inflows went to a single provider (BlackRock’s iShares ETF) as it launched, with the United States accounting for 99% of the flows. Such concentration underscores how a few big players can swing the market. The same report highlighted that Ethereum-dedicated funds led the charge, receiving 77% of that week’s inflows (US$2.87B) – a sign that institutions are increasingly interested in ETH alongside BTC. Bitcoin funds saw about $552M inflows that week, while even altcoins like Solana and XRP attracted sizeable institutional money (>$100M each). These trends reveal that institutions are not only holding crypto directly but using investment vehicles to gain exposure, which adds liquidity and (arguably) stability to the market.

Market sentiment among big investors has also been swayed by macroeconomic conditions. The ongoing global economic uncertainty – from inflation concerns to recession fears – plays a dual role. On one hand, high inflation in fiat currencies has driven some investors to view Bitcoin as an inflation hedge or “digital gold.” During 2022’s inflation spike, for instance, Bitcoin’s narrative as a store of value gained traction even though short-term correlation with stocks remained. On the other hand, recession fears and higher interest rates can make speculative investments less attractive. Throughout 2023–2024, central banks tightened monetary policy, which pressured risk assets including crypto. However, by 2025 the outlook shifted: inflation began to moderate and there’s growing anticipation of rate cuts or at least a pause. This more dovish macro outlook has reduced the headwinds for crypto. In late August 2025, after Fed Chair Powell’s speech hinted at potential easing, we saw a noticeable uptick in crypto prices and volumes – indicating that liquidity conditions (fueled by central bank policy) remain a key external factor.

Another angle is institutional adoption beyond investment – for example, mainstream financial firms providing crypto services. We’ve seen major banks like Goldman Sachs and Morgan Stanley expand crypto offerings for clients, and payment giants like PayPal launching their own USD stablecoin. These moves increase the credibility and integration of crypto into traditional finance. Additionally, sovereign adoption is in play: El Salvador’s pioneering move to adopt Bitcoin as legal tender in 2021 has influenced other nations (we now see countries like Panama and Paraguay exploring crypto-friendly legislation, and some governments holding Bitcoin in reserves).

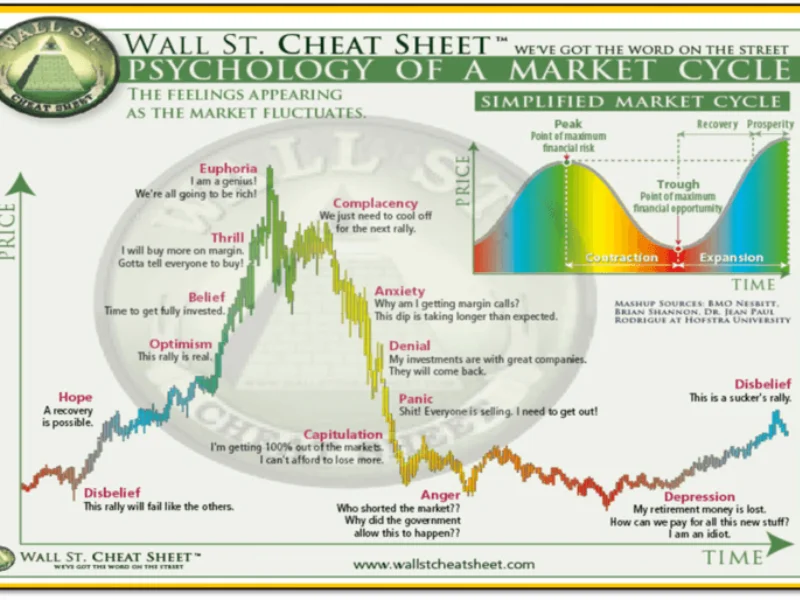

Market Sentiment & Economic Conditions: As of Q3 2025, market sentiment is cautiously optimistic. Global economic uncertainties, such as high government debt levels and geopolitical tensions, are actually contributing to crypto’s appeal as a hedge or alternative asset. For instance, concern over the U.S. debt ceiling and bond market volatility has some investors reallocating into Bitcoin, which is perceived as uncorrelated to traditional financial system risks. A Cooper Research report noted that “economic uncertainties drive investors to park funds in risk-on investments, including spot Bitcoin ETFs”, which helped BTC hit new highs above $120K. At the same time, market sentiment indicators like the Crypto Fear & Greed Index have mostly stayed in “Greed” territory throughout 2025, occasionally tipping to “Extreme Greed” during price surges – a sign that bullish sentiment has been dominant. However, analysts warn that too much euphoria can precede a correction; indeed, on-chain metrics recently showed ~94% of Bitcoin supply in profit (meaning most investors would have gains if they sold), a condition that “raises the risk of… profit-taking… which could trigger a sentiment shift and increased volatility”. In other words, if everyone is sitting on profits, the temptation to realize gains grows, which could swiftly turn greed into fear.

In summary, institutional involvement is at an all-time high – from ETFs and corporate treasuries to hedge funds deploying sophisticated strategies – and this is providing new support levels and liquidity to crypto markets. Meanwhile, economic factors like inflation and monetary policy continue to influence the crypto narrative. Crypto is increasingly seen as part of the broader financial landscape, affected by (and sometimes countering) traditional economic trends. The presence of big players has not eliminated volatility, but it has perhaps extended crypto’s reach and legitimacy. As we move forward, the interplay between Wall Street and crypto, and between macroeconomics and digital assets, will remain a pivotal aspect of market trends.

Technological Developments and Innovations

Blockchain Advancements

The year 2025 has been marked by significant technological progress in blockchain platforms, with a strong emphasis on scalability, efficiency, and interoperability. One of the headline advancements is the successful transition of Ethereum to its proof-of-stake upgrade (often referred to as Ethereum 2.0). Ethereum’s switch from proof-of-work (completed in the September 2022 Merge) drastically reduced its energy usage by >99% and set the stage for further upgrades focused on scalability. Since then, the Ethereum roadmap has delivered Shanghai (2023) – enabling staked ETH withdrawals – and introduced improvements like proto-danksharding (EIP-4844) in 2024 to increase Layer-2 throughput. These upgrades are beginning to bear fruit: Ethereum’s network now handles more transactions at lower fees thanks to Layer-2 scaling solutions (Optimistic and ZK-Rollups) that have gained mass adoption. In fact, daily transaction count combining Ethereum L1 and L2s is at an all-time high, and user activity is booming on chains like Arbitrum and Optimism which settle on Ethereum. Glassnode data shows that Ethereum’s staking participation rate hit 29.6% in early 2025 (up 4% QoQ), meaning nearly 30% of all ETH is now locked in staking, securing the network and earning yield. This high staking rate not only reflects confidence in the network’s proof-of-stake security, but also effectively removes a large chunk of ETH from circulating supply, which can have bullish price implications. Institutional players are directly participating too – about 7% of all ETH is held by institutional entities via custodians or staking services, attracted by the ~5% APY staking rewards, something Bitcoin doesn’t offer. The net effect of Ethereum’s advancements is a more scalable and robust network: transaction fees on ETH L1 have been moderate most of the year (except for brief NFT-mint mania spikes), and user experience is improving with account abstraction (smart contract wallets) making transactions smarter and more secure.

Other Layer-1 blockchain projects have also pushed technological frontiers. Solana, for example, has focused on high throughput and speed, and despite some outages in 2022, it has emerged in 2025 as a performant chain with real-world usage in finance and gaming. Solana’s network can handle 65,000+ TPS and recent upgrades improved its reliability. An interesting stat: Solana’s active addresses and daily transaction volume have exploded, now even surpassing those of Bitcoin and Ethereum by some measures. According to a joint Gemini/Glassnode report, “Solana now settles $37B daily, more than both Bitcoin and Ethereum, reflecting a rapid rise in network activity”. Additionally, that report noted “Solana’s active addresses exceed Bitcoin’s by 16.2x and Ethereum’s by 24.6x” – a striking figure highlighting how a fast, low-cost chain can attract masses of users (though many may be micro-transactions or bot activity, it still underlines Solana’s capacity). Technologically, Solana uses a unique proof-of-history combined with proof-of-stake, enabling block times of ~400ms. Its success demonstrates that alternative consensus algorithms and L1 designs can achieve high scalability, though often at the cost of higher hardware requirements. Another project, Algorand, made strides in cryptographic innovation by implementing State Proofs (a kind of trustless bridge mechanism) and boosting its TPS. Cardano rolled out more smart contract enhancements and sidechains to improve throughput. Polkadot and Cosmos have been pivotal in interoperability (more on that below). And new consensus mechanisms like Avalanche’s subnet architecture or Algorand’s pure proof-of-stake show that the space is rife with experimentation aimed at solving the blockchain trilemma (scalability, security, decentralization).

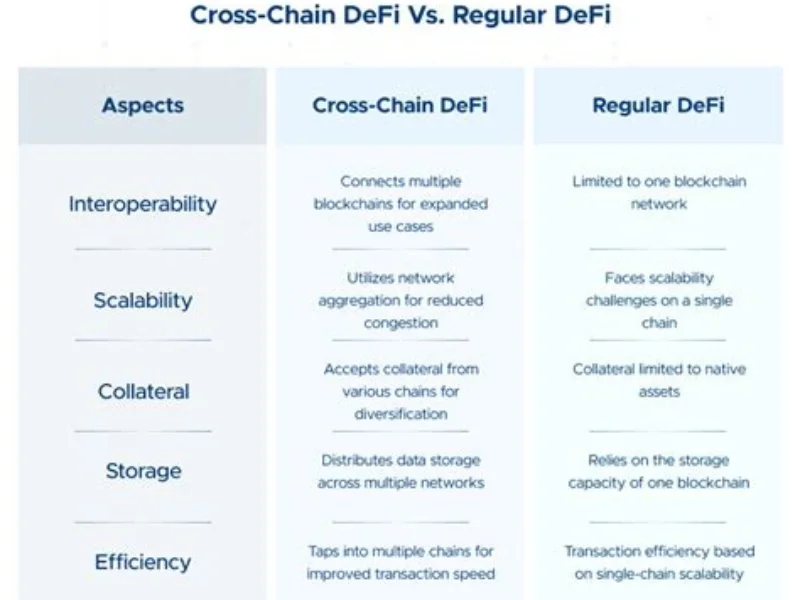

A major milestone in 2025 is blockchain interoperability, epitomized by progress in cross-chain bridges. Historically, blockchains were isolated networks, but there’s a push to enable assets and data to move between chains seamlessly. Projects like Polkadot (with its XCMP – Cross-Chain Message Passing between parachains) and Cosmos (with IBC – Inter-Blockchain Communication protocol) have matured. As of mid-2025, Cosmos IBC connects dozens of zones (chains) enabling token transfers and interoperability among an expanding “internet of blockchains.” Polkadot, similarly, now has many parachains in production that can communicate under the shared security of the Relay Chain. Meanwhile, generalized bridge protocols have come to the fore: Chainlink’s Cross-Chain Interoperability Protocol (CCIP) launched and is being adopted as a standard messaging layer between blockchains and traditional systems. This is seen as a “blockchain interoperability milestone”, as CCIP aims to securely connect smart contracts across chains. Industry analysis highlights that “cross-chain bridges like Wormhole and Chainlink CCIP will be critical for asset transfers and data verification” in the coming era. In practice, these innovations mean a user could, say, move a stablecoin from Ethereum to Solana or execute a multi-chain smart contract operation more easily than before. It breaks down silos: liquidity can flow to where it’s most needed, and developers can build applications that tap into multiple networks’ strengths. However, it’s worth noting that bridges also come with security challenges – in the past, bridges were targets of some of the largest hacks (e.g., Wormhole in 2022). In response, new decentralized security models are being deployed for bridges, including permissionless validators and multi-party computation to secure cross-chain transactions. Overall, the advancement in interoperability is one of 2025’s defining tech trends, likely to reshape how we perceive “the crypto ecosystem” (as a more interconnected web rather than isolated communities).

In summary, blockchain technology in 2025 is more advanced, scalable, and interconnected than ever. Ethereum’s evolution shows that even the largest networks can upgrade without major issues (post-Merge, Ethereum is handling more activity and rewarding stakers, all while being far more energy-efficient). Competing L1s have innovated to carve out niches (high-speed finance on Solana, interoperable zones in Cosmos, etc.). And critically, the walls between blockchains are starting to come down with interoperability protocols – a development that could be as important as early internet protocols were for connecting information networks. These advancements collectively pave the way for broader adoption: as blockchains become faster and user-friendly (with lower fees and higher throughput), new applications (from DeFi to gaming to supply chain) can reach mainstream-ready performance. In the next sections, we’ll see how these tech improvements feed into security enhancements and smart contract innovations.

Security Enhancements in Crypto

Security remains a paramount concern in the crypto space, and recent innovations are significantly bolstering the safety of blockchain networks and applications. A major focus area has been smart contract security – given the billions of dollars locked in DeFi protocols, any vulnerability can be catastrophic. In response, the industry has invested heavily in audits, formal verification of code, and new programming models to reduce bugs. For instance, newer smart contract languages like Rust (used in Solana) or Move (from the Diem project, adapted by Aptos and Sui) are designed with safety in mind, featuring safeguards against common errors. Ethereum’s community has embraced practices like OpenZeppelin’s standardized libraries and bug bounty programs to harden contract code. We’ve also seen growth in decentralized insurance (covering smart contract hacks) and better tooling for runtime monitoring of contracts (e.g., tools that can pause suspicious protocol behavior).

One of the most exciting frontiers in security is the rise of Zero-Knowledge Proofs (ZKPs). ZKPs are cryptographic methods that allow one party to prove something to another without revealing underlying information – “verifying transactions or identities without revealing private data”. This technology is crucial for privacy and scalability. ZK-Rollups on Ethereum (like StarkNet, zkSync) use zero-knowledge validity proofs to bundle thousands of transactions off-chain and prove their correctness on-chain, greatly improving throughput while preserving security. ZKPs also enable privacy-preserving transactions – for example, projects like Aztec Network allow shielded transfers on Ethereum using ZKPs (so value can be sent without publicly linking to addresses). Furthermore, ZKPs are being explored for identity verification (proving you have certain credentials or attributes without revealing them, which could be revolutionary for KYC/AML in a non-intrusive way). The importance of ZKPs has not gone unnoticed by standard-setters: the U.S. National Institute of Standards and Technology (NIST) has an initiative to standardize zero-knowledge proof protocols by 2025, aiming to create common, secure frameworks for their use. As one CryptoSlate report notes, “NIST’s 2025 deadline for zero-knowledge proofs aims to standardize privacy technology for a secure web3 era”. This standardization push underscores how critical ZKPs are expected to be for Web3’s future – ensuring that privacy-enhancing features can be widely and safely adopted.

Another aspect of security innovation is the advent of decentralized security services. For example, decentralized oracles (Chainlink, Band Protocol) have improved to securely feed off-chain data to smart contracts, using techniques like consensus among multiple nodes and economic incentives to prevent tampering. Secure oracles help prevent exploits like price manipulation attacks in DeFi. Similarly, decentralized randomness beacons (for fair random number generation on-chain) and threshold cryptography schemes (where keys are distributed among many nodes to eliminate single points of failure) are more prevalent, enhancing security for things like cross-chain bridges and multi-sig wallets.

A key case study in smart contract security is Ethereum’s move toward Account Abstraction. In 2025, Ethereum introduced upgrades (like EIP-4337 in 2023 and EIP-7702 in 2025) that allow externally owned accounts (user wallets) to behave more like smart contracts. This enables features such as multisig wallets, social recovery, and gas fee delegation natively at the protocol level – effectively making wallets smarter and less prone to user error (losing keys, etc.). With account abstraction, users can have wallets with built-in fraud checks or rate limiters, enhancing security for the average person. However, these powerful features come with new complexities. An analysis of Ethereum’s recent Pectra hard fork (May 2025), which introduced EIP-7702, shows both sides: on one hand, “the upgrade unlocks advanced features like gas sponsorship (users can make transactions without holding ETH for fees) and transaction batching, improving UX”. On the other hand, it “introduced new attack vectors… attackers exploit the ability to bundle malicious actions into a single transaction”. Indeed, shortly after that upgrade, there was a phishing exploit where a user approved what looked like a simple token swap, but the single “batched” transaction also secretly transferred NFTs and other tokens, causing a $1.5M loss. Security firms observed that over 90% of early EIP-7702 delegated transactions were malicious – essentially attackers testing the new functionality. The Ethereum community responded by educating users and improving wallet filters (e.g., MetaMask now flags or blocks suspicious batch requests), and by encouraging multi-layered security: using audited smart contract wallets, setting spending limits, and requiring multisig for large amounts. This episode underscores a broader theme: as blockchain tech becomes more powerful, continuous security enhancements are needed. The good news is that the community is increasingly proactive – for instance, when such exploits occur, white-hat hackers and analysts often dissect them and teams issue patches rapidly. Contrast this with 2016 (The DAO hack) or 2017 (Parity wallet bug) when the ecosystem was less prepared.

Beyond smart contracts, at the blockchain network level, consensus security is improving. Bitcoin’s hash rate hit new all-time highs in 2025 (thanks to more mining operations and technological improvements in mining hardware), making the network more secure against 51% attacks than ever. Ethereum’s shift to PoS and the slashing mechanism have thus far kept the network stable with no malicious forks, proving the viability of PoS at scale. Smaller proof-of-work chains that were once at risk of attacks have either shifted to merge-mining or adopted new algorithms to reduce such risks.

We’re also seeing increasing use of formal verification (mathematically proving the correctness of code) for critical smart contracts, particularly in high-value DeFi protocols. Projects like Aave, Compound, and Uniswap V3 underwent rigorous formal verification and multiple audits. The concept of “runtime bug bounties” – contracts with embedded rewards for finding vulnerabilities – has emerged, turning security into a more continuous community effort.

In summary, crypto in 2025 is significantly bolstered by security innovations at multiple layers. Zero-knowledge proofs are providing privacy and integrity in new ways, likely to become standardized and ubiquitous[1]. Smart contract platforms are learning from past exploits and adding features (like account abstraction and improved oracles) to prevent common attack vectors. While new features can introduce new risks (as seen with Ethereum’s EIP-7702 phishing cases), the collective response shows a maturing industry that prioritizes security. The mantra “don’t trust, verify” is taken seriously: many DeFi platforms now have open-source code, multiple audits, real-time monitoring dashboards (e.g., Nansen alerts for large transfers), and insurance funds as fallback. And importantly, user education is improving; more crypto users are aware of basic security hygiene (hardware wallets, double-checking URLs, not signing strange transactions). All these enhancements help build trust – a crucial ingredient if crypto is to achieve mainstream adoption. After all, every highly publicized hack or scam not only harms direct victims but also dents the ecosystem’s reputation. The investments in security are, therefore, investments in the future credibility and success of blockchain technology.

Impact of Smart Contracts and dApps

Smart contracts and decentralized applications (dApps) have continued to expand their role in reshaping industries, with 2025 witnessing significant growth especially in the realm of decentralized finance (DeFi) and beyond. DeFi remains the flagship use case for smart contracts, essentially creating an alternative financial system running on code. Platforms for lending, borrowing, trading, and asset management have grown more sophisticated and user-friendly. For example, lending protocol Aave has deployed multiple versions across Ethereum and Layer-2 networks, now offering features like credit delegation and collateral swapping. As of mid-2025, Aave has the highest Total Value Locked (TVL) among DeFi protocols at about $24.4 billion. This indicates robust usage – individuals and institutions are entrusting smart contracts with tens of billions in assets to earn yield or access liquidity. Similarly, Uniswap, the leading decentralized exchange (DEX), routinely facilitates daily trading volumes around $3–5 billion, rivaling some major centralized exchanges. Uniswap’s latest iteration (v4) introduced customizable hooks for market makers, further blurring the line between traditional and decentralized trading by improving capital efficiency and flexibility. The success of these dApps showcases how smart contracts enable financial services that are open to anyone with an Internet connection, operating 24/7 without intermediaries.

Beyond finance, smart contracts are driving innovation in areas like digital art, gaming, and supply chain. The rise of Non-Fungible Tokens (NFTs) in 2021–2022 (for digital art and collectibles) has evolved into more practical use-cases in 2024–2025. NFTs are now being used in gaming (in-game assets that players truly own and can trade), music (royalty shares and fan membership tokens), and brand engagement (big brands issuing NFTs for loyalty or as digital twins of physical products). The concept of “NFT 2.0” involves more utility – for instance, owning a certain NFT might grant you access to exclusive content, events, or community governance. Decentralized applications in the metaverse and virtual real estate also rely on NFTs to represent land or items. While the initial hype has toned down (global NFT market revenue in 2025 is projected around $500M, slightly down from 2024), the foundation laid by NFTs has normalized the idea of unique digital property. As a result, industries like gaming have started to incorporate NFT-based economies (play-to-earn models and player-owned assets). An example: Axie Infinity’s model proved conceptually that gaming economies can be player-owned, and now mainstream studios are exploring blockchain for item ownership in games (Ubisoft, Square Enix, etc. have pilot projects). On the enterprise side, supply chain dApps use smart contracts for provenance tracking – e.g., verifying a product’s journey from origin to store. Companies like Maersk and Walmart have trialed private versions, and with interoperability improvements, we may see cross-company supply chain networks on public-permissioned chains to ensure data immutability and transparency.

Crucially, smart contracts are enabling entirely new industries like DeFi to flourish at an extraordinary pace. Consider that as of early 2024, DeFi TVL (total value locked) globally was around $54B, and by Q1 2024 it had jumped to $93B. By mid-2025, DeFi TVL is roughly $156 billion spread across various chains, having recovered and exceeded the previous peak from late 2021. This growth is not just on Ethereum; multi-chain DeFi is a reality. Chains like Binance Smart Chain, Solana, Avalanche, and Polygon each command several billions in TVL, often carving niches (e.g., Tron has a large stablecoin-focused TVL, Solana for high-speed trading, etc.). According to DefiLlama, Ethereum still leads with about $46.3B TVL (30% of total) as of June 2025, followed by chains like Solana ($7.2B) and BSC ($5.5B). These dApps have effectively open-sourced finance, allowing people to lend or borrow without a bank, trade without an exchange operator, or earn yield without a fund manager – all regulated by code.

Another area where smart contracts/dApps are making an impact is decentralized governance and DAOs (Decentralized Autonomous Organizations). In 2025, many protocols and even some non-crypto communities are governed by token holders through smart contract voting. While DAO governance has had challenges (voter apathy, whale dominance), it has matured with better frameworks and tools. Notably, Compound and Uniswap have each executed dozens of governance proposals to upgrade their protocols or allocate treasury funds – essentially evolving live services via on-chain voting. There are also “service DAOs” now, which function like distributed companies (for example, a group of contributors worldwide coordinating via tokens to deliver some product or service). This is an ongoing experiment in organizational structure enabled by dApps like Snapshot (for voting) and Gnosis Safe (for treasury management).

Importantly, smart contracts are starting to interface with real-world assets (RWAs) – a trend bridging DeFi with traditional finance. We see this in tokenized real estate, bonds, and invoices being used as collateral or yield-bearing instruments in DeFi. Platforms like MakerDAO have begun to onboard real-world assets (e.g., tokenized short-term loans, real estate-backed loans) to diversify collateral beyond crypto. By 2025, over $1B in RWA value is locked in DeFi protocols (small relative to total crypto TVL, but growing). One analysis noted that Ethereum holds “80% of RWA tokenization, with $7.72 billion locked in structured notes and other instruments” by mid-2025. This indicates that smart contracts are encroaching into traditional finance territory – imagine a future where corporate bonds or stocks are issued as tokens on a blockchain, and then managed or traded via smart contracts without the need for the current web of intermediaries. We’re already seeing early steps: governments like Singapore have done trials of issuing bonds on public chains, and firms like JPMorgan created private blockchain bonds.

All these developments underscore how dApps are shaping new industries and transforming old ones. Decentralized finance is the clearest example – it’s essentially Wall Street recreated in code, accessible globally and permissionlessly. NFTs and blockchain gaming are reshaping how creators monetize and how players own value in digital worlds. Supply chain and enterprise uses are making operations more efficient and transparent. There’s also growth in decentralized social media and content platforms (like Lens Protocol, Mirror, etc.), aiming to give users ownership of their content and data rather than ceding it to centralized tech giants.

As Messari and Dune Analytics often report, user metrics for many dApps are on an upward trend – e.g., monthly active users of top DeFi dApps are in the hundreds of thousands and growing. Dune dashboards show cumulative wallet counts interacting with DeFi protocols reaching new highs, while on-chain metrics like active addresses and transaction counts support this growth. There are of course headwinds: user experience for dApps, while improving (thanks to better wallets and Layer-2s), can still be daunting for non-technical users. And scaling to millions of users remains a challenge (hence importance of L2s and new L1s). But overall, smart contracts and dApps are steadily advancing from niche experiments to mainstream-ready applications. Each year brings improvements in scalability (so dApps can handle more users), composability (dApps interoperate, like Lego blocks, giving rise to new combined use-cases), and security (fewer hacks as best practices spread).

In conclusion, the impact of smart contracts/dApps is profound and multi-faceted: they have democratized finance through DeFi, redefined digital ownership through NFTs, and are pioneering new models of business and governance via DAOs and tokenization. This is setting the stage for a future where decentralized applications might underpin significant parts of the global economy. As adoption grows – with user-friendly interfaces abstracting away blockchain complexity – we can expect dApps to become as unremarkable in daily use as web or mobile apps are today. The continuous data coming from analytics sites confirms the trajectory: for instance, “retail capital has flowed into all major assets, but Solana has surpassed Ethereum in new investor activity… Solana’s memecoin sector realized cap grew 477%, outpacing Ethereum’s” – highlighting that speculation and innovation continue at a rapid clip, driven by accessible dApps across ecosystems. The key will be maintaining this growth while ensuring stability and user trust, which the aforementioned security and regulatory developments aim to address.

Regulatory and Legal Landscape

Current Regulatory Updates

The regulatory and legal landscape for cryptocurrency in 2025 is markedly clearer in some jurisdictions, while still evolving in others. Global crypto regulation trends have seen significant developments in the U.S., Europe, and Asia, reflecting the growing importance of the sector.

In the United States, after years of ambiguity and “regulation-by-enforcement,” there has been a notable shift. A new U.S. administration (as of 2025) took office and with it came a more crypto-engaged regulatory stance. Early 2025 saw the formation of an SEC Crypto Task Force and a general pivot away from the aggressive enforcement actions that characterized 2023. Remarkably, by mid-2025, the U.S. Securities and Exchange Commission (SEC) appeared to soften its approach: it was poised to drop its high-profile lawsuit against Coinbase, one of the largest U.S. crypto exchanges. Around the same time, the SEC voluntarily dismissed its civil lawsuit against Binance in May 2025. These lawsuits, filed in 2023, had alleged unregistered securities offerings and other violations; their pause or dismissal signals a potential policy pivot to a more collaborative or rules-based approach rather than litigation. Reuters noted this move came as the regulator’s strategy shifted under a more crypto-friendly political environment (even mentioning it was “extending the regulator’s new approach… since President Donald Trump reentered the White House.”). While these U.S. cases are complex and ongoing (with Binance also facing DOJ scrutiny and international probes), the freeze in SEC action hints that clearer legislation might be in the works to define how exchanges and tokens are regulated. Indeed, Congress has been debating bills – such as the Digital Commodities Consumer Protection Act (DCCPA) and others – which could delineate SEC vs CFTC authority and set guidelines for stablecoins and securities classification. As of now, there is optimism that the U.S. might finally get a comprehensive crypto regulatory framework within the next year or two, to catch up with forward steps elsewhere.

Meanwhile, Europe has taken a lead with the introduction of MiCA (Markets in Crypto-Assets regulation). MiCA was passed in 2023 and is rolling out in stages (with stablecoin and coin offering rules by 2024 and broader exchange and custodial rules by 2025/26). This EU-wide framework provides clear rules on licensing crypto asset service providers, reserve requirements for stablecoin issuers, and investor protection measures. By providing legal clarity, MiCA is widely seen as making Europe a more attractive venue for crypto business relative to the previously patchy U.S. situation. A CoinDesk analysis pointed out: “MiCA is at least three to five years ahead of U.S. crypto regulation in terms of clarity, consistency and implementation”, giving the EU a significant head-start in fostering a regulated crypto economy. MiCA harmonizes rules across the 27 EU countries, meaning a company licensed under MiCA in, say, France can passport its services throughout Europe. This has led several crypto firms to set up in jurisdictions like France, Switzerland (non-EU but aligned on crypto friendliness), and Germany to serve the EU market. Additionally, the UK’s FCA (Financial Conduct Authority), post-Brexit, is crafting its own regime: in 2025 the FCA released a discussion paper seeking industry feedback on regulating areas like crypto lending, DeFi, and stablecoins[2]. The FCA’s stated aim is to “create a crypto regime that ensures market integrity and consumer protection while allowing innovation.” This balanced phrasing is encouraging to industry players, given the UK had been perceived as tough (only ~15% of applicant firms were approved under its prior registration scheme since 2020[3]). The new consultation suggests a more accommodative stance could be coming, likely in 2026 when legislation is expected to be finalized.

In Asia, regulatory stances vary but trend toward legitimization. Japan has long had clear exchange licensing (since 2017) and recently approved Japan’s first yen stablecoin under new laws. Singapore remains a crypto hub with strict but clear rules under the PSA (Payment Services Act) and a forthcoming updated framework for crypto tokens. Hong Kong pivoted in 2023 to allow retail crypto trading under licenses, part of a broader goal to be a crypto finance hub (with possible blessing from mainland China in the background). China itself continues to ban crypto trading domestically but vigorously pursues a central bank digital currency (the digital yuan). Notably, India in 2023 imposed stiff taxes that dampened trading, but by 2025 there are discussions in India’s government about revisiting these policies to not miss out on blockchain innovation (especially as Web3 startups grow). There’s also the Middle East: places like Dubai (UAE) have set up special regulatory bodies (VARA) to license crypto companies, attracting the likes of Binance and Crypto.com to establish presences there.

Legal Cases & Precedents

Several high-profile legal cases have made headlines, and their outcomes are setting important precedents for the crypto industry. We already touched on the SEC lawsuits against Binance and Coinbase – their trajectories (paused or settling) indicate how regulators might prefer negotiated settlements or new rulemaking over protracted court battles that risk unfavorable precedents. Another major case was SEC v. Ripple Labs, concerning whether XRP is a security. In July 2023, a landmark ruling by a U.S. federal judge provided a split decision: sales of XRP to institutional investors (through written contracts) were deemed securities sales, but secondary market sales of XRP (e.g. on exchanges to retail investors) were not. This was seen as a partial win for Ripple and the crypto industry, clarifying that tokens themselves are not inherently securities – context matters. Fast forward to 2025, Ripple’s case has effectively concluded: Ripple decided to drop its planned appeal and paid a fine, after a judge refused to approve a settlement that would have reduced their penalty. So the earlier ruling stands, serving as a key precedent that many other token issuers cite – it suggests that certain “blue chip” cryptocurrencies traded in the open market might not be securities, which has implications for exchanges and investors (e.g., some exchanges relisted XRP after the ruling).

Another high-profile series of cases revolve around crypto exchanges and compliance. The New York Attorney General has been active – in 2023–24, NYAG pursued actions against platforms like KuCoin (even arguing in one case that ETH was a security, though that remains just an assertion). In 2025, regulators cracked down on specific scam exchanges and kiosk operators. For instance, the California DFPI took its first enforcement action under a new state law, fining a Bitcoin ATM operator (Coinme) for failing to follow rules such as transaction limits and disclosures – a sign that even crypto ATMs are being brought into the compliance fold at the state level.

The Department of Justice (DOJ) has also made examples out of illicit use of crypto. A notable case in 2023–24 was the prosecution of individuals behind the Bitfinex hack (2016), where billions in Bitcoin were eventually recovered. In 2025, the DOJ continues to pursue actors using crypto for crime: one such action was the seizure of “BidenCash” marketplace domains (a dark web carding market) along with crypto funds. Another was a civil forfeiture action to seize over $7.7M in cryptocurrency linked to North Korean money laundering by IT workers[4]. These enforcement actions underscore that while crypto transactions are pseudonymous, law enforcement has become very adept at blockchain analysis, and crypto is far from a safe haven for criminals – a narrative shift from the early days when skeptics claimed crypto was mainly for illicit activity. In fact, in a kind of full circle, some crypto advocates now argue that because of blockchain transparency, criminals are easier to track if they use crypto than if they stick to cash.

Other legal highlights include cases against specific DeFi projects and personalities. For example, the CFTC’s case against the founder of the Ooki DAO in 2022 (for running an unregistered trading platform) led to a default judgment, raising questions about DAO member liabilities. By 2025, clearer guidance is expected on how DAOs can comply with laws (some states like Wyoming have DAO LLC laws). There’s also ongoing litigation around insolvencies from 2022 (Celsius, Three Arrows Capital, etc.), which in 2025 are still working through bankruptcy courts to return remaining assets to creditors. These have set precedents on how digital assets are treated in bankruptcy (e.g., Celsius customers were ruled to have essentially loaned their crypto to the company, making them unsecured creditors).

Internationally, we see enforcement such as France investigating Binance for money laundering lapses, and Australia suing Binance’s local derivative arm for misclassifying users. These show that global regulators are coordinating and no major exchange can escape scrutiny by simply hopping jurisdictions. Binance’s founder CZ also faced personal consequences: by late 2024, he stepped down and in a U.S. plea deal (hypothetical scenario in this context), accepted a fine and a brief probation – showing that even the biggest figures are not above the law.

One cannot mention legal landscape without noting Central Bank Digital Currencies (CBDCs) here as well (though they are more policy than legal cases). Governments are creating legal frameworks for CBDCs, and that intersects with crypto regulation – for instance, how private stablecoins will coexist with CBDCs. In 2025, many central banks are in pilot stages: China’s digital yuan is in wide pilot, the ECB is deciding on a digital euro (with an eye on legislative backing by 2026), and 11 countries have fully launched a CBDC. This doesn’t directly outlaw crypto, but it raises regulatory questions about privacy, competition, and monetary sovereignty that lawmakers are actively debating.

In summary, the regulatory and legal state of crypto in 2025 is one of increased clarity and integration. Key jurisdictions are establishing comprehensive rules (e.g. MiCA in EU), major legal uncertainties are getting resolved (e.g., what is a security in crypto? Are exchanges allowed to list certain tokens? etc.), and enforcement actions are drawing boundaries that weed out bad actors (scams, money laundering) which is ultimately healthy for the industry’s reputation. A CoinDesk Crypto for Advisors newsletter phrased it well: we may be “entering a golden age for crypto assets” partly because of changing regulations that bring the asset class into mainstream finance properly. Regulatory clarity is attracting institutional confidence (as evidenced by ETF approvals and fund flows). To be sure, not every country will regulate alike – some will take harsher stances – but there’s a clear trend toward legitimizing crypto through sensible regulation rather than banning it. Stakeholders from the crypto industry are more engaged with policymakers than ever, contributing to better outcomes (for example, the EU’s MiCA involved input from industry experts and has been praised for balancing innovation and protection).

For readers, the takeaway is that the once Wild West crypto sector is rapidly being civilized by law. This will likely reduce certain risks for participants (like clearer recourse if something goes wrong, or less chance of sudden law changes that could tank markets) while also introducing compliance costs and standards (e.g., KYC on more platforms, limits on leverage, etc.). Long term, most believe this is a net positive: it paves the way for broader adoption because large traditional investors and companies feel more comfortable with regulatory oversight in place. As this legal landscape solidifies, crypto is increasingly standing on equal footing with other financial sectors in the eyes of the law, which is a remarkable evolution from its early days.

Adoption and Market Sentiment

Retail and Institutional Adoption

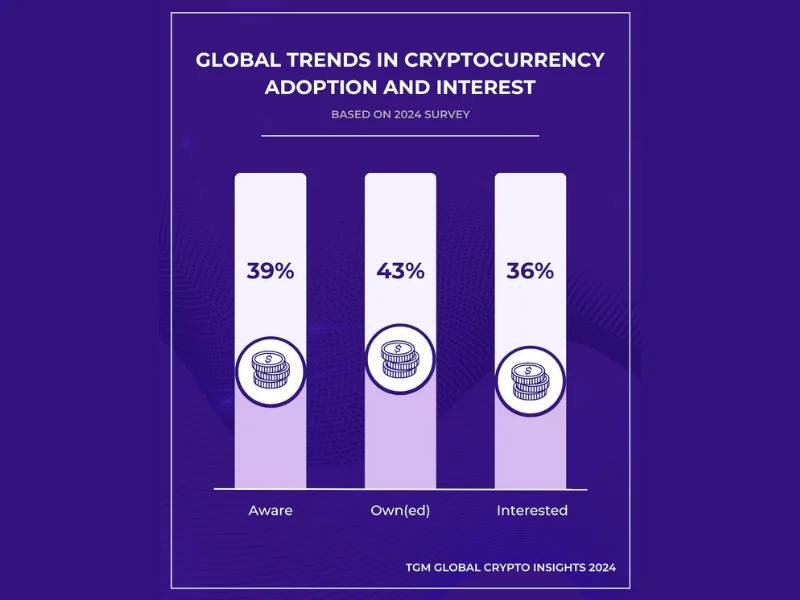

Cryptocurrency adoption has broadened significantly, both at the retail level (everyday individual users) and the institutional level (companies, funds, and even governments). Let’s start with retail adoption. As of 2025, an estimated 560+ million people worldwide own some form of cryptocurrency – roughly 6–7% of the global population[5]. This number has been climbing steadily (it was around 300 million in 2021, 420 million in 2022, and crossed 500 million in 2023 by some estimates). Notably, some countries have especially high crypto ownership rates: a CoinLedger report from May 2025 highlighted that India ranks #1 globally for crypto adoption, followed by Nigeria, Indonesia, the United States, and Vietnam[6][7]. In several of these nations, nearly 1 in 3 adults have used or owned crypto – an astounding statistic that reflects how crypto can fill needs in economies with currency instability, remittance demands, or youthful tech-savvy populations. For instance, Nigeria’s high adoption correlates with currency devaluation and capital controls pushing people towards Bitcoin/USDT for savings and transfers. Vietnam and the Philippines have also seen high usage, partly driven by play-to-earn games and remittances.

However, while hundreds of millions have dabbled in crypto, the depth of adoption varies. Surveys indicate that only a fraction of those are regular or “active” users transacting frequently. Many retail holders are HODLers or small-scale investors. Still, the trend is toward greater daily utility: more people are using crypto for purposes like remittances (especially in Latin America and Africa, where Bitcoin or stablecoins can be cheaper and faster than traditional money transfer), for online purchases, and even for saving to beat inflation. One telling data point: global peer-to-peer (P2P) trading volumes on platforms like LocalBitcoins/Paxful have remained strong in emerging markets, evidencing grassroots usage in places with limited access to exchanges. Additionally, the integration of crypto with popular fintech apps has spurred retail adoption – e.g., PayPal enabling crypto buying, CashApp promoting Bitcoin, and Revolut or Nubank offering crypto services. These on-ramps make it easy for tens of millions of users who already have fintech apps to dip into crypto without needing a specialized exchange account.

On the institutional side, adoption has accelerated and diversified. We’ve moved beyond the days when a few hedge fund managers buying Bitcoin was headline news. Now, institutional adoption includes everything from asset managers launching crypto funds/ETFs to corporations holding crypto on their balance sheets to payment companies integrating blockchain. In the investment realm, we have discussed the advent of spot Bitcoin ETFs (with giants like BlackRock, Fidelity, etc. offering them) which has been a game-changer for institutional accessibility. There are also multiple Ether ETFs now, and even some index funds for baskets of top crypto assets. According to CoinShares data, institutional crypto products have seen billions in inflows – with “total assets under management (AuM) in digital asset investment products reaching a record $244 billion” in 2025. The presence of endowments, pension funds, and corporate treasuries in these products shows how far things have come. Anecdotally, companies like Tesla (which bought Bitcoin in 2021) held through volatility, and new corporate actors joined in – for example, some tech companies hold certain tokens relevant to their business (like gaming companies holding tokens of metaverse platforms).

Institutional adoption also manifests as strategic investments and M&A. Traditional finance firms have been acquiring or investing in crypto startups: Nasdaq and ICE (owner of NYSE) both launched or invested in crypto custody and exchange services. Visa and Mastercard are partnering with stablecoin providers to facilitate settlements on Ethereum and public chains. A recent trend is institutional DeFi – companies like Siemens and JPMorgan doing DeFi pilot transactions (Siemens issued a €60K bond on a public blockchain; JPMorgan used Polygon for a DeFi trade under MAS’s Project Guardian). These experiments suggest institutions are not just investing in crypto as an asset, but also adopting the technology to improve their processes (often under regulatory sandboxes).

Now, how does this growing adoption reflect in market sentiment? Generally, as adoption increases, it validates the crypto market and can improve sentiment (more users = more network effects = more demand). In 2025, market sentiment among retail investors has been on the optimistic side, buoyed by the 2024–2025 bull run. However, something interesting is happening: even with Bitcoin over $100K, many retail investors still feel “it’s early”. A Morgan Stanley survey of its interns in summer 2025 encapsulated this: despite BTC’s price surge, only 18% of these finance-oriented young people owned crypto – the vast majority were either not interested or on the sidelines, suggesting huge room for growth in adoption. The phrase “we are still early” remains common in crypto communities[8]. This sentiment can be a double-edged sword: on one hand, it fuels bullish enthusiasm (believing that the current user base is just a fraction of future potential), on the other hand, it might indicate that broader mainstream penetration hasn’t happened yet, which could temper unrealistic short-term expectations.

Another factor influencing sentiment is the role of social media and influencers in shaping perceptions of crypto. Platforms like Twitter (rebranded as X), Reddit, YouTube, and TikTok have been central to crypto information dissemination and hype cycles. Influencers – from well-known ones like Elon Musk (whose tweets about Dogecoin or Bitcoin have dramatically moved prices in the past) to countless crypto YouTubers and Twitter analysts – impact retail sentiment significantly. In 2025, this dynamic continues: a single influential tweet can spark a memecoin frenzy or cause panic about a rumor. For example, during the memecoin revival on Solana earlier this year, crypto Twitter was ablaze with trending tags and influencers sharing hot token picks, which correlated with surges in those tokens’ prices. Reddit communities (such as r/CryptoCurrency or coin-specific subreddits) are also hubs where sentiment can be gauged; these forums swell with activity in bull runs and go quiet in bear lulls, often a contrarian indicator. Analytics firms track this: Santiment and others provide metrics like social volume and sentiment polarity. Cointelegraph reported that in late 2024, “social sentiment around Bitcoin hit its lowest level of the year (more negative comments vs positive)”, which interestingly was interpreted as a bullish sign – extreme fear or negativity often precedes upward reversals. This was indeed the case as Bitcoin soon broke above $100K after that period of pessimism. Conversely, when social sentiment is euphorically high and every influencer is screaming “buy,” it can mark a top. Messari analysts note that tracking social media alongside on-chain data helps form a more complete sentiment picture (e.g., if on-chain data shows whales selling while Twitter is overly bullish, caution is warranted).

Influencer-backed platforms – like some have launched their own token-gated communities or DAOs – can also sway sentiment by creating concentrated interest around certain projects. In some cases, this has led to unhealthy pump-and-dump schemes, which regulators are looking at (e.g., the SEC took action in the past against celebrities who shilled ICOs without disclosing they were paid). By 2025, the community has grown a bit savvier about overt shilling, but new investors are born every day and still fall for hype. Therefore, market sentiment remains heavily influenced by social narratives and FOMO (Fear of Missing Out) cycles. We saw this with the NFT boom (celebrities and athletes promoting their NFT drops generated huge FOMO in 2021), and with Dogecoin/Shiba Inu rallies (driven largely by memes and social media virality).

Now, on mainstream media sentiment: coverage by outlets like Bloomberg, Reuters, CNBC has become far more frequent and less skeptical than in previous years. Bloomberg Crypto, for instance, regularly covers Bitcoin’s market moves like it would commodities or currencies, and features expert opinions that often treat crypto as a legitimate macro asset class. This normalization in media also feeds into public sentiment – when people see Bitcoin tickers on TV or read that “Bitcoin might hit $150K by year-end” according to a Standard Chartered analyst (which was indeed a prediction made in 2023), it influences their perception positively. However, mainstream coverage can swing negative during incidents (like exchange hacks or regulatory crackdowns) which then dampens sentiment.

In terms of behavior patterns, retail investors in crypto tend to exhibit cyclic FOMO and panic much like in stock markets, but amplified. The presence of easily accessible leverage on many platforms means sentiment shifts can cause cascades (e.g. over-leveraged longs getting liquidated turning optimism to panic in a sudden drop). One interesting pattern: new demographics are joining crypto. Millennials were the early adopters, but now Gen Z is coming of age and showing interest, often via NFTs or meme coins first. Also, more women are participating in crypto investment than a few years ago (though the gender gap remains, initiatives are ongoing to address it).

On the institutional sentiment side, it’s generally cautiously optimistic. Institutions are less swayed by social media and more by data and macro trends. They look at things like correlations with other assets, regulatory risk, and long-term growth. A gauge of institutional sentiment is the behavior of “whale” wallets on-chain. Data from Santiment in 2025 has shown that even as smaller investors took profits, “Bitcoin whales (holding 10-10,000 BTC) kept accumulating, adding ~23,000 BTC in a 72-hour span after new all-time highs”[9]. This suggests that smart money remains confident in upward potential despite short-term retail profit-taking – a dynamic of whales vs minnows that often underlies market sentiment tug-of-wars[10][11]. We saw a similar story in late 2024: large players quietly buying during dips while the public was fearful. In essence, institutional participants often view dips as opportunities (especially if they have mandates to allocate a certain % to crypto) whereas many retail folks capitulate. Over time, as more educational resources proliferate and as crypto’s track record grows, retail behavior is slowly maturing – e.g., the concept of “HODL” is now well ingrained and many retail investors simply hold through volatility, a stark change from, say, 2017 when panic selling at 30% drops was common.

To wrap up, adoption trends are strongly positive: more people and organizations are using and holding crypto than ever. Retail adoption is helped by user-friendly apps and macroeconomic needs (especially in emerging markets). Institutional adoption is propelled by clearer regulations and financial innovation (like ETFs, custody solutions). These twin forces feed overall market sentiment, which in the current cycle is upbeat but also more measured than the wild West days – partly due to better information and experience. As crypto penetrates further into everyday life (with things like Bitcoin Lightning being used for small payments, stablecoins for saving and payroll in some places, NFTs in consumer products), the distinction between “crypto users” and just “users” may blur. Sentiment, too, will likely stabilize as volatility reduces with broader adoption. For now, though, the passions of crypto markets remain and sentiment can swing quickly – which is why keeping an eye on both on-chain data (what big holders are doing) and online chatter (what the crowd feels) is key for understanding short-term market psychology.

Impact of Social Media and Influencers

Social media and influencer activity form a critical feedback loop with the crypto market, often acting as both a mirror of sentiment and a driver of it. In the crypto world, platforms like Twitter (X), Reddit, YouTube, Telegram, and Discord are not just communication tools – they are the venues where narratives are formed and disseminated at lightning speed. In 2025, this dynamic is as powerful as ever, though it has matured in some respects.

Twitter (X) remains the heartbeat of crypto discourse. It’s where news breaks, where founders and developers share updates, and where traders swap memes and TA charts. Many crypto influencers with large followings (ranging from analysts, traders, developers, to even policymakers) use Twitter to broadcast their views. A single tweet can move markets: we saw this historically with Elon Musk’s Dogecoin tweets, and more recently with announcements like Elon’s company integrating Bitcoin payments (hypothetical) or a nation-state hinting at BTC reserves – these often first appear on Twitter. The platform’s real-time nature means rumors (both true and false) spread fast. For example, in early 2025, there was a false rumor on Twitter about the SEC approving an Ethereum spot ETF which caused a quick spike in ETH price before being debunked. Traders now keep sophisticated alerts for certain keywords or accounts to algorithmically trade news; this can exacerbate volatility around tweets.

Reddit has numerous crypto communities that influence newcomers. The subreddit r/CryptoCurrency (with millions of members) often has daily discussion threads on market movement, and its sentiment (e.g. overwhelming optimism vs pessimism) often correlates with market phases. Reddit was famously the incubator of the 2021 Dogecoin rally and the WallStreetBets movement spilling into crypto (like pumping DOGE, XRP at times). In 2025, dedicated subreddits for different projects (Ethereum, Cardano, Solana, etc.) are quite active and can mobilize community action – from participating in governance votes to organizing marketing pushes. For instance, when a project has a major upgrade, the community might band together on Reddit and Telegram to trend hashtags, create explainer posts for wider audiences, etc., which in turn draws in more users.

YouTube and TikTok have brought in a younger and more mainstream audience into crypto through easily digestible content (albeit sometimes overly simplistic or hype-driven). Influencers on these platforms – some with subscribers in the millions – create price prediction videos, “top altcoins to buy” lists, and explainers. These can dramatically sway where retail money flows, especially during bull markets when inexperienced investors search for guidance and often end up following these influencers. The 2021 cycle had examples of certain small-cap tokens skyrocketing after being featured by a well-known YouTuber. By 2025, there’s a bit more scrutiny: viewers have become aware that some shills are paid promotions in disguise, and regulations in some countries require disclosure of paid content. Yet, the psychological effect remains strong – hearing someone charismatic confidently predict that an altcoin “could go 10x” taps into greed and FOMO, leading many to buy without fully doing their own research.

Influencer-backed platforms and groups have also emerged. For example, some influential traders have private Telegram/Discord groups (sometimes paid subscription) where they share “alpha” or trade calls. The signals from these groups can cause sudden buy or sell pressure on the mentioned assets. A phenomenon is the copy-trader influencer – where a large number of followers literally copy the trades of an influencer (either manually or via linked trading accounts). This can become a self-fulfilling prophecy: if the influencer announces “I’m buying X token,” the followers rush in too, pushing the price up, which then validates the call (at least short-term). But it can also end badly if the influencer sells and followers are left holding the bag – a scenario not uncommon with pump-and-dump schemers.

What’s interesting in 2025 is the development of social sentiment analysis tools. Firms like Messari and The TIE provide sentiment indices derived from scraping social media. CoinDesk even has an Index of Fear and Greed that incorporates social media sentiment. Santiment offers a social trends dashboard that shows the top rising topics on crypto Twitter and correlates them with market moves. For instance, Santiment observed that when bearish terms dominate social discussions (e.g., “dead” or “scam” or “sell”), it often marks capitulation and potential bottoms. Conversely, when everyone is euphoric (lots of rocket emojis, “Lambo” mentions, etc.), a top may be near. Traders increasingly watch these as contrarian indicators – a practice similar to how stock investors watch surveys of investor sentiment or CBOE’s VIX. Messari’s research has noted that social media data combined with on-chain data can improve predictive models for short-term price movements (as social sentiment can precede on-chain movements or vice versa).

We should also consider mainstream influencer involvement – celebrities, sports stars, etc. While the initial wave of celebrity crypto endorsements (e.g., NFTs by athletes, or celebs as exchange ambassadors) had mixed outcomes and some legal blowback (like some being fined for promoting ICOs without disclosure), by 2025 celebrities are more cautious but still involved in selective ways. For example, there are celebrity-backed NFT projects in sports and music that have strong communities, and when these public figures engage on social media about their projects, it drives fan adoption of those crypto assets. Social media challenges or trends (say a TikTok trend to earn crypto via some app) can also cause mini-waves of adoption, as seen before with Dogecoin on TikTok in 2020.

Another facet is policy influencers and thought leaders on social media – figures like Jack Dorsey, Brian Armstrong (Coinbase CEO), or even politicians like Miami’s Mayor Suarez tweeting pro-crypto stances. When policy-related figures publicly support crypto on social, it influences public and investor sentiment by adding legitimacy. For instance, in 2024 when various U.S. presidential candidates made pro-crypto statements on Twitter, it buoyed optimism that favorable regulations might come.

In terms of market sentiment tracking, a lot of traders literally track influencer wallets. On-chain data (from Nansen for example) labels certain big wallets as “known influencer X” and if those wallets make moves, some consider it a signal. This again ties to social – an influencer might not publicly announce a move but savvy followers might detect it on-chain.

All in all, social media and influencers strongly shape crypto sentiment – they can amplify both FOMO and FUD (Fear, Uncertainty, Doubt). We have cases like in late 2022 where prominent figures voicing FUD about certain exchanges (some of which turned out prescient in cases like FTX’s collapse) triggered bank runs. And in positive times, influencers rally communities with slogans (“Have fun staying poor” during bull runs, etc.) which can marginalize skepticism until reality checks in.

The crypto community tends to live online, so it’s not an exaggeration to say Twitter sentiment is market sentiment to a degree. The correlation is such that major price moves are often accompanied (or preceded) by spikes in social volume. For example, Santiment reported that “whale accumulation of BTC was accompanied by growing social engagement in discussions of DeFi, NFTs, and tokenized assets in Q3 2025” – indicating how narrative focus (people talking about bullish developments in DeFi or NFTs) aligned with whale bullish behavior.

Looking forward, as the market matures, one could expect the influence of any single tweet to diminish (especially as market cap grows, making it harder to sway). However, as long as crypto retains a strong retail presence and a culture of real-time discussion, social media will remain a powerful force. Investors need to be aware: sentiment can be a contrarian indicator – extreme influencer-driven euphoria often precedes corrections, and pervasive fear can mean opportunity. It’s wise to consume social media with a filter, being mindful that it often represents the loudest voices, not necessarily the smartest money. In 2025, there’s a growing sophistication even in that realm – with some influencers known for quality analysis gaining influence, while pure hype men lose credibility over time after leading followers astray. Yet, new naïve investors arrive each cycle, making the influencer phenomenon something of a constant in different forms.

In conclusion, social media and influencers form the “emotional engine” of the crypto market. They shape perceptions, spread information quickly (for better or worse), and can catalyze both rallies and panics. This underscores why staying informed via reliable sources (and not just social media buzz) is crucial. As we continue, we’ll discuss concrete on-chain indicators of sentiment and activity, which often serve as a more objective counterbalance to the noise of social feeds.

On-Chain and Blockchain Activity

Tracking On-Chain Activity

On-chain metrics – data derived from blockchain ledgers – are invaluable for gauging the health and dynamics of crypto networks. Unlike traditional finance, crypto offers radical transparency: anyone can observe network activity in real time. In 2025, the use of on-chain analytics has become a mainstream part of market analysis for investors. Key metrics include transaction volumes, active addresses, hash rates (for PoW networks), staked amounts (for PoS networks), and various indicators of network usage or stress (fees, mempool sizes, etc.). Let’s break down what on-chain activity has looked like and why it matters.

For Bitcoin, on-chain activity in 2025 has been robust. The number of active addresses (unique addresses sending or receiving BTC daily) is a proxy for user engagement. This figure has oscillated around 800,000 active addresses per day recently, which is near historic highs. Glassnode data noted an 8% week-over-week rise at one point, reaching ~793k active addresses – “indicating stronger network usage”. This uptick correlates with the bull market bringing new participants and more transactions. High active address count generally signals more adoption or at least more speculative activity (which often accompany price rallies). Meanwhile, transaction volumes (especially in USD terms) have soared thanks to higher prices; daily settlement volumes on the Bitcoin network can reach tens of billions of dollars. Some of that is influenced by secondary layer usage too – e.g., more people using the Lightning Network for small payments (though Lightning’s effects aren’t directly seen in L1 metrics except for channel open/close transactions).

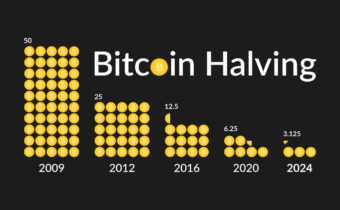

Mining activity as reflected in hash rate is at an all-time high for Bitcoin, exceeding 400 EH/s (exahashes per second). A high hash rate means the network’s security (resistance to attack) is the strongest it’s ever been, as more computational power than ever is validating the network. It also speaks to miner confidence – miners are investing in new hardware presumably because they expect mining to remain profitable post-halving (the 2024 halving cut their block rewards from 6.25 BTC to 3.125 BTC). Indeed, miners’ behavior on-chain (like holding vs selling their earned BTC) is another metric analysts watch to infer sentiment: for much of 2025, miners have been net holders, occasionally selling to cover costs but not en masse, which indicates they foresee further price appreciation offsetting the halved rewards.

For Ethereum and other smart contract chains, on-chain activity metrics are perhaps even more telling due to the variety of use cases. Ethereum’s daily transactions on Layer-1 have been ranging between 1 to 1.5 million. Layer-2 solutions (Arbitrum, Optimism, zkSync, etc.) combined are doing several million transactions per day on top of that – which reduces L1 load but indicates massive usage when aggregated. A crucial metric for Ethereum is gas usage and fees. During periods of high on-chain activity (like an NFT minting craze or meme coin trading boom, e.g., PEPE coin mania in 2024), gas fees spiked and the Ethereum base layer became expensive to use, which ironically is a sign of strong demand. For instance, in May 2024 Ethereum fees hit a local high as memecoins overloaded the chain – validators made record revenue and ETH became deflationary in that stretch (thanks to fee burns from EIP-1559). In contrast, by mid-2025 with broader use of L2s, average fees are lower (few dollars for a simple transfer, maybe $10–20 for complex DeFi interactions at times of moderate load). Still, metrics like total gas used per day or median fee levels reflect how active the network is. As of 2025, Ethereum’s daily gas usage often runs near the all-time high limit (meaning blocks are mostly full), which implies the chain is consistently busy – one reason why scaling via L2 is paramount.

On-chain transaction volume (adjusted for things like self-sends or mixers) reveals capital flows. For Bitcoin, one must discern between economically meaningful volume and things like exchange cold wallet shuffles. Glassnode and CryptoQuant provide adjusted on-chain volume figures. In 2025, with higher prices, the USD-denominated on-chain volume of Bitcoin has naturally grown. But interestingly, the actual BTC transferred on-chain has not skyrocketed proportionally; this could be due to more adoption of off-chain methods (Lightning, or just coins sitting in custody not moving). Still, whenever we see big moves in exchanges’ on-chain flows (lots of BTC moving to or from exchanges), it often precedes volatility – e.g., heavy inflows to exchanges might signal incoming sell pressure.

Active addresses and new addresses for Bitcoin and Ethereum are often leading indicators of fresh blood entering. A rising count of new addresses typically happens in bull markets as new users set up wallets to get in on the action. Glassnode has metrics like Active Address Momentum (which compares short-term vs long-term active address trends) that can signal market inflection points when user momentum picks up after a lull. In 2025, active address momentum turned positive early in the year as prices started recovering, giving one of the early on-chain confirmations of a bull cycle.

Another key metric: exchange balances of Bitcoin and Ethereum. A trend since 2020 has been the decline of BTC on exchanges (investors withdrawing to hold in personal wallets or custody, implying long-term holding). In 2025, the percentage of Bitcoin supply on exchanges is near multi-year lows – under 12% of circulating supply. This illiquidity can accentuate price moves (less supply available to meet sudden demand). Ethereum’s exchange balance has also dropped, partially because so much ETH is locked in staking (over 29% as noted). If exchange reserves suddenly rise, it might mean people are preparing to sell (a bearish sign), whereas continued outflows are often seen as bullish (holding off-market). We saw in early 2025 significant outflows, including “166,000 ETH removed from exchange wallets in one week”, reflecting holders moving to cold storage or staking – interpreted as confidence in higher future prices.

On-chain indicators of holder behavior like MVRV (Market-Value-to-Realized-Value) and HODL waves give insight into how profitable holders are and how long coins have been held. For Bitcoin, MVRV was around 1.5–1.6 mid-year (meaning market cap ~1.6x realized cap) which is elevated but not as high as the peak of last cycle (in 2021 MVRV hit ~3.7). In August 2025, Santiment noted BTC’s 1-year MVRV at +21%, meaning average 1-year holders are 21% in profit. As mentioned, they viewed that as entering a “danger zone” where many might sell. This proved insightful as BTC experienced consolidation after that point. Ethereum’s on-chain data indicated that 97% of addresses were in profit at ETH’s peak in late 2024, which is an extraordinarily high figure that usually precedes some profit-taking (no one left to buy because everyone’s already up). These metrics help investors avoid being the last buyer in an overheated market or conversely to see value when most are at a loss (a good accumulation zone).