1) Introduction

Purpose of this article. You asked for a clear, up-to-the-minute, analytical read that covers what matters now in crypto and, specifically, weighs the market impact of Bitcoin’s halving versus Ethereum’s Merge. Below you’ll find a single, comprehensive brief that brings together current prices and flows, the latest tech upgrades, regulation, adoption, and expert takes—then delivers a verdict on which event has been (and is likely to remain) more market-moving.

Why staying updated is essential. Crypto moves at the speed of software and the scale of macro. Since early 2024 the industry has absorbed spot BTC and ETH ETFs in the U.S., a fresh Bitcoin halving (Apr 2024), Ethereum’s scaling upgrades post-Merge, and a changing regulatory stance in the U.S. and Europe—all while liquidity and correlations with TradFi keep shifting. These dynamics have direct implications for portfolio construction, risk, and timing for retail, crypto beginners, and institutions alike.

Primary sources used. This analysis leans on real-time and institutional-grade references: CoinDesk for breaking market/tech updates; Glassnode for on-chain fundamentals; Bloomberg Crypto/News for macro and corporate coverage; market aggregates from CoinGecko; fund-flow intelligence from CoinShares; liquidity and microstructure from Kaiko; plus regulatory coverage from Reuters, Financial Times, and DL News. Where applicable, we also reference DeFiLlama, Dune, Nansen, Santiment, BIS, and IMF for specialized views.

What’s inside. We’ll cover global market conditions; institutional and macro drivers; tech progress across L1s/L2s; regulation; adoption; on-chain signals; and end with a decision framework comparing Halving vs. Merge—including where each is likely to matter most going forward.

2) Global Market Trends

Current market performance & capitalization

As of today, the global crypto market cap is hovering in the $3.9–4.0T range with Bitcoin dominance ~56–57% and Ethereum ~14%. Live trackers show daily swings of ~±1–3% with seven-day moves shaped by policy headlines and liquidity rotations.

On a weekly basis, BTC and ETH have been consolidating just below recent highs after setting records this summer; headlines around Jackson Hole and a weekend “flash crash” underscored how macro and large treasury/ETF flows can whipsaw near-term price action.

Takeaways for all audiences.

- Beginners: total market cap and dominance are your North Stars for orientation.

- Retail: watch 24h vs. 7d spreads to distinguish noise from trend.

- Institutions: dominance + realized volatility + order-book depth (see Kaiko) frame execution and hedging.

Institutional involvement & economic influence

Institutional flows continue to set the tone. CoinShares’ latest weekly shows record-scale rotations: in mid-August, digital asset ETPs took in $3.75B with ETH leading; by Aug 25, macro jitters flipped to $1.43B outflows (largest since March), $1B of which were from BTC products, while ETH saw comparatively milder redemptions. These flows illustrate a market increasingly sensitive to policy and rates but with deep institutional participation.

On the macro side, BTC printed new all-time highs this summer amid corporate interest and a softer USD at times; market structure research also notes correlation breaks between crypto and equities as narratives (ETFs, policy) dominated.

Sentiment snapshot: In August, Bitcoin hit fresh highs before sharp retracements tied to policy signaling and profit-taking—classic “post-ATH digestion” behavior. Expect liquidity pockets and options-market hedging to shape near-term moves.

3) Technological Developments & Innovations

Blockchain advancements

Ethereum: The Merge (Sept 15, 2022) moved Ethereum to proof-of-stake, slashing energy use by ~99.95%, reducing issuance, and paving the way for scaling upgrades. The Dencun upgrade (Mar 2024) added EIP-4844 “blobs”, cutting Layer-2 fees and boosting L2 throughput—a key unlock for dApp UX.

Solana: After a notable Feb 2024 outage (~5 hours) that prompted criticism, the ecosystem has emphasized client diversity and performance. Firedancer, a high-performance validator client from Jump Crypto, is slated for rollout across 2025, with testing demonstrating potential for ~1M+ TPS under synthetic conditions—important for resiliency and throughput if it lands broadly on mainnet by late 2025.

Security enhancements in crypto

Security remains a dual track: protocol-level hardening (clients, ZKPs, upgrades) and ecosystem monitoring (liquidity, on-chain flows). Despite improvements, mid-2025 YTD hacks exceeded 2024’s total by July, spotlighting persistent DeFi and centralized service risks. Researchers tracked >$2.1B in service thefts YTD, dominated by a single mega-incident, reminding investors to prioritize audits, bug bounties, and custody hygiene. DeFiLlama’s dedicated hacks trackers complement this picture.

Smart contracts and dApps

DeFi and dApp ecosystems continue to expand, with L2s absorbing more execution thanks to blob-based fee cuts. Messari and Dune dashboards show growth in active addresses and transactions across rollups; developers are shipping faster on L2 with modular data availability and standardized tooling. TVL across chains (DeFiLlama) has rebounded with market cap—though composition is increasingly L2 & cross-chain rather than only L1.

4) Regulatory & Legal Landscape

Current regulatory updates

- United States. The SEC approved spot ETH ETFs in May 2024; trading began July 23, 2024, reinforcing Ethereum’s mainstream investability. In 2025, new leadership and “Project Crypto” signaled a more rules-based approach to digital assets, with market-structure bills advancing in Congress.

- European Union. MiCA entered into force with stablecoin rules phased in 2024 and full scope through 2024–25. The ECB has even pushed for adjustments to MiCA as U.S. policy warms, and ESMA urged tight national compliance. Expect euro-stablecoin share to grow under MiCA.

- United Kingdom. The FCA’s stance on promotions and a slower stablecoin framework have drawn criticism, with commentators warning the UK risks falling behind peers.

Legal cases & precedents

- Coinbase v. SEC. A U.S. federal judge dismissed the SEC’s case against Coinbase, an important precedent for how courts interpret token classification and exchange conduct. (Appeals and parallel actions may still evolve.)

- Binance (context). Enforcement and settlements since late 2023 reshaped CEX risk management globally; regulators continue pressing AML/market integrity in multiple jurisdictions. (Broader impact covered across Reuters/FT ongoing coverage.)

5) Adoption & Market Sentiment

Retail and institutional adoption

ETFs have normalized crypto exposure for advisors, pensions, and 401(k) plans, while wallets and L2 dApps lowered onboarding frictions for retail. CoinShares flows show ETH gaining share in recent weeks—even versus BTC—while CoinGecko research highlights an expanding user base in Q1-2025 despite choppy prices.

The social-media flywheel

Social momentum remains powerful. In July, Bitcoin’s social dominance spiked to historic levels as prices broke to new highs—often a contrarian near-term signal, per Santiment. Their weekly notes frequently highlight funding-rate and social-sentiment extremes as reversal zones.

6) On-Chain & Liquidity

Tracking on-chain activity

For Bitcoin, Glassnode’s H1-2025 work shows how ETF flows, fee pressure, and long-term holder behavior shape supply dynamics. Post-halving, fee/reward composition fluctuated sharply—briefly pushing fees to dominate miner income around the event window—before normalizing. Such spikes often accompany ATH periods and run-ins with new protocols (e.g., Ordinals/Runes).

Liquidity & market microstructure

Kaiko reports detail market depth, spreads, and correlations. In 2025, BTC has increasingly decoupled from equities at times, driven by idiosyncratic ETF/treasury flows and macro policy. Their “10 charts” series and weekly insights track depth, slippage, and options skews, which institutions use for sizing and hedges.

7) Emerging Trends & Future Outlook

NFTs: beyond JPEGs

After a deep bear, NFT activity is stabilizing and diversifying (gaming, ticketing, IP licensing). DappRadar’s Q2-2025 report maps shifting volumes and chains, while Coin Center continues policy analysis on digital ownership and speech—relevant as enterprise/IP use cases mature.

DeFi’s continuing evolution

TVL has recovered in aggregate (with leadership oscillating across L2s and high-throughput L1s), and the design frontier is risk-managed lending, perps, and RWAs. Use DeFiLlama to track protocol TVL, chains, and sectors in real time.

Stablecoins & CBDCs

Stablecoins are now integral to crypto (and increasingly to global payments rails). Regulators are getting specific: MiCA in the EU, U.S. bills advancing, and BIS/IMF urging robust guardrails. The BIS 2024/25 survey shows ~90%+ of central banks actively exploring CBDCs; IMF notes lay out design trade-offs, cyber resilience, and adoption strategies.

8) Investor Insights & Sentiment Analysis

Behavioral shifts. Nansen and Santiment show whale activity clustering around narrative peaks (ETFs, policy, halving run-ups). Sentiment extremes often precede reversals, and development-activity trackers (e.g., Santiment) can surface under-the-radar momentum in infra tokens.

Risk management. Options skew (Kaiko), basis, and funding rates have become mainstream tools—even for long-only allocators—to manage tail risk during macro weeks and ETF windows. Keeping a simple hedge playbook (long downside via puts into event risk, long gamma around CPI/FOMC weeks, etc.) can materially improve risk-adjusted returns.

9) Case Studies & Market Examples

Bitcoin halving events & price impact

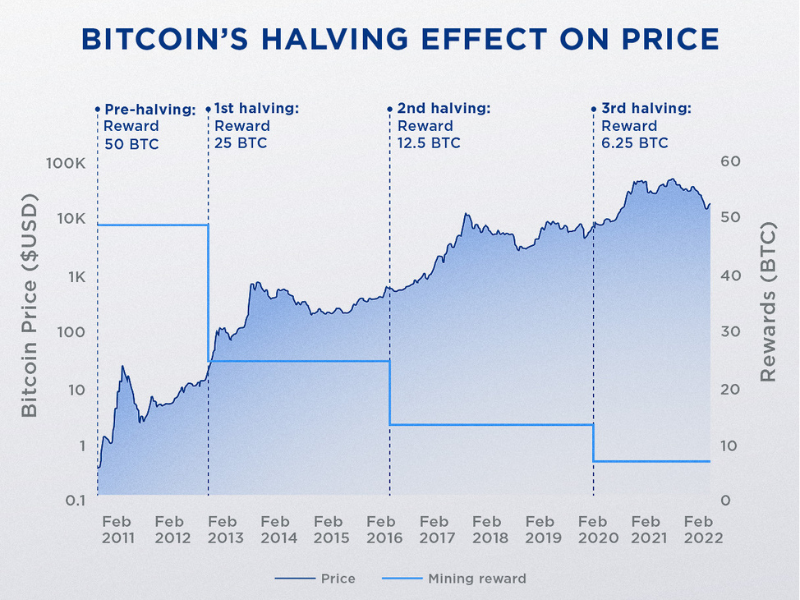

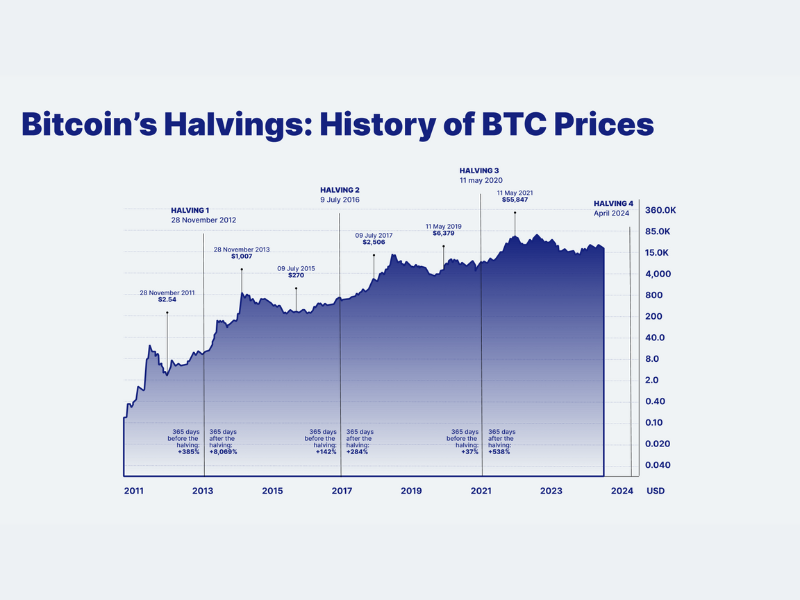

Bitcoin’s fourth halving hit block 840,000 on Apr 19–20, 2024, cutting issuance from 6.25 → 3.125 BTC per block. The halving block carried record fees and briefly saw fees comprise >70% of miner revenue as Runes/Ordinals congested blockspace. Historically, halving cycles compress supply and tighten miner economics; price impact tends to manifest with a lag as flows and narratives adjust.

Post-halving miner economics. Glassnode’s “Week On-Chain” work shows a re-balancing toward fee-sensitive miner revenue and how network activity at ATHs compresses the Fee-Revenue Multiple, a hallmark of bull phases.

Ethereum 2.0 transition (Merge → Dencun)

The Merge fundamentally changed ETH’s energy profile (~99.95% less energy) and issuance schedule (net issuance can be near-flat/deflationary during high activity, thanks to EIP-1559 burns). With Dencun/EIP-4844, L2 fees dropped materially, catalyzing dApp growth and improving user experience.

A crucial market datapoint: by Aug 2025, U.S. ETH ETFs’ August inflows were reported to exceed ETH issued since the Merge—illustrating how tradFi pipes can now absorb net issuance in weeks, not years.

10) Impact of Global Events on Crypto

Economic factors. BTC’s surges above $110K–$120K in 2025 coincided with policy optimism, ETF momentum, and periodic USD weakness; conversely, hawkish surprises or rate-path uncertainty drove sharp pullbacks. The correlation to equities ebbs and flows, and 2025 has seen idiosyncratic BTC behavior lead the complex.

Geopolitics & policy. Headlines around tariffs, elections, and regulatory pushes have repeatedly synchronized with large inflow/outflow weeks in CoinShares data—and with sentiment spikes across social channels.

11) Key Insights from Industry Experts

- Bloomberg Crypto and others tracked BTC’s new highs and the corporate/treasury interest that’s growing alongside ETFs—an institutionalization trend that tightens supply on exchanges.

- CoinDesk’s coverage around the halving and Dencun has emphasized how protocol design (supply schedule, blob transactions) shapes real demand and fee markets.

- CoinShares’ research repeatedly shows how flows (in and out) can dwarf on-chain issuance on short time frames—critical when evaluating ETF-era dynamics.

12) Halving vs. Merge — Which had the bigger impact?

Short answer:

- Market capitalization & near-term price cycles: Bitcoin’s halving still wins. Its hard-coded supply shock, reinforced by spot BTC ETFs and corporate treasuries, has coincided with the largest absolute wealth creation, stronger all-time highs, and the heaviest ETP flow swings in 2025.

- Technology, ESG profile, and platform economics: Ethereum’s Merge has been the bigger structural shift—eliminating ~99.95% of energy use, lowering issuance, and enabling cost-cutting L2 scale via Dencun. It didn’t spike price overnight; it reshaped the platform’s long-run capacity and institutional palatability (especially post ETH-ETF approvals).

Nuanced view by audience:

- Retail beginners: If you care about price trend and “number go up,” halving years remain historically powerful; if you care about using apps and low fees, the Merge → Dencun pipeline matters more to your daily experience.

- Active retail/informed enthusiasts: Track BTC ETF flows and miner behavior around halvings and watch L2 metrics (fees/users) on ETH; both inform rotations.

- Institutional allocators: For beta to the asset class, the halving-plus-ETF regime is the main event. For venture/infra and fee-sensitive businesses, the Merge’s long-term effects (lower energy, improved UX via L2) are likely the bigger deal.

Bottom line: In 2024–2025, the halving created the larger immediate market impact, while the Merge re-architected Ethereum’s fundamentals, making its impact more enduring and structural.

13) Conclusion

- Trends: Market cap near $4T; BTC dominance stable; ETH’s platform economics improving; liquidity deeper but still event-sensitive; ETFs channeling large, rapid flows.

- Tech: Ethereum’s Merge and Dencun changed energy, issuance, and fees; Solana’s Firedancer aims at resilience + throughput in 2025.

- Regulation: MiCA implementation continues; U.S. moving toward clearer market structure; court rulings and agency posture are reshaping exchange/token risk.

- Verdict: BTC halving = bigger immediate market impact; ETH Merge = bigger structural impact. Together, they’ve driven 2024–2025’s narrative: scarcity + scalability.

Call to action: Keep a weekly rhythm: check CoinDesk for policy/tech, CoinShares for flows, Glassnode for on-chain, Kaiko for liquidity, CoinGecko for caps/dominance. It’s the fastest way to stay ahead of rotations.

14) FAQs (10 quick answers)

- What is Bitcoin’s halving and why does it matter?

Every ~4 years BTC’s block reward halves, cutting new supply (Apr 2024: 6.25 → 3.125 BTC). Supply compression + narrative + ETF-era demand often fuel medium-term uptrends. - What changed with Ethereum’s Merge?

Ethereum shifted to proof-of-stake, slashing energy use by ~99.95% and reducing issuance, laying the foundation for cheaper L2 transactions after Dencun (EIP-4844). - Which event moved prices more in 2024–2025?

Halving, aided by ETF flows, drove stronger headline highs in 2025; the Merge’s effects are more structural (costs, sustainability, issuance). - How do ETFs factor in?

Spot BTC ETFs (since Jan 2024) and ETH ETFs (live since Jul 23, 2024) let institutions allocate at scale; recent weeks saw ETH sometimes out-inflow BTC, showing broadened demand. - What on-chain metrics should I watch?

Active addresses, fees, miner revenue, LTH supply (Glassnode), and exchange reserves (various providers) help gauge stress or froth. Fee spikes around ATHs often mark demand extremes. - Is Solana fixing outages?

The last major outage was Feb 2024; 2025 is focused on Firedancer to add client diversity and big throughput. - Where is DeFi TVL trending?

Up with prices but rotating to L2s and high-throughput chains; check DeFiLlama for protocol and chain-level trends. - What about stablecoins and CBDCs?

Regulators are tightening standards; BIS says >90% of central banks explore CBDCs, and MiCA is reshaping the EU stablecoin market. - How does social media impact prices?

Santiment shows social dominance surges often coincide with local tops; use this as contrarian context with funding and options data. - Best way to keep up weekly?

Scan CoinDesk (policy/tech), CoinShares (flows), Kaiko (liquidity), Glassnode (on-chain), and CoinGecko (caps/dominance) for a rounded view.