1) Introduction

Purpose of the article

This report distills the latest available market data and research to help all audiences—retail investors, Global Crypto beginners, and institutional allocators—quickly grasp the state of the crypto market. It synthesizes price action, on-chain activity, liquidity, regulation, and adoption into a single “health check,” pointing to trusted primary sources throughout (CoinDesk, Glassnode, CoinGecko/CoinMarketCap, CoinShares, Kaiko, DeFiLlama, Bloomberg Crypto, Reuters, BIS/IMF, and others). Where appropriate we cite time-stamped, authoritative datasets.

Why staying updated matters

Crypto moves faster than most asset classes: liquidity regimes can flip in days, regulation can re-price risk premia overnight, and protocol upgrades can structurally cut transaction costs within a single release. For investors and enthusiasts alike, tracking these shifts improves portfolio sizing, timing, risk management, and even product strategy for teams building in the space. Recent examples include the surge and subsequent rotation of ETF flows between BTC and ETH, Ethereum’s Pectra upgrade, and evolving stablecoin/CBDC policy guidance from Global Crypto institutions—all developments with market-wide consequences.

What this piece covers

We’ll walk through market movements (prices, dominance, capitalization), institutional participation, technology and security (L2s, ZK, upgrades), regulation (SEC/CFTC, MiCA, FCA), adoption and sentiment (retail vs institutional, social signals), on-chain activity and liquidity, emerging trends (NFTs/DeFi/stablecoins/CBDCs), investor behavior, and case studies (Bitcoin halving; Ethereum Pectra). Primary sources include CoinGecko/CMC for market caps and prices; CoinShares for ETF/ETP flows; Glassnode/CryptoQuant for on-chain; Kaiko for liquidity; DeFiLlama for TVL; CoinDesk/Reuters/Bloomberg Crypto for news and regulatory context.

2) Global Crypto Market Trends

Current market performance & capitalization

As of today, the global crypto market capitalization is hovering around $3.8–$3.9T. Bitcoin (BTC) dominance sits ~56–58%, with Ethereum (ETH) near 14%. Daily trading volumes are in the $180–$210B range. These figures, refreshed intraday across major aggregators, provide the top-down context for risk and liquidity.

Price snapshots and short-term momentum: BTC has been trading around the low $110Ks recently, while ETH trades in the mid-$4Ks; both show meaningful 7-day volatility around broader macro headlines and ETF flow rotations. Use the 24h/7d bands on price pages for precise deltas at read time.

Trend analysis (24h/7d) and key drivers:

- Macro: Risk appetite has oscillated with shifting expectations for U.S. rate cuts, USD strength, and growth prints—each affecting crypto’s correlation to equities and its positioning as a “reactionary store of value.”

- Flows: ETF/ETP flow cycles have alternated between record inflows and sharp outflows month-to-month, often coinciding with macro data or policy signals.

Institutional involvement & economic influence

ETFs & ETPs: July saw record inflows into digital asset products, led by ETH; in contrast, late August registered one of the largest weekly outflows of 2025—both underscoring how institutional products now drive cyclical risk-on/risk-off in crypto. As of Aug 25, BlackRock’s IBIT reports ~$83B in AUM, illustrating the scale of institutionalization.

Corporate treasuries & crypto-native institutions: Ongoing accumulation by corporates and large holders (e.g., MicroStrategy) continues to concentrate supply and amplify the role of long-term holders—one reason drawdowns often encounter deeper bids than in prior cycles. (For real-time holdings, consult issuer disclosures and earnings/press updates.)

Sentiment: Kaiko and Glassnode note that liquidity and on-chain profitability oscillate with macro, while ETF volumes and market depth have climbed to cycle highs—supportive for price discovery but capable of accelerating both rallies and corrections.

3) Technological Developments & Innovations

Blockchain advancements

Ethereum Pectra (May 7, 2025): Pectra activated on mainnet, combining execution-layer (“Prague”) and consensus-layer (“Electra”) changes. Headliners include EIP-7702 (advancing account abstraction for user-friendly wallets), validator and staking improvements, and refinements that build on Dencun’s blob data path. This materially enhances UX, safety, and scalability for dapps.

Solana client diversity & performance: The forthcoming Firedancer validator client from Jump Crypto targets throughput, resilience, and client diversity, which historically mitigates single-client outage risk. Solana’s own network health reports in 2025 emphasize multiple clients to reduce systemic risk.

On-chain metrics to validate progress: Glassnode’s Market Pulse notes how user activity, fees, and transfer volumes adapt post-upgrade cycles—offering evidence of whether UX and cost improvements translate into organic demand.

Security enhancements in crypto

Zero-knowledge proofs (ZKPs): Ethereum researchers are actively exploring zk-EVM proving for L1, pointing to a future where validity proofs bolster base-layer security and censorship resistance—a notable long-term direction.

“Trillion-Dollar Security” initiative (EF): The Ethereum Foundation outlined a 2025 program to harden education, tooling, and protocol defenses across the stack—an indicator that core teams view security as a first-class public good.

Incident landscape: Despite maturing audits and formal verification, hack losses can still spike (e.g., Immunefi flagged Q1 2025 as a historically severe quarter), reinforcing the need for diversified custody, contract audits, and defense-in-depth across DeFi. Track live exploit data on DeFiLlama’s/De.Fi’s “Rekt” dashboards.

Impact of smart contracts & dapps

Smart contracts now underpin lending, exchanges, structured products, RWA tokenization, and gaming. DappRadar counted ~24.3M daily unique active wallets (dUAW) in Q2 2025 (note: a wallet ≠ a unique person), signaling durable engagement despite rotation among use cases. Messari’s sector and protocol reports add depth on capitalization, user growth, and unit economics across ecosystems.

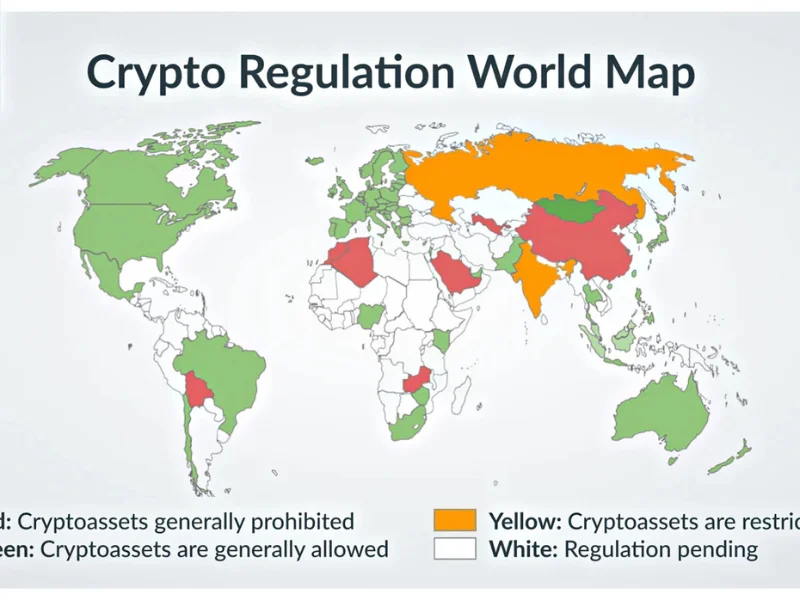

4) Regulatory & Legal Landscape

Current regulatory updates

United States (SEC/CFTC): The policy stance has evolved in 2025. Headlines include the SEC’s leadership changes and initiatives toward a more rules-based, engagement-focused approach to crypto market structure. Discussions span registration pathways, custody, tokenized securities, and ETF expansion.

European Union (MiCA): The EU’s Markets in Crypto-Assets (MiCA) regime entered phased effect, with stablecoin rules prioritized and broader licensing rolling out across 2024–2025. MiCA is reshaping issuer obligations and venue compliance for EU-facing products. Datawallet

United Kingdom (FCA/BoE): The UK is progressing a regulated stablecoin regime (consultations & policy statements in 2024 feeding into 2025 implementation planning), while industry voices call for faster clarity to maintain fintech competitiveness. ethereum.org

Legal cases & precedents

Recent U.S. enforcement settlements and dismissals have materially reframed risk. Notables include:

- Ripple: SEC case concluded with a $125M penalty in Aug 2025—removing a long-running overhang.

- Binance/CZ: DOJ resolution (2023) and 2024 sentencing clarified past AML deficiencies; the SEC dismissed its civil suit in May 2025 amid a broader policy shift.

These outcomes—plus active policy drafting—are feeding into the expanding ETF menu and tokenization pilots at U.S. venues.

5) Adoption & Market Sentiment

Retail and institutional adoption

ETF/ETP penetration has mainstreamed access for advisors, pensions, and model portfolios—an inflection point highlighted by record monthly inflows into crypto ETPs this summer, even as flows remain cyclical week-to-week. Coinbase + Glassnode estimate that structural tailwinds (ETF rails, stablecoin usage) are lifting market depth and dominance of “blue-chip” assets (BTC/ETH).

Retail behavior is evident in wallet adoption and dapp usage (see DappRadar’s dUAW), and in rotating interest across categories (DeFi, NFTs, L2s). CoinGecko’s category boards and market trackers help contextualize where user attention is moving.

Impact of social media & influencers

Sentiment gauges (e.g., Santiment) track keyword spikes (Fed, rates, cuts) that often precede flow rotations; Glassnode and Kaiko complement this with on-chain profit metrics and market depth measures to separate noise from structural signals.

6) On-Chain & Liquidity Activity

Tracking on-chain activity

Why it matters: Active addresses, fees, realized profit/loss, and transfer volumes illuminate organic demand vs speculative churn. Recent Glassnode dispatches show how activity cooled from early-2025 peaks, then re-accelerated into volatility spikes—useful for timing risk and confirming narratives.

Mining & issuance: Post-halving miner economics, fee markets (L2 data blobs on ETH; inscriptions on BTC), and energy costs all feed into sell pressure and security budgets. (Track in Glassnode/CryptoQuant dashboards.)

Liquidity and market microstructure

Market depth at narrow spreads has improved materially vs prior cycles, with Kaiko showing record 1% market depth recently—supporting tighter execution and lower slippage for larger tickets. Kaiko’s liquidity rankings provide asset-level comparisons.

DeFi liquidity: TVL and venue fragmentation matter for slippage and pricing. DappRadar flagged DeFi TVL making fresh ATHs this summer, while NFTs briefly led in users—illustrating how liquidity and attention rotate across verticals.

7) Emerging Trends & Future Outlook

NFTs: growth & impact

After a choppy 2024, NFT activity rebounded mid-2025. DappRadar reported July’s NFT market cap near $7B, and CryptoSlam shows monthly sales in the $400–600M range through the summer. Utility-driven collections (gaming, IP) and brand tie-ins are dominating over pure speculation.

Policy & speech angles: Coin Center continues to frame NFTs and crypto code as speech—relevant as jurisdictions define the boundaries between consumer protection and expression.

DeFi’s continued evolution

Borrow-lend protocols, DEXs, perps, and RWAs remain core pillars. 2025 has seen consolidation of liquidity into venues with strong security histories and robust oracle design. DeFi TVL is climbing again, but attention rotates as yields compress; watch protocol revenues and security incident rates as leading indicators.

Stablecoins & CBDCs

Stablecoins now intermediate massive volumes and are integral to crypto market plumbing, but Global Crypto standard-setters (BIS/ECB) have sharpened critiques—arguing most stablecoins fall short as “sound money” and urging tighter regimes. Meanwhile, 91% of central banks surveyed by BIS report CBDC work continues apace; the IMF outlines how digital money could improve cross-border speed and cost. Expect sustained policy attention and divergent regional models.

8) Investor Insights & Sentiment Analysis

Investor behavior patterns

Cycle anatomy is changing. K33 and others suggest the classic 4-year BTC cycle is weakening as institutional access and macro forces dominate. ETF rails, liquidity, and sovereign interest may create smoother—but still volatile—paths. Glassnode’s NUPL and cost-basis frameworks help map regimes (capitulation → belief → euphoria).

What to watch:

- ETF/ETP flows by asset and issuer (CoinShares weekly).

- On-chain realized profit/loss and illiquid vs liquid supply (Glassnode).

- Market depth/impact and funding/oi (Kaiko).

Risk management in crypto portfolios

Given flow cyclicality and event risk, allocators increasingly employ:

- Sizing bands & DCA to manage entry timing.

- Diversified custody and venue risk checks.

- Hedging via futures/options around known catalysts (e.g., upgrades, policy votes, large unlocks).

Messari’s sector reports and Glassnode’s risk lenses provide data-driven context for these choices.

9) Case Studies & Market Examples

Bitcoin halvings & price impact

Historically, halvings tightened supply and eventually supported higher prices—but effects vary, and lead-lag can be long. The April 2024 halving cut issuance to 3.125 BTC per block; research notes that macro and ETF access may now overshadow pure “stock-to-flow” narratives. Treat halving as a structural tailwind, not a short-term timing tool.

Ethereum’s Pectra transition

Pectra’s mainnet activation in May 2025 progressed Ethereum’s UX and programmability (notably EIP-7702), while reinforcing staking and security mechanics. Post-Pectra data should track L2 fees, blob utilization, and dapp metrics to validate the thesis of cheaper, safer, more composable apps.

10) Impact of Global Crypto Indices

Economic factors driving adoption

Institutional ETF inflows, corporate treasury moves, and expectations for monetary policy have underpinned BTC’s 2025 strength (with ETH increasingly participating). Kaiko’s research ties rallies to USD weakness and rate-cut bets; CoinShares flow surges around macro news confirm the linkage.

Geopolitics & policy

From EU MiCA implementation to U.S. ETF proliferation and tokenization pilots, policy signals now shape liquidity distribution. Reuters and the FT underscore how ETF-ization accelerated mainstream acceptance and may soon extend to additional assets—subject to each jurisdiction’s risk appetite.

11) Key Insights from Industry Experts

- CoinDesk Indices: Halving effects persist but diminish as markets mature; expect macro and structural access (ETFs) to dominate cycle dynamics.

- Bloomberg Crypto / ETF analysts: Crypto ETFs have rapidly scaled, with experts highlighting wealth-platform integrations and a broadening product set in 2025.

- Glassnode + Coinbase Institutional: Bitcoin dominance, ETH sentiment recovery, and stablecoin velocity underpin the 2025 institutional playbook.

- CoinShares: Weekly flow intel is an essential read to contextualize market risk—watch how ETH-led inflows/outflows rotate vs BTC month-to-month.

12) Conclusion

Recap:

- Market: ~$3.8–3.9T cap; BTC dominance mid-50s; liquidity and ETF rails at cycle highs.

- Institutions: Flow regimes are the primary short-cycle driver.

- Tech: Pectra marks a meaningful Ethereum UX and security step; Solana client diversity (Firedancer) targets resilience.

- Policy: U.S. posture is evolving; MiCA reshapes EU obligations; UK stablecoin rules in progress.

- Adoption: dapp engagement persists; NFTs rebounded; stablecoins are systemic to crypto plumbing while CBDCs advance Global Crypto Indices.

Stay informed: Build a dashboard of the sources cited here—CoinDesk, CoinShares, Glassnode, Kaiko, CoinGecko/CMC, DeFiLlama, Reuters/FT/Bloomberg Crypto, BIS/IMF—and review weekly. The highest-signal inputs remain flows, liquidity, and on-chain profitability, set against the macro calendar.

Call to action: Track ETF flows (CoinShares), market depth (Kaiko), on-chain (Glassnode), and policy (CoinDesk/Reuters/Bloomberg). Use these to size risk, identify rotations, and avoid narrative whiplash.

13) FAQs (10 quick answers)

- What is the best single indicator of crypto market “health”?

No single metric suffices. Use a basket: total market cap & dominance (breadth), ETF/ETP net flows (institutional risk-on/off), market depth (execution quality), and on-chain realized P/L (distribution of profits/losses). - Are ETFs “safer” than holding spot crypto?

ETFs add custodial and regulatory layers many investors prefer (audited cold storage, 40-Act/’33 Act-style oversight) but introduce fund-level risks (fees, tracking). Choose based on mandate and constraints; many institutions can only access via ETFs. - How did the 2024 Bitcoin halving change things?

Issuance fell to 3.125 BTC/block. Historically supportive over multi-quarter windows, but 2025 suggests flows + macro can dominate timing. - What did Ethereum’s Pectra actually improve?

Better wallet UX via account abstraction (EIP-7702), validator/staking enhancements, and further scalability groundwork—helping apps reduce friction and costs. - Why does market depth matter for investors?

Deeper order books = lower slippage and more reliable execution. Kaiko shows 2025 depth at or near records for BTC, improving institutional readiness. - Are NFTs “back”?

They’re evolving. July 2025 saw a rebound in market cap and volumes, led by utility and brand IP rather than pure speculation. Expect cyclicality. - What’s the near-term risk for DeFi users?

Smart-contract exploits continue. Use audited protocols, multi-sig or hardware wallets, and conservative collateral ratios; monitor incident trackers. - How do stablecoins and CBDCs fit together?

Stablecoins grease crypto rails; BIS/ECB caution they’re not “sound money” without strict oversight. Meanwhile, 91% of central banks are exploring CBDCs. Expect co-existence with divergent regional rules. - How much should beginners allocate to crypto?

There’s no universal answer; many advisors suggest small, risk-aware allocations given volatility. ETFs can simplify entry; always align with time horizon and drawdown tolerance. (See general advisor commentary.) - What sources should I check weekly?

- CoinShares (flows), Glassnode (on-chain), Kaiko (liquidity), CoinGecko/CMC (caps/prices), DeFiLlama (TVL), CoinDesk/Reuters/Bloomberg Crypto (policy/news). Build a watchlist and compare signals.